Wichtige Strategie zur Umkehrung von Backtests

Schriftsteller:ChaoZhangTags:

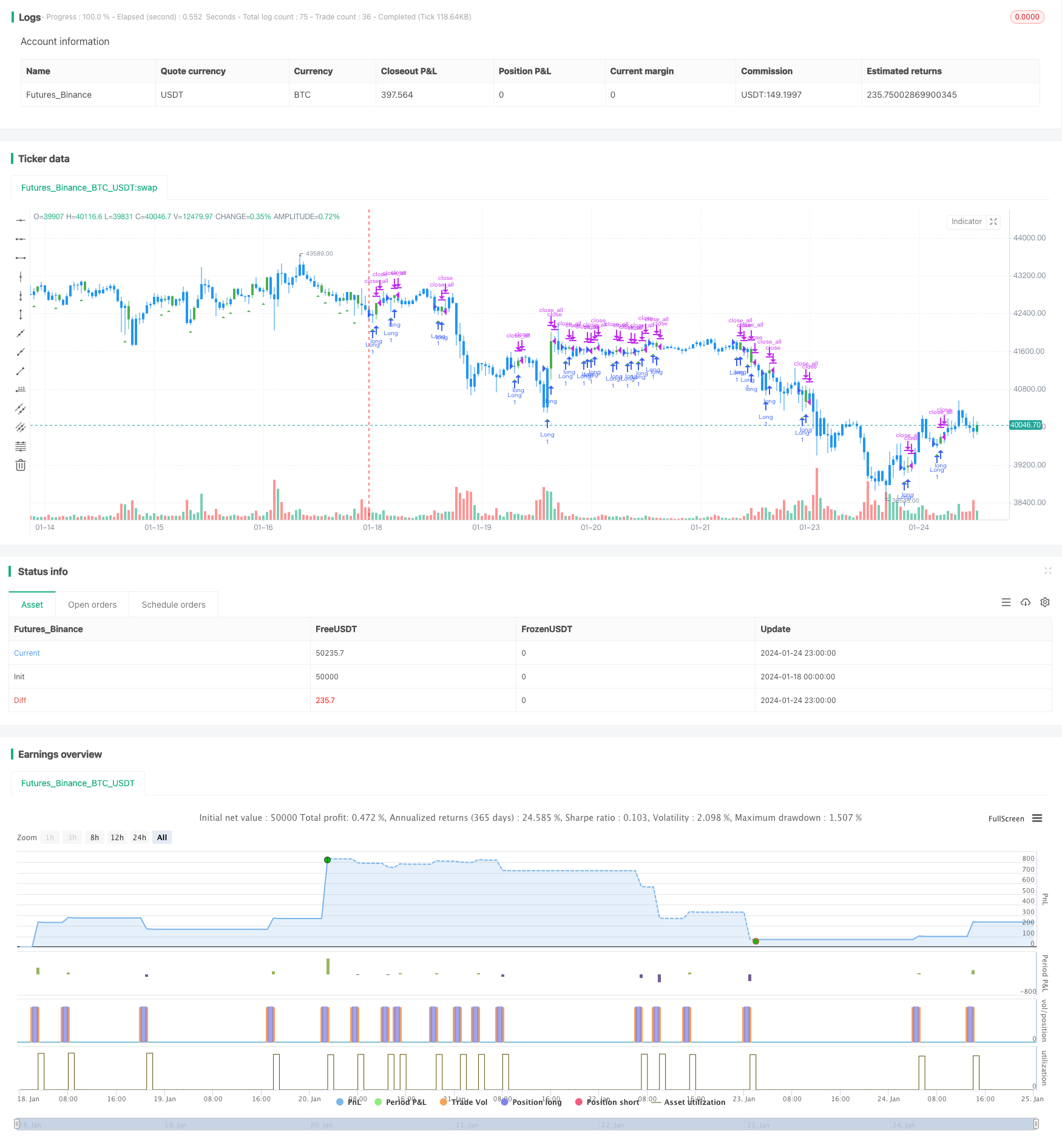

Übersicht

Strategieprinzip

Analyse der Vorteile

Risikoanalyse

Optimierungsrichtlinien

-

Optimieren Sie die Tracking-Strategie nach der Umkehrung. Preisbewegungen nach der Umkehrung haben auch bestimmte Regeln zu befolgen.

Zusammenfassung

/*backtest

start: 2024-01-18 00:00:00

end: 2024-01-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/01/2020

//

// A key reversal is a one-day trading pattern that may signal the reversal of a trend.

// Other frequently-used names for key reversal include "one-day reversal" and "reversal day."

// How Does a Key Reversal Work?

// Depending on which way the stock is trending, a key reversal day occurs when:

// In an uptrend -- prices hit a new high and then close near the previous day's lows.

// In a downtrend -- prices hit a new low, but close near the previous day's highs

// WARNING:

// - For purpose educate only

// - This script to change bars colors.

////////////////////////////////////////////////////////////

strategy(title="Key Reversal Up Backtest", shorttitle="KRU Backtest", overlay = true)

nLength = input(1, minval=1, title="Enter the number of bars over which to look for a new low in prices.")

input_takeprofit = input(20, title="Take Profit pip", step=0.01)

input_stoploss = input(10, title="Stop Loss pip", step=0.01)

xLL = lowest(low[1], nLength)

C1 = iff(low < xLL and close > close[1], true, false)

plotshape(C1, style=shape.triangleup, size = size.small, color=color.green, location = location.belowbar )

posprice = 0.0

pos = 0

barcolor(nz(pos[1], 0) == -1 ? color.red: nz(pos[1], 0) == 1 ? color.green : color.blue )

posprice := iff(C1== true, close, nz(posprice[1], 0))

pos := iff(posprice > 0, 1, 0)

if (pos == 0)

strategy.close_all()

if (pos == 1)

strategy.entry("Long", strategy.long)

posprice := iff(low <= posprice - input_stoploss and posprice > 0, 0 , nz(posprice, 0))

posprice := iff(high >= posprice + input_takeprofit and posprice > 0, 0 , nz(posprice, 0))

Mehr

- Kurzfristige Handelsstrategie der Crossover EMA

- Trend nach Strategie auf Basis eines dynamischen Stop-Loss-Systems für den Dual-EMA-Crossover

- Auftritt des Bullenmarktes Darvas Box Kaufstrategie

- Die relative Dynamikstrategie

- Wellenentwicklung und VWMA-basierte Entwicklung nach Quant-Strategie

- Strategie zur Kombination von Doppel gleitenden Durchschnitten und Williams-Durchschnitten

- Adaptive Dreifach-Supertrend-Strategie

- Strategie für die Verlagerung des gleitenden Durchschnitts

- Mengenmäßige Handelsstrategie mit mehreren Indikatoren

- Market Cypher Welle B Automatische Handelsstrategie

- Die drei EMA Stochastic RSI Crossover Golden Cross-Strategie

- Strategie zur Umkehrung der Backtesting-Strategie

- Die RSI-Strategie wird von Ehlers-Smoothed angewendet.

- Swing-High-Low-Price-Channel-Strategie V.1

- Handelsstrategie zur Umkehrung der Dynamik

- Adaptive lineare Regressionskanalstrategie

- Strategie der gleitenden Durchschnittsdifferenz mit null Kreuz

- Mehrere Indikatoren folgen der Strategie

- Solider Trend nach Strategie

- Preisüberschreitung des gleitenden Durchschnitts nach Strategie