Heiken Ashi Momentum Quant Estratégia

Autora:ChaoZhangTags:

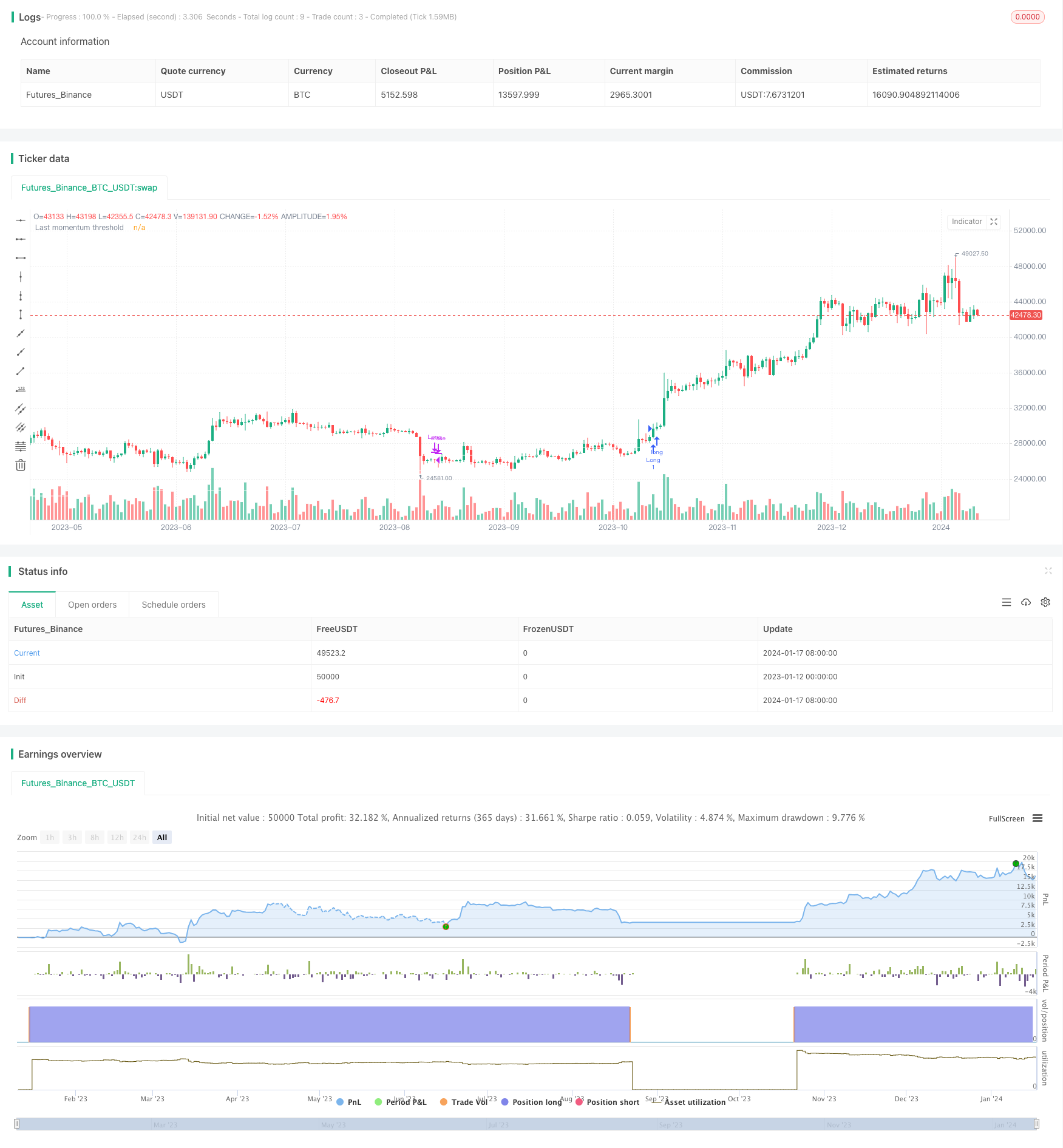

Resumo

Estratégia lógica

-

Quando o preço de fechamento ultrapassa o limiar de impulso, as posições longas são iniciadas mensalmente.

Análise dos prós

Além disso, todos os dados subjacentes são derivados de velas Heiken Ashi, o que intrinsecamente ajuda a reduzir o problema da dependência excessiva de prazos vinculados que existe em outros tipos de estratégias de velas.

Análise de riscos

Orientações de otimização

Há algumas formas de melhorar ainda mais a estratégia:

-

Incorporar mais prazos, construir um mecanismo de pontuação com média exponencial para melhorar a estabilidade.

-

Introduzir dados de maior frequência, como barras de minutos, para melhorar o tempo real.

Conclusão

/*backtest

start: 2023-01-12 00:00:00

end: 2024-01-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © FrancoPassuello

//@version=5

strategy("Heiken Ashi ADM", overlay=true)

haClose = (open + high + low + close) / 4

// prevHaOpen = line.new(na, na, na, na, width = 1)

haOpen = (open[1] + close[1]) / 2

// line.set_xy1(prevHaOpen, bar_index[1], nz(haOpen[1]))

// line.set_xy2(prevHaOpen, bar_index, haClose[1])

[monopen, _1monopen, _2monopen, _3monopen, _4monopen, _5monopen, _6monopen] = request.security(syminfo.tickerid, "M", [haOpen, haOpen[1], haOpen[2], haOpen[3], haOpen[4], haOpen[5], haOpen[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[monclose, _1monclose, _3monclose, _6monclose] = request.security(syminfo.tickerid, "M", [haClose, haClose[1], haClose[3], haClose[6]] , barmerge.gaps_off, barmerge.lookahead_on)

[dayclose1, _21dayclose, _63dayclose, _126dayclose, dayclose] = request.security(syminfo.tickerid, "1D", [haClose[1], haClose[21], haClose[63], haClose[126], haClose], barmerge.gaps_off, barmerge.lookahead_on)

[dayopen1, _21dayopen, _63dayopen, _126dayopen] = request.security(syminfo.tickerid, "1D", [haOpen[1], haOpen[21], haOpen[63], haOpen[126]], barmerge.gaps_off, barmerge.lookahead_on)

get_rate_of_return(price1, price2) =>

return_ = (price1/price2 -1)*100

return_

m0 = get_rate_of_return(monclose, monopen)

m1 = get_rate_of_return(_1monclose, _1monopen)

m2 = get_rate_of_return(monclose, _2monopen)

m3 = get_rate_of_return(_1monclose, _3monopen)

m4 = get_rate_of_return(monclose, _4monopen)

m5 = get_rate_of_return(monclose, _5monopen)

m6 = get_rate_of_return(_1monclose, _6monopen)

MS = (m1 + m3 + m6)/100

CS = (m0 + m2 + m5)/100

d1 = get_rate_of_return(dayclose1, _21dayopen)

d2 = get_rate_of_return(dayclose1, _63dayopen)

d3 = get_rate_of_return(dayclose1, _126dayopen)

DS = (d1 + d2 + d3)/100

//Last (DAILY)

lastd_s_avg1 = DS/3

lastd_Approximate1 = dayclose1*(1-lastd_s_avg1)

last_approx1_d21 = lastd_Approximate1 / _21dayopen-1

last_approx1_d63 = lastd_Approximate1 / _63dayopen-1

last_approx1_d126 = lastd_Approximate1 / _126dayopen-1

lastd_s_avg2 = (last_approx1_d21 + last_approx1_d63 + last_approx1_d126) / 3

lastd_approximate2 = (dayclose1)*(1-(lastd_s_avg1 + lastd_s_avg2))

lastd_price = lastd_approximate2

//plot(lastd_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//Last

last_s_avg1 = MS/3

last_Approximate1 = _1monclose*(1-last_s_avg1)

last_approx1_m1 = last_Approximate1 / _1monopen-1

last_approx1_m3 = last_Approximate1 / _3monopen-1

last_approx1_m6 = last_Approximate1 / _6monopen-1

last_s_avg2 = (last_approx1_m1 + last_approx1_m3 + last_approx1_m6) / 3

last_approximate2 = (_1monclose)*(1-(last_s_avg1 + last_s_avg2))

last_price = last_approximate2

Scoring_price = _1monclose*(1-CS)

plot(last_price,color = color.rgb(255, 255, 255, 14), title = "Last momentum threshold")

//plot(Scoring_price,color = color.rgb(234, 0, 255, 14), title = "Last momentum threshold")

//Long based on month close and being the first trade of the month.

var int lastClosedMonth = -1

limit_longCondition = _1monclose > last_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Long based on day close and being the first trade of the month.

limit_Dlongcondition = dayclose1 > lastd_approximate2 and (lastClosedMonth == -1 or month(time) != lastClosedMonth)

// Close trade based on day close

DCloseLongCondition = dayclose1<lastd_approximate2

//Old standard Trading rules

longCondition = _1monclose > Scoring_price

MCloseLongCondition = _1monclose<Scoring_price

shortCondition = CS < 0

if (longCondition)

strategy.entry("Long", strategy.long)

if (strategy.position_size > 0 and MCloseLongCondition)

strategy.close("Long")

lastClosedMonth := month(time)

Mais.

- Estratégia de acompanhamento da tendência do oscilador de impulso

- Média móvel de sobreposição de atraso zero com estratégia de negociação de saída Chandelier

- RSI 5 Estratégia de negociação de momento

- Estratégia de vetor normalizada em escala com funções de ativação, vers.4

- Tendência Seguindo Estratégia Baseada em Altíssimo Histórico

- Tendência de criptomoeda seguindo estratégia baseada em Heiken Ashi

- Estratégia quantitativa de acompanhamento da tendência da força da MA

- Estratégia de negociação de canal de preços de média móvel dupla

- Estratégia de Scalping de 5 Minutos do Bitcoin e do Ouro 2.0

- Estratégia de negociação cruzada de média móvel intradiária

- Estratégia multi-DCA da EMA com um trailing stop loss e uma meta de lucro

- Tendência na sequência da estratégia baseada nos envelopes Nadaraya-Watson e no indicador ROC

- Dual Take Profit Dual Stop Loss Trailing Stop Loss Bitcoin Estratégia Quantitativa

- Aroon + Williams + MA + BB + ADX Estratégia multi-indicador poderosa

- Crossover da média móvel exponencial e da média móvel com estratégia próxima

- Uma estratégia de otimização de tendências baseada no gráfico de nuvens de Ichimoku

- Reversão de tendência cruzada combinada com três estratégias duplas de oscilador de dez

- Candela de média de Fibonacci com estratégia de média móvel para negociação quantitativa

- Estratégia de compra e parada simples baseada em porcentagem

- Uma análise da estratégia de negociação quantitativa baseada na função de erro de Gauss