Estratégia de média móvel suavizada

Autora:ChaoZhang, Data: 2023-11-06 10:29:24Tags:

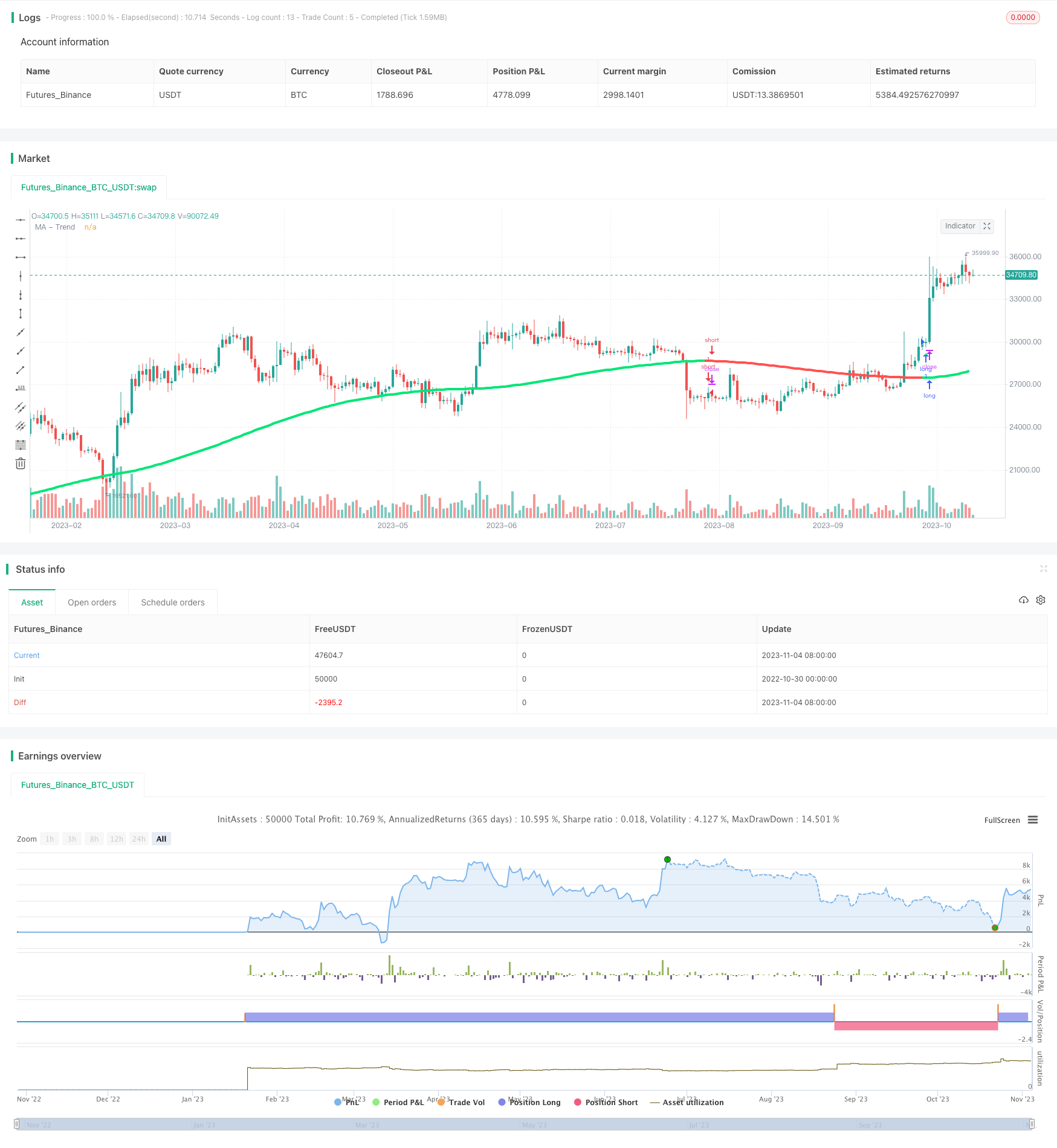

Resumo

Esta estratégia combina múltiplas médias móveis para implementar uma estratégia simples de tendência.

Estratégia lógica

A estratégia primeiro suaviza o preço de fechamento, com a opção de usar o preço de fechamento de Heiken Ashi. Em seguida, chama a função smoothMA para sobrepor múltiplas médias móveis suavizadas. A função smoothMA primeiro chama a função variante, que pode gerar vários tipos de médias móveis como SMA, EMA, DEMA etc. Depois que a função variante gera a média móvel especificada, smoothMA chama variante várias vezes recursivamente para sobrepor a suavização. Isso resulta em uma média móvel com alto nível de suavidade.

Análise das vantagens

- A sobreposição múltipla de médias móveis pode filtrar eficazmente o ruído do mercado e identificar tendências.

- Suporta vários tipos de médias móveis como SMA, EMA, DEMA, etc., permitindo combinações flexíveis.

- A técnica Heiken Ashi filtra falhas.

- Simples e fáceis de implementar.

- O comprimento, o tipo e os tempos de suavização MA personalizáveis permitem a otimização para diferentes produtos.

Análise de riscos

- A suavização múltipla pode causar atraso e perder mudanças iniciais da tendência.

- O sistema MA simples luta para lucrar em mercados variados.

- Ignora os custos de transacção, o que corrói a rentabilidade nas negociações reais.

- Não haverá stop loss, o que implica riscos de perdas aumentadas.

Considere a combinação de outros indicadores como MACD, KDJ para melhorar a precisão do sinal. Otimize os parâmetros MA para reduzir o atraso. Use stop loss razoável para controlar a perda de uma única negociação. Também controle a frequência do comércio para minimizar os custos de transação.

Orientações de otimização

- Teste diferentes comprimentos e tipos de MA para obter a melhor combinação.

- Adicionar outros indicadores técnicos para regras de entrada e saída mais sistemáticas.

- Configure a sessão de negociação para evitar a influência de eventos importantes.

- Ajustar os parâmetros com base nas características do produto.

- Configure stop loss e take profit para controlar os riscos.

Resumo

A estratégia segue as tendências através de múltiplas sobreposições de médias móveis, filtrando efetivamente o ruído do mercado. As vantagens são simplicidade e flexibilidade.

/*backtest

start: 2022-10-30 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Copyright (c) 2007-present Jurik Research and Consulting. All rights reserved.

// Copyright (c) 2018-present, Alex Orekhov (everget)

// Thanks to everget for code for more advanced moving averages

// Smooth Moving Average [STRATEGY] @PuppyTherapy script may be freely distributed under the MIT license.

strategy( title="Smooth Moving Average [STRATEGY] @PuppyTherapy", overlay=true )

// ---- CONSTANTS ----

lsmaOffset = 1

almaOffset = 0.85

almaSigma = 6

phase = 2

power = 2

// ---- GLOBAL FUNCTIONS ----

kama(src, len)=>

xvnoise = abs(src - src[1])

nfastend = 0.666

nslowend = 0.0645

nsignal = abs(src - src[len])

nnoise = sum(xvnoise, len)

nefratio = iff(nnoise != 0, nsignal / nnoise, 0)

nsmooth = pow(nefratio * (nfastend - nslowend) + nslowend, 2)

nAMA = 0.0

nAMA := nz(nAMA[1]) + nsmooth * (src - nz(nAMA[1]))

t3(src, len)=>

xe1_1 = ema(src, len)

xe2_1 = ema(xe1_1, len)

xe3_1 = ema(xe2_1, len)

xe4_1 = ema(xe3_1, len)

xe5_1 = ema(xe4_1, len)

xe6_1 = ema(xe5_1, len)

b_1 = 0.7

c1_1 = -b_1*b_1*b_1

c2_1 = 3*b_1*b_1+3*b_1*b_1*b_1

c3_1 = -6*b_1*b_1-3*b_1-3*b_1*b_1*b_1

c4_1 = 1+3*b_1+b_1*b_1*b_1+3*b_1*b_1

nT3Average_1 = c1_1 * xe6_1 + c2_1 * xe5_1 + c3_1 * xe4_1 + c4_1 * xe3_1

// The general form of the weights of the (2m + 1)-term Henderson Weighted Moving Average

getWeight(m, j) =>

numerator = 315 * (pow(m + 1, 2) - pow(j, 2)) * (pow(m + 2, 2) - pow(j, 2)) * (pow(m + 3, 2) - pow(j, 2)) * (3 * pow(m + 2, 2) - 11 * pow(j, 2) - 16)

denominator = 8 * (m + 2) * (pow(m + 2, 2) - 1) * (4 * pow(m + 2, 2) - 1) * (4 * pow(m + 2, 2) - 9) * (4 * pow(m + 2, 2) - 25)

denominator != 0

? numerator / denominator

: 0

hwma(src, termsNumber) =>

sum = 0.0

weightSum = 0.0

termMult = (termsNumber - 1) / 2

for i = 0 to termsNumber - 1

weight = getWeight(termMult, i - termMult)

sum := sum + nz(src[i]) * weight

weightSum := weightSum + weight

sum / weightSum

get_jurik(length, phase, power, src)=>

phaseRatio = phase < -100 ? 0.5 : phase > 100 ? 2.5 : phase / 100 + 1.5

beta = 0.45 * (length - 1) / (0.45 * (length - 1) + 2)

alpha = pow(beta, power)

jma = 0.0

e0 = 0.0

e0 := (1 - alpha) * src + alpha * nz(e0[1])

e1 = 0.0

e1 := (src - e0) * (1 - beta) + beta * nz(e1[1])

e2 = 0.0

e2 := (e0 + phaseRatio * e1 - nz(jma[1])) * pow(1 - alpha, 2) + pow(alpha, 2) * nz(e2[1])

jma := e2 + nz(jma[1])

variant(src, type, len ) =>

v1 = sma(src, len) // Simple

v2 = ema(src, len) // Exponential

v3 = 2 * v2 - ema(v2, len) // Double Exponential

v4 = 3 * (v2 - ema(v2, len)) + ema(ema(v2, len), len) // Triple Exponential

v5 = wma(src, len) // Weighted

v6 = vwma(src, len) // Volume Weighted

v7 = na(v5[1]) ? sma(src, len) : (v5[1] * (len - 1) + src) / len // Smoothed

v8 = wma(2 * wma(src, len / 2) - wma(src, len), round(sqrt(len))) // Hull

v9 = linreg(src, len, lsmaOffset) // Least Squares

v10 = alma(src, len, almaOffset, almaSigma) // Arnaud Legoux

v11 = kama(src, len) // KAMA

ema1 = ema(src, len)

ema2 = ema(ema1, len)

v13 = t3(src, len) // T3

v14 = ema1+(ema1-ema2) // Zero Lag Exponential

v15 = hwma(src, len) // Henderson Moving average thanks to @everget

ahma = 0.0

ahma := nz(ahma[1]) + (src - (nz(ahma[1]) + nz(ahma[len])) / 2) / len //Ahrens Moving Average

v16 = ahma

v17 = get_jurik( len, phase, power, src)

type=="EMA"?v2 : type=="DEMA"?v3 : type=="TEMA"?v4 : type=="WMA"?v5 : type=="VWMA"?v6 :

type=="SMMA"?v7 : type=="Hull"?v8 : type=="LSMA"?v9 : type=="ALMA"?v10 : type=="KAMA"?v11 :

type=="T3"?v13 : type=="ZEMA"?v14 : type=="HWMA"?v15 : type=="AHMA"?v16 : type=="JURIK"?v17 : v1

smoothMA(c, maLoop, type, len) =>

ma_c = 0.0

if maLoop == 1

ma_c := variant(c, type, len)

if maLoop == 2

ma_c := variant(variant(c ,type, len),type, len)

if maLoop == 3

ma_c := variant(variant(variant(c ,type, len),type, len),type, len)

if maLoop == 4

ma_c := variant(variant(variant(variant(c ,type, len),type, len),type, len),type, len)

if maLoop == 5

ma_c := variant(variant(variant(variant(variant(c ,type, len),type, len),type, len),type, len),type, len)

ma_c

// Smoothing HA Function

smoothHA( o, h, l, c ) =>

hao = 0.0

hac = ( o + h + l + c ) / 4

hao := na(hao[1])?(o + c / 2 ):(hao[1] + hac[1])/2

hah = max(h, max(hao, hac))

hal = min(l, min(hao, hac))

[hao, hah, hal, hac]

// ---- Main Selection ----

haSmooth = input(false, title=" Use HA as source ? " )

length = input(60, title=" MA1 Length", minval=1, maxval=1000)

maLoop = input(2, title=" Nr. of MA1 Smoothings ", minval=1, maxval=5)

type = input("EMA", title="MA Type", options=["SMA", "EMA", "DEMA", "TEMA", "WMA", "VWMA", "SMMA", "Hull", "LSMA", "ALMA", "KAMA", "ZEMA", "HWMA", "AHMA", "JURIK", "T3"])

// ---- BODY SCRIPT ----

[ ha_open, ha_high, ha_low, ha_close ] = smoothHA(open, high, low, close)

_close_ma = haSmooth ? ha_close : close

_close_smoothed_ma = smoothMA( _close_ma, maLoop, type, length)

maColor = _close_smoothed_ma > _close_smoothed_ma[1] ? color.lime : color.red

plot(_close_smoothed_ma, title= "MA - Trend", color=maColor, transp=85, linewidth = 4)

long = _close_smoothed_ma > _close_smoothed_ma[1] and _close_smoothed_ma[1] < _close_smoothed_ma[2]

short = _close_smoothed_ma < _close_smoothed_ma[1] and _close_smoothed_ma[1] > _close_smoothed_ma[2]

plotshape( short , title="Short", color=color.red, transp=80, style=shape.triangledown, location=location.abovebar, size=size.small)

plotshape( long , title="Long", color=color.lime, transp=80, style=shape.triangleup, location=location.belowbar, size=size.small)

//* Backtesting Period Selector | Component *//

//* Source: https://www.tradingview.com/script/eCC1cvxQ-Backtesting-Period-Selector-Component *//

testStartYear = input(2018, "Backtest Start Year",minval=1980)

testStartMonth = input(1, "Backtest Start Month",minval=1,maxval=12)

testStartDay = input(1, "Backtest Start Day",minval=1,maxval=31)

testPeriodStart = timestamp(testStartYear,testStartMonth,testStartDay,0,0)

testStopYear = 9999 //input(9999, "Backtest Stop Year",minval=1980)

testStopMonth = 12 // input(12, "Backtest Stop Month",minval=1,maxval=12)

testStopDay = 31 //input(31, "Backtest Stop Day",minval=1,maxval=31)

testPeriodStop = timestamp(testStopYear,testStopMonth,testStopDay,0,0)

testPeriod() => time >= testPeriodStart and time <= testPeriodStop ? true : false

if testPeriod() and long

strategy.entry( "long", strategy.long )

if testPeriod() and short

strategy.entry( "short", strategy.short )

- Segunda-feira Reversão Tendência intradiária Seguindo estratégia

- ADX Filtrado Chande Kroll Stop Loss Tendência Seguindo a Estratégia

- Indice de desvio de tendência com estratégia de média móvel

- Estratégia de indicador integral de impulso

- MACD Moving Average Crossover Trend Seguindo uma estratégia com trailing stop loss

- Estratégia de fusão de captura de tendências de duas vias

- Preço de avanço Bollinger Band A Estratégia

- RSI baseado na estratégia de negociação da ROC

- A estratégia de alta fuga de ontem

- A tendência segue a estratégia

- Estratégia de negociação de tendência cruzada de média móvel dupla

- Sistema de Tartarugas do Connecticut

- A tendência segue a estratégia

- Estratégia de busca de tendências com laser duplo

- Tendência do oscilador da EMA na sequência da estratégia

- Estratégia de cruzamento da média móvel tripla

- Estratégia de acompanhamento da tendência baseada na ruptura do impulso

- Estratégia de oscilação aleatória

- Super Estratégia de Impulso

- Estratégia de bloqueio de tamanho