ハイケン・アシのモメンタム・量子戦略

作者: リン・ハーンチャオチャンタグ:

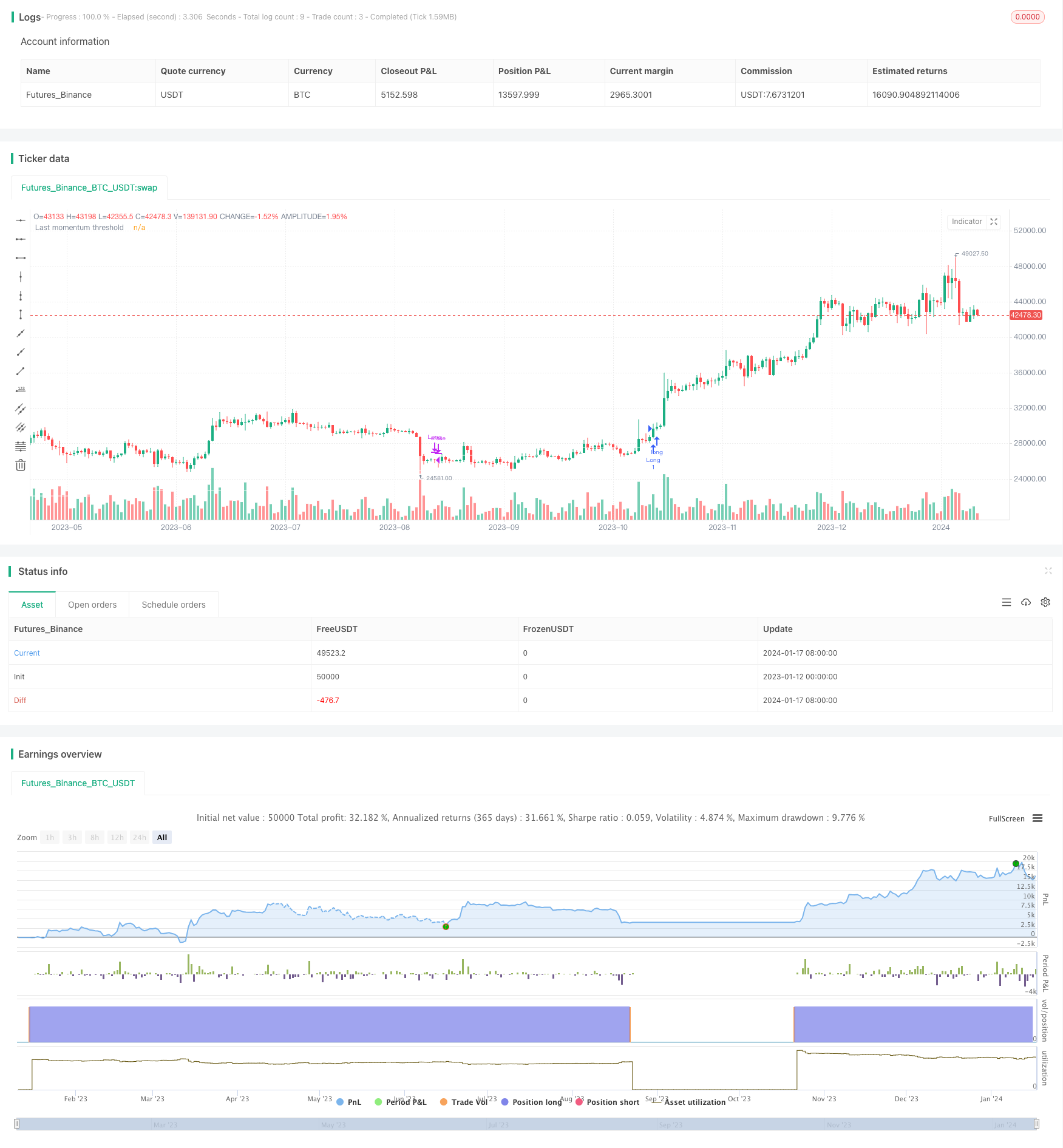

概要

戦略の論理

利点を分析

リスク分析

緩和する方法は,より高い周波数データと 会社の基本面に関するリアルタイムフィードバックを組み込むこと. または検証と最適化のためにより主観的な取引信号で補完することです.

オプティマイゼーションの方向性

戦略をさらに改善するいくつかの方法があります.

結論

/*backtest

start: 2023-01-12 00:00:00

end: 2024-01-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FrancoPassuello

//@version=5

strategy("Heiken Ashi ADM", overlay=true)

haClose = (open + high + low + close) / 4

// prevHaOpen = line.new(na, na, na, na, width = 1)

haOpen = (open[1] + close[1]) / 2

// line.set_xy1(prevHaOpen, bar_index[1], nz(haOpen[1]))

// line.set_xy2(prevHaOpen, bar_index, haClose[1])

[monopen, _1monopen, _2monopen, _3monopen, _4monopen, _5monopen, _6monopen] = request.security(syminfo.tickerid, "M", [haOpen, haOpen[1], haOpen[2], haOpen[3], haOpen[4], haOpen[5], haOpen[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[monclose, _1monclose, _3monclose, _6monclose] = request.security(syminfo.tickerid, "M", [haClose, haClose[1], haClose[3], haClose[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[dayclose1, _21dayclose, _63dayclose, _126dayclose, dayclose] = request.security(syminfo.tickerid, "1D", [haClose[1], haClose[21], haClose[63], haClose[126], haClose], barmerge.gaps_off, barmerge.lookahead_on)

[dayopen1, _21dayopen, _63dayopen, _126dayopen] = request.security(syminfo.tickerid, "1D", [haOpen[1], haOpen[21], haOpen[63], haOpen[126]], barmerge.gaps_off, barmerge.lookahead_on)

get_rate_of_return(price1, price2) =>

return_ = (price1/price2 -1)*100

return_

m0 = get_rate_of_return(monclose, monopen)

m1 = get_rate_of_return(_1monclose, _1monopen)

m2 = get_rate_of_return(monclose, _2monopen)

m3 = get_rate_of_return(_1monclose, _3monopen)

m4 = get_rate_of_return(monclose, _4monopen)

m5 = get_rate_of_return(monclose, _5monopen)

m6 = get_rate_of_return(_1monclose, _6monopen)

MS = (m1 + m3 + m6)/100

CS = (m0 + m2 + m5)/100

d1 = get_rate_of_return(dayclose1, _21dayopen)

d2 = get_rate_of_return(dayclose1, _63dayopen)

d3 = get_rate_of_return(dayclose1, _126dayopen)

DS = (d1 + d2 + d3)/100

//Last (DAILY)

lastd_s_avg1 = DS/3

lastd_Approximate1 = dayclose1*(1-lastd_s_avg1)

last_approx1_d21 = lastd_Approximate1 / _21dayopen-1

last_approx1_d63 = lastd_Approximate1 / _63dayopen-1

last_approx1_d126 = lastd_Approximate1 / _126dayopen-1

lastd_s_avg2 = (last_approx1_d21 + last_approx1_d63 + last_approx1_d126) / 3

lastd_approximate2 = (dayclose1)*(1-(lastd_s_avg1 + lastd_s_avg2))

lastd_price = lastd_approximate2

//plot(lastd_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//Last

last_s_avg1 = MS/3

last_Approximate1 = _1monclose*(1-last_s_avg1)

last_approx1_m1 = last_Approximate1 / _1monopen-1

last_approx1_m3 = last_Approximate1 / _3monopen-1

last_approx1_m6 = last_Approximate1 / _6monopen-1

last_s_avg2 = (last_approx1_m1 + last_approx1_m3 + last_approx1_m6) / 3

last_approximate2 = (_1monclose)*(1-(last_s_avg1 + last_s_avg2))

last_price = last_approximate2

Scoring_price = _1monclose*(1-CS)

plot(last_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//plot(Scoring_price,color = color.rgb(234, 0, 255, 14), title = "Last momentum threshold")

//Long based on month close and being the first trade of the month.

var int lastClosedMonth = -1

limit_longCondition = _1monclose > last_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Long based on day close and being the first trade of the month.

limit_Dlongcondition = dayclose1 > lastd_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Close trade based on day close

DCloseLongCondition = dayclose1<lastd_approximate2

//Old standard Trading rules

longCondition = _1monclose > Scoring_price

MCloseLongCondition = _1monclose<Scoring_price

shortCondition = CS < 0

if (longCondition)

strategy.entry("Long", strategy.long)

if (strategy.position_size > 0 and MCloseLongCondition)

strategy.close("Long")

lastClosedMonth := month(time)

もっと

- モメントオシレータートレンド追跡戦略

- チェンデリア・エグジット・トレード戦略によるゼロ・ラグ・オーバーラッピング・ムービング・メアディア

- RSI 5 モメント・トレード・戦略

- アクティベーション関数を持つスケール化された標準化ベクトル戦略,ver.4

- 戦略をフォローする傾向 歴史的な高値に基づいた

- ハイケン・アシに基づく戦略をフォローする暗号通貨のトレンド

- MA 力の傾向を追跡する定量戦略

- 2つの移動平均価格チャネル取引戦略

- ビットコインとゴールド 5分スカルピング戦略 2.0

- EMAのマルチDCA戦略,ストップ損失と利益目標の追尾

- 二重取利益 二重ストップ損失 トレイリングストップ損失 ビットコイン 定量戦略

- Aroon + Williams + MA + BB + ADX 強力なマルチインジケーター戦略

- 指数関数移動平均と移動平均のクロスオーバーと緊密な戦略

- イチモク・クラウド・チャートに基づくトレンド戦略最適化

- クロストレンド逆転と3つのオシレーターダブル戦略を組み合わせた

- 定量取引のための移動平均戦略を持つフィボナッチ平均キャンドル

- % に基づいたシンプルなストップ&購入戦略

- ガウス誤差関数に基づく定量的な取引戦略の分析