Heiken Ashi Momentum Quant Strategi

Penulis:ChaoZhangTag:

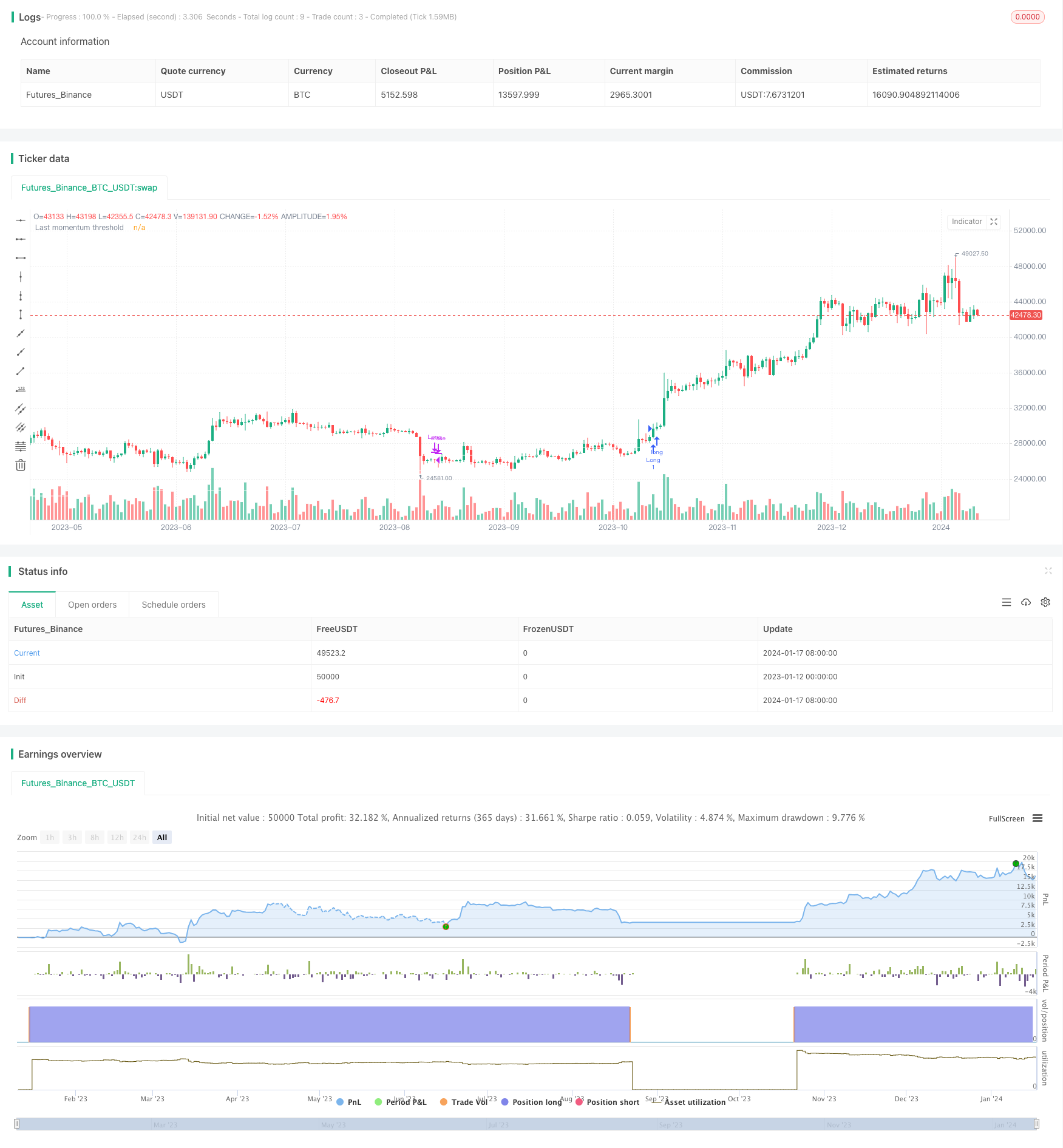

Gambaran umum

Logika Strategi

Analisis Pro

Juga, semua data yang mendasari berasal dari lilin Heiken Ashi, yang secara intrinsik membantu mengurangi masalah ketergantungan berlebihan pada kerangka waktu yang terkait yang ada dalam jenis lain dari strategi lilin.

Analisis Risiko

Arahan Optimasi

-

Lebih lanjut meningkatkan lilin Heiken Ashi sendiri yaitu mengoptimalkan konfigurasi berat.

-

Memperkenalkan data frekuensi yang lebih tinggi seperti bar menit untuk meningkatkan waktu nyata.

Kesimpulan

/*backtest

start: 2023-01-12 00:00:00

end: 2024-01-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FrancoPassuello

//@version=5

strategy("Heiken Ashi ADM", overlay=true)

haClose = (open + high + low + close) / 4

// prevHaOpen = line.new(na, na, na, na, width = 1)

haOpen = (open[1] + close[1]) / 2

// line.set_xy1(prevHaOpen, bar_index[1], nz(haOpen[1]))

// line.set_xy2(prevHaOpen, bar_index, haClose[1])

[monopen, _1monopen, _2monopen, _3monopen, _4monopen, _5monopen, _6monopen] = request.security(syminfo.tickerid, "M", [haOpen, haOpen[1], haOpen[2], haOpen[3], haOpen[4], haOpen[5], haOpen[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[monclose, _1monclose, _3monclose, _6monclose] = request.security(syminfo.tickerid, "M", [haClose, haClose[1], haClose[3], haClose[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[dayclose1, _21dayclose, _63dayclose, _126dayclose, dayclose] = request.security(syminfo.tickerid, "1D", [haClose[1], haClose[21], haClose[63], haClose[126], haClose], barmerge.gaps_off, barmerge.lookahead_on)

[dayopen1, _21dayopen, _63dayopen, _126dayopen] = request.security(syminfo.tickerid, "1D", [haOpen[1], haOpen[21], haOpen[63], haOpen[126]], barmerge.gaps_off, barmerge.lookahead_on)

get_rate_of_return(price1, price2) =>

return_ = (price1/price2 -1)*100

return_

m0 = get_rate_of_return(monclose, monopen)

m1 = get_rate_of_return(_1monclose, _1monopen)

m2 = get_rate_of_return(monclose, _2monopen)

m3 = get_rate_of_return(_1monclose, _3monopen)

m4 = get_rate_of_return(monclose, _4monopen)

m5 = get_rate_of_return(monclose, _5monopen)

m6 = get_rate_of_return(_1monclose, _6monopen)

MS = (m1 + m3 + m6)/100

CS = (m0 + m2 + m5)/100

d1 = get_rate_of_return(dayclose1, _21dayopen)

d2 = get_rate_of_return(dayclose1, _63dayopen)

d3 = get_rate_of_return(dayclose1, _126dayopen)

DS = (d1 + d2 + d3)/100

//Last (DAILY)

lastd_s_avg1 = DS/3

lastd_Approximate1 = dayclose1*(1-lastd_s_avg1)

last_approx1_d21 = lastd_Approximate1 / _21dayopen-1

last_approx1_d63 = lastd_Approximate1 / _63dayopen-1

last_approx1_d126 = lastd_Approximate1 / _126dayopen-1

lastd_s_avg2 = (last_approx1_d21 + last_approx1_d63 + last_approx1_d126) / 3

lastd_approximate2 = (dayclose1)*(1-(lastd_s_avg1 + lastd_s_avg2))

lastd_price = lastd_approximate2

//plot(lastd_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//Last

last_s_avg1 = MS/3

last_Approximate1 = _1monclose*(1-last_s_avg1)

last_approx1_m1 = last_Approximate1 / _1monopen-1

last_approx1_m3 = last_Approximate1 / _3monopen-1

last_approx1_m6 = last_Approximate1 / _6monopen-1

last_s_avg2 = (last_approx1_m1 + last_approx1_m3 + last_approx1_m6) / 3

last_approximate2 = (_1monclose)*(1-(last_s_avg1 + last_s_avg2))

last_price = last_approximate2

Scoring_price = _1monclose*(1-CS)

plot(last_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//plot(Scoring_price,color = color.rgb(234, 0, 255, 14), title = "Last momentum threshold")

//Long based on month close and being the first trade of the month.

var int lastClosedMonth = -1

limit_longCondition = _1monclose > last_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Long based on day close and being the first trade of the month.

limit_Dlongcondition = dayclose1 > lastd_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Close trade based on day close

DCloseLongCondition = dayclose1<lastd_approximate2

//Old standard Trading rules

longCondition = _1monclose > Scoring_price

MCloseLongCondition = _1monclose<Scoring_price

shortCondition = CS < 0

if (longCondition)

strategy.entry("Long", strategy.long)

if (strategy.position_size > 0 and MCloseLongCondition)

strategy.close("Long")

lastClosedMonth := month(time)

Lebih banyak

- Strategi Pelacakan Tren Momentum Oscillator

- Zero Lag Overlapping Moving Average dengan Chandelier exit trading strategy

- RSI 5 Strategi Perdagangan Momentum

- Skala Vektor Strategy dengan fungsi aktivasi, ver.4

- Tren Mengikuti Strategi Berdasarkan Tinggi Sejarah

- Tren Cryptocurrency Mengikuti Strategi Berdasarkan Heiken Ashi

- Strategi Kuantitatif Melacak Tren Kekuatan MA

- Strategi Perdagangan Saluran Harga Rata-rata Bergerak Ganda

- Strategi Scalping 5 Menit Bitcoin dan Emas 2.0

- EMA Multi-DCA Strategy dengan Trailing Stop Loss dan Target Keuntungan

- Tren Mengikuti Strategi Berdasarkan Amplop Nadaraya-Watson dan Indikator ROC

- Aroon + Williams + MA + BB + ADX Strategi multi-indikator yang kuat

- Perpindahan rata-rata bergerak eksponensial dan rata-rata bergerak dengan strategi dekat

- Optimasi Strategi Tren Berdasarkan Bagan Awan Ichimoku

- Peralihan Tren silang dikombinasikan dengan Tiga Strategi Dual Osilator

- Lilin Rata-rata Fibonacci dengan Strategi Rata-rata Bergerak untuk Perdagangan Kuantitatif

- Strategi Stop & Buy yang sederhana berdasarkan Persentase

- Analisis Strategi Perdagangan Kuantitatif Berdasarkan Fungsi Kesalahan Gaussian