Динамическая сетевая стратегия торговли

Автор:Чао Чжан, Дата: 2024-01-23 10:53:05Тэги:

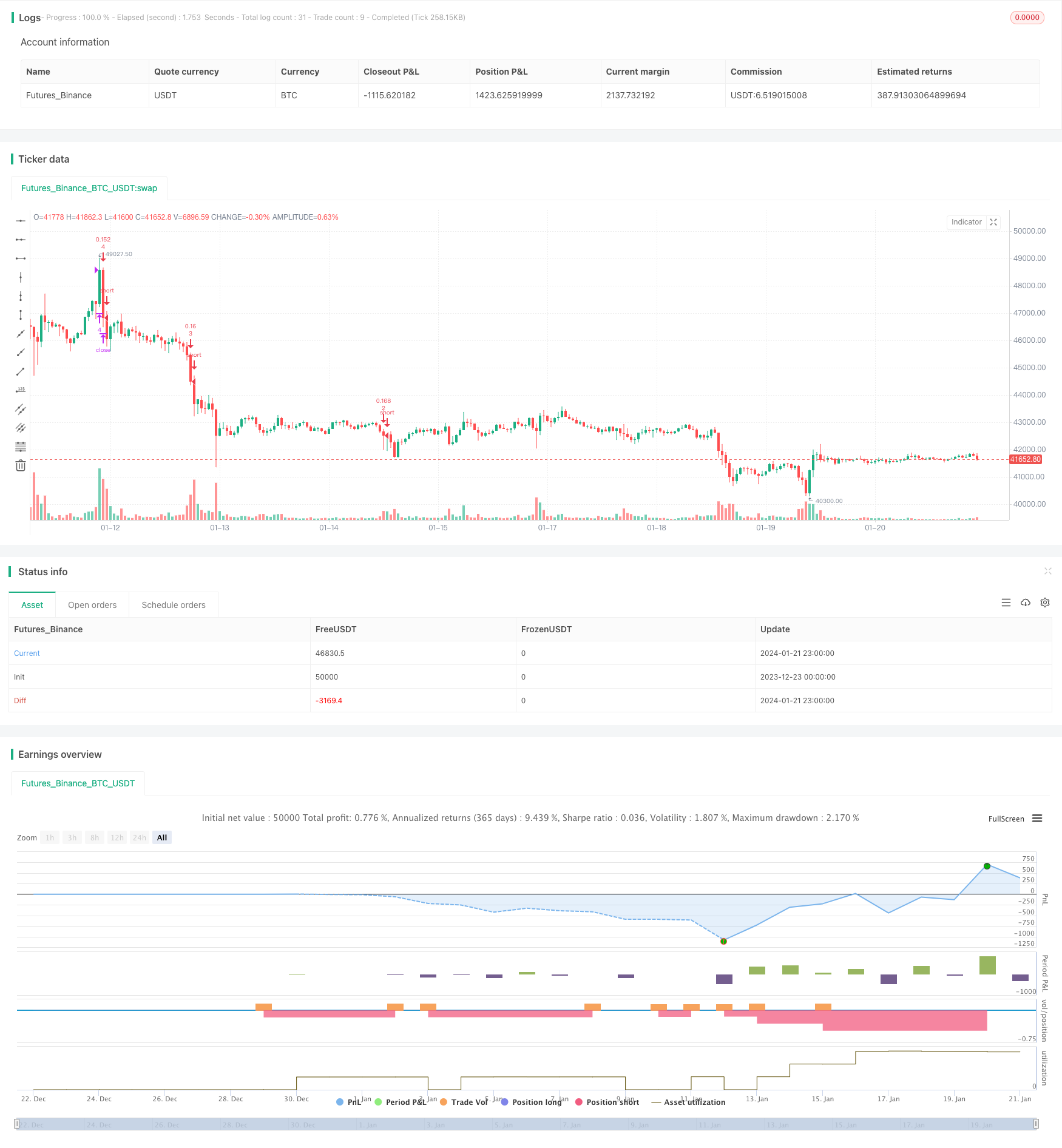

Обзор

Эта стратегия реализует сетевую торговлю путем размещения нескольких параллельных ордеров на покупку и продажу в пределах ценового диапазона.

Логика стратегии

- Установите верхние и нижние границы сети, которые могут быть настроены вручную или автоматически рассчитаны на основе последних высоких и низких цен.

- Вычислить ширину интервала сетки в соответствии с указанным количеством линий сетки.

- Создать массив цен на сетевые линии с соответствующим количеством.

- Когда цена опускается ниже линии сетки, открыть длинный заказ ниже нее; когда цена повышается выше линии сетки, закрыть короткий заказ выше нее.

- Динамически корректировать границы, ширину интервалов и цены на линии сети для адаптации стратегии к изменениям рынка.

Анализ преимуществ

- Могут стабильно получать прибыль на рынке с ограниченным диапазоном и волатильностью, независимо от направления тренда.

- Поддерживает как ручные, так и автоматические настройки параметров для сильной адаптивности.

- Оптимизируемые параметры, такие как количество сетки, ширина интервала и размер заказа для лучшей награды.

- Встроенное управление положением для снижения риска.

- Динамическая регулировка диапазона сетки повышает адаптивность.

Анализ рисков

- В условиях сильного тренда на рынке могут возникнуть серьезные потери.

- Неправильные настройки количества и положения сетки могут увеличить риск.

- Автоматически рассчитанный диапазон сетки может потерпеть неудачу при экстремальных колебаниях цен.

Управление рисками:

- Оптимизируйте параметры сетки и строго контролируйте общую позицию.

- Закройте стратегию до значительного движения цены.

- Судите о состоянии рынка с помощью индикаторов тренда, при необходимости используйте стратегию.

Руководство по оптимизации

- Выберите оптимальное количество сети на основе характера рынка и масштаба капитала.

- Проверьте разные периоды для оптимизации параметров авто.

- Оптимизировать расчет размеров заказов для более стабильной награды.

- Добавить индикаторы для определения тенденции и стратегических условий закрытия.

Резюме

Динамическая стратегия торговли сеткой адаптируется к рынку путем корректировки параметров сети. Она приносит прибыль на рынке с ограниченным диапазоном и волатильностью. При правильном контроле позиций риск смягчается. Оптимизация настроек сети и включение индикаторов оценки тренда могут еще больше улучшить стабильность стратегии.

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("sarasa srinivasa kumar", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving Average

i_boundLookback = input(group="Grid Bounds", title="(Auto) Bound Lookback", defval=250, type=input.integer, maxval=500, minval=0) // when calculating auto grid bounds, how far back should we look for a High & Low, or what should the length be of our sma

i_boundDev = input(group="Grid Bounds", title="(Auto) Bound Deviation", defval=0.10, type=input.float, maxval=1, minval=-1) // if sourcing auto bounds from High & Low, this percentage will (positive) widen or (negative) narrow the bound limits. If sourcing from Average, this is the deviation (up and down) from the sma, and CANNOT be negative.

i_upperBound = input(group="Grid Bounds", title="(Auto) Upper Boundry", defval=0.285, type=input.float) // for manual grid bounds only. The upperbound price of your grid

i_lowerBound = input(group="Grid Bounds", title="(Auto) Lower Boundry", defval=0.225, type=input.float) // for manual grid bounds only. The lowerbound price of your grid.

i_gridQty = input(group="Grid Lines", title="Grid Line Quantity", defval=8, maxval=15, minval=3, type=input.integer) // how many grid lines are in your grid

f_getGridBounds(_bs, _bl, _bd, _up) =>

if _bs == "Hi & Low"

_up ? highest(close, _bl) * (1 + _bd) : lowest(close, _bl) * (1 - _bd)

else

avg = sma(close, _bl)

_up ? avg * (1 + _bd) : avg * (1 - _bd)

f_buildGrid(_lb, _gw, _gq) =>

gridArr = array.new_float(0)

for i=0 to _gq-1

array.push(gridArr, _lb+(_gw*i))

gridArr

f_getNearGridLines(_gridArr, _price) =>

arr = array.new_int(3)

for i = 0 to array.size(_gridArr)-1

if array.get(_gridArr, i) > _price

array.set(arr, 0, i == array.size(_gridArr)-1 ? i : i+1)

array.set(arr, 1, i == 0 ? i : i-1)

break

arr

var upperBound = i_autoBounds ? f_getGridBounds(i_boundSrc, i_boundLookback, i_boundDev, true) : i_upperBound // upperbound of our grid

var lowerBound = i_autoBounds ? f_getGridBounds(i_boundSrc, i_boundLookback, i_boundDev, false) : i_lowerBound // lowerbound of our grid

var gridWidth = (upperBound - lowerBound)/(i_gridQty-1) // space between lines in our grid

var gridLineArr = f_buildGrid(lowerBound, gridWidth, i_gridQty) // an array of prices that correspond to our grid lines

var orderArr = array.new_bool(i_gridQty, false) // a boolean array that indicates if there is an open order corresponding to each grid line

var closeLineArr = f_getNearGridLines(gridLineArr, close) // for plotting purposes - an array of 2 indices that correspond to grid lines near price

var nearTopGridLine = array.get(closeLineArr, 0) // for plotting purposes - the index (in our grid line array) of the closest grid line above current price

var nearBotGridLine = array.get(closeLineArr, 1) // for plotting purposes - the index (in our grid line array) of the closest grid line below current price

strategy.initial_capital = 50000

for i = 0 to (array.size(gridLineArr) - 1)

if close < array.get(gridLineArr, i) and not array.get(orderArr, i) and i < (array.size(gridLineArr) - 1)

buyId = i

array.set(orderArr, buyId, true)

strategy.entry(id=tostring(buyId), long=true, qty=(strategy.initial_capital/(i_gridQty-1))/close, comment="#"+tostring(buyId))

if close > array.get(gridLineArr, i) and i != 0

if array.get(orderArr, i-1)

sellId = i-1

array.set(orderArr, sellId, false)

strategy.close(id=tostring(sellId), comment="#"+tostring(sellId))

if i_autoBounds

upperBound := f_getGridBounds(i_boundSrc, i_boundLookback, i_boundDev, true)

lowerBound := f_getGridBounds(i_boundSrc, i_boundLookback, i_boundDev, false)

gridWidth := (upperBound - lowerBound)/(i_gridQty-1)

gridLineArr := f_buildGrid(lowerBound, gridWidth, i_gridQty)

closeLineArr := f_getNearGridLines(gridLineArr, close)

nearTopGridLine := array.get(closeLineArr, 0)

nearBotGridLine := array.get(closeLineArr, 1)

Больше

- Тенденция адаптивного ATR и RSI после стратегии с последующей остановкой потери

- Стратегия торговли дивергенцией по РСИ

- Тенденция в разных периодах времени в соответствии со стратегией

- Стратегия двойной скользящей средней линии подтверждения преимущества

- Крипто-РСИ Мини-Снайпер быстрого реагирования Тенденция после стратегии

- Эта стратегия - это стратегия импульса, основанная на скользящих средних линиях.

- Стратегия торговли с изменением импульса спроса и предложения

- Стратегия торговли динамическим импульсным осциллятором

- Тенденция в соответствии со стратегией, основанной на скользящей средней

- Стратегия отслеживания тренда

- Стратегия торговли ETF по отслеживанию тенденции реверсионного RSI

- Отслеживание тенденций и краткосрочная стратегия торговли на основе индикатора ADX

- Двойная стратегия импульсного тренда