Heiken Ashi Momentum Estrategia Cuántica

El autor:¿ Qué pasa?Las etiquetas:

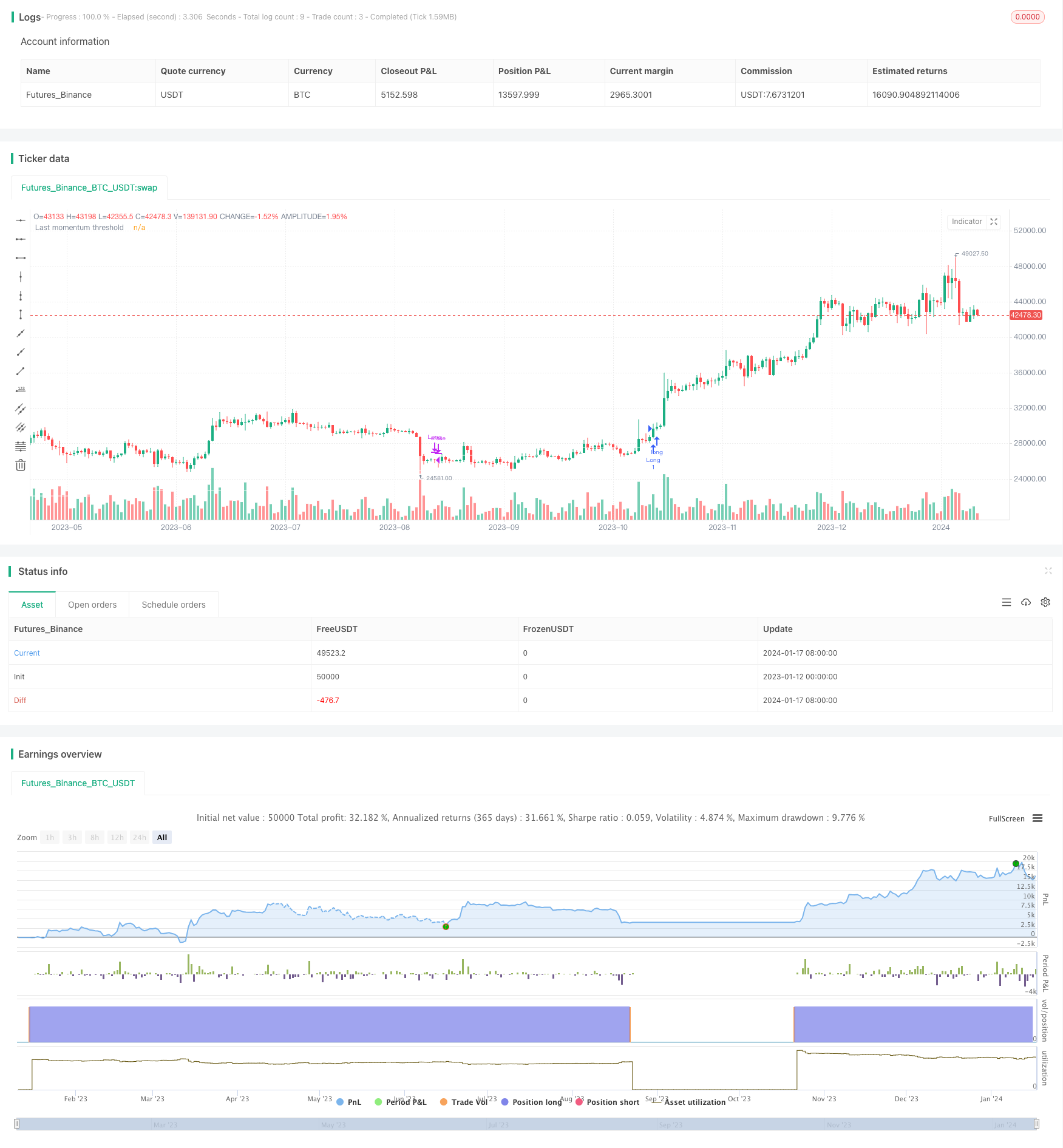

Resumen general

Estrategia lógica

-

Calcular el cambio porcentual entre los precios de apertura y los precios de cierre históricos durante diferentes períodos, tanto para los plazos mensuales como diarios.

-

Tomemos las medias de las fluctuaciones diarias y mensuales del momento, respectivamente.

Análisis de ventajas

Análisis de riesgos

El mayor riesgo es que los cálculos de impulso se basen únicamente en los precios históricos. Si los fundamentos subyacentes de las empresas o los regímenes de mercado experimentan cambios significativos, la representatividad de los precios históricos disminuye, lo que conduce a errores en la identificación de entradas y salidas.

Direcciones de optimización

La estrategia puede mejorarse de varias maneras:

-

Incorporar más marcos de tiempo, construir un mecanismo de puntuación exponencialmente promedio para mejorar la estabilidad.

Conclusión

/*backtest

start: 2023-01-12 00:00:00

end: 2024-01-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FrancoPassuello

//@version=5

strategy("Heiken Ashi ADM", overlay=true)

haClose = (open + high + low + close) / 4

// prevHaOpen = line.new(na, na, na, na, width = 1)

haOpen = (open[1] + close[1]) / 2

// line.set_xy1(prevHaOpen, bar_index[1], nz(haOpen[1]))

// line.set_xy2(prevHaOpen, bar_index, haClose[1])

[monopen, _1monopen, _2monopen, _3monopen, _4monopen, _5monopen, _6monopen] = request.security(syminfo.tickerid, "M", [haOpen, haOpen[1], haOpen[2], haOpen[3], haOpen[4], haOpen[5], haOpen[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[monclose, _1monclose, _3monclose, _6monclose] = request.security(syminfo.tickerid, "M", [haClose, haClose[1], haClose[3], haClose[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[dayclose1, _21dayclose, _63dayclose, _126dayclose, dayclose] = request.security(syminfo.tickerid, "1D", [haClose[1], haClose[21], haClose[63], haClose[126], haClose], barmerge.gaps_off, barmerge.lookahead_on)

[dayopen1, _21dayopen, _63dayopen, _126dayopen] = request.security(syminfo.tickerid, "1D", [haOpen[1], haOpen[21], haOpen[63], haOpen[126]], barmerge.gaps_off, barmerge.lookahead_on)

get_rate_of_return(price1, price2) =>

return_ = (price1/price2 -1)*100

return_

m0 = get_rate_of_return(monclose, monopen)

m1 = get_rate_of_return(_1monclose, _1monopen)

m2 = get_rate_of_return(monclose, _2monopen)

m3 = get_rate_of_return(_1monclose, _3monopen)

m4 = get_rate_of_return(monclose, _4monopen)

m5 = get_rate_of_return(monclose, _5monopen)

m6 = get_rate_of_return(_1monclose, _6monopen)

MS = (m1 + m3 + m6)/100

CS = (m0 + m2 + m5)/100

d1 = get_rate_of_return(dayclose1, _21dayopen)

d2 = get_rate_of_return(dayclose1, _63dayopen)

d3 = get_rate_of_return(dayclose1, _126dayopen)

DS = (d1 + d2 + d3)/100

//Last (DAILY)

lastd_s_avg1 = DS/3

lastd_Approximate1 = dayclose1*(1-lastd_s_avg1)

last_approx1_d21 = lastd_Approximate1 / _21dayopen-1

last_approx1_d63 = lastd_Approximate1 / _63dayopen-1

last_approx1_d126 = lastd_Approximate1 / _126dayopen-1

lastd_s_avg2 = (last_approx1_d21 + last_approx1_d63 + last_approx1_d126) / 3

lastd_approximate2 = (dayclose1)*(1-(lastd_s_avg1 + lastd_s_avg2))

lastd_price = lastd_approximate2

//plot(lastd_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//Last

last_s_avg1 = MS/3

last_Approximate1 = _1monclose*(1-last_s_avg1)

last_approx1_m1 = last_Approximate1 / _1monopen-1

last_approx1_m3 = last_Approximate1 / _3monopen-1

last_approx1_m6 = last_Approximate1 / _6monopen-1

last_s_avg2 = (last_approx1_m1 + last_approx1_m3 + last_approx1_m6) / 3

last_approximate2 = (_1monclose)*(1-(last_s_avg1 + last_s_avg2))

last_price = last_approximate2

Scoring_price = _1monclose*(1-CS)

plot(last_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//plot(Scoring_price,color = color.rgb(234, 0, 255, 14), title = "Last momentum threshold")

//Long based on month close and being the first trade of the month.

var int lastClosedMonth = -1

limit_longCondition = _1monclose > last_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Long based on day close and being the first trade of the month.

limit_Dlongcondition = dayclose1 > lastd_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Close trade based on day close

DCloseLongCondition = dayclose1<lastd_approximate2

//Old standard Trading rules

longCondition = _1monclose > Scoring_price

MCloseLongCondition = _1monclose<Scoring_price

shortCondition = CS < 0

if (longCondition)

strategy.entry("Long", strategy.long)

if (strategy.position_size > 0 and MCloseLongCondition)

strategy.close("Long")

lastClosedMonth := month(time)

- Estrategia de seguimiento de tendencias del oscilador de impulso

- Promedio móvil de superposición de retraso cero con estrategia de negociación de salida Chandelier

- RSI 5 Estrategia de negociación de impulso

- Estrategia de vectores normalizados a escala con funciones de activación, ver.4

- Tendencia siguiendo una estrategia basada en un máximo histórico

- Tendencia de criptomonedas siguiendo una estrategia basada en Heiken Ashi

- Estrategia cuantitativa para el seguimiento de la tendencia de la fortaleza de la MA

- Estrategia de negociación de canal de precios de media móvil doble

- Bitcoin y oro estrategia de scalping de 5 minutos 2.0

- Estrategia de negociación cruzada de promedio móvil intradiario

- Estrategia multi-DCA de la EMA con objetivo de pérdidas y ganancias

- Tendencia de seguimiento de la estrategia basada en los paquetes de Nadaraya-Watson y el indicador ROC

- Dual Take Profit Dual Stop Loss Trailing Stop Loss Bitcoin Estrategia cuantitativa

- Aroon + Williams + MA + BB + ADX Potente estrategia de varios indicadores

- Cruce de media móvil exponencial y media móvil con estrategia cercana

- Optimización de la estrategia de tendencia basada en el gráfico de la nube de Ichimoku

- Reversión de tendencia cruzada combinada con tres estrategias dobles de oscilador de diez

- Candela de promedio de Fibonacci con estrategia de promedio móvil para el comercio cuantitativo

- Estrategia de compra y parada simple basada en el porcentaje

- Un análisis de la estrategia de negociación cuantitativa basada en la función de error de Gauss