Python version of simple grid policy

Author: Inventors quantify - small dreams, Created: 2020-01-04 14:28:04, Updated: 2024-12-15 16:03:28

Python version of simple grid policy

There are not many Python strategies on Strategy Square, but here is a Python version of the grid strategy. The strategy is very simple: a series of grid nodes are generated within a price range at a fixed price distance, and when the market changes, the price reaches a grid node price position and hangs a buy order.

The risk of a grid strategy is not necessary to say, any grid strategy is a strategy for the price fluctuation in a certain range, and once the price breaks out of the grid range, it can cause a serious float. So the purpose of writing this strategy is to provide a reference in Python strategy writing ideas or program design.

The explanation of the strategy idea is written directly in the commentary of the strategy code.

The Strategy Code

'''backtest

start: 2019-07-01 00:00:00

end: 2020-01-03 00:00:00

period: 1m

exchanges: [{"eid":"OKEX","currency":"BTC_USDT"}]

'''

import json

# 参数

beginPrice = 5000 # 网格区间开始价格

endPrice = 8000 # 网格区间结束价格

distance = 20 # 每个网格节点的价格距离

pointProfit = 50 # 每个网格节点的利润差价

amount = 0.01 # 每个网格节点的挂单量

minBalance = 300 # 账户最小资金余额(买入时)

# 全局变量

arrNet = []

arrMsg = []

acc = None

def findOrder (orderId, NumOfTimes, ordersList = []) :

for j in range(NumOfTimes) :

orders = None

if len(ordersList) == 0:

orders = _C(exchange.GetOrders)

else :

orders = ordersList

for i in range(len(orders)):

if orderId == orders[i]["Id"]:

return True

Sleep(1000)

return False

def cancelOrder (price, orderType) :

orders = _C(exchange.GetOrders)

for i in range(len(orders)) :

if price == orders[i]["Price"] and orderType == orders[i]["Type"]:

exchange.CancelOrder(orders[i]["Id"])

Sleep(500)

def checkOpenOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "pending" :

orderId = exchange.Sell(arrNet[i]["coverPrice"], arrNet[i]["amount"], arrNet[i], ticker)

if orderId :

arrNet[i]["state"] = "cover"

arrNet[i]["id"] = orderId

else :

# 撤销

cancelOrder(arrNet[i]["coverPrice"], ORDER_TYPE_SELL)

arrMsg.append("挂单失败!" + json.dumps(arrNet[i]) + ", time:" + _D())

def checkCoverOrders (orders, ticker) :

global arrNet, arrMsg

for i in range(len(arrNet)) :

if not findOrder(arrNet[i]["id"], 1, orders) and arrNet[i]["state"] == "cover" :

arrNet[i]["id"] = -1

arrNet[i]["state"] = "idle"

Log(arrNet[i], "节点平仓,重置为空闲状态。", "#FF0000")

def onTick () :

global arrNet, arrMsg, acc

ticker = _C(exchange.GetTicker) # 每次获取当前最新的行情

for i in range(len(arrNet)): # 遍历所有网格节点,根据当前行情,找出需要挂单的位置,挂买单。

if i != len(arrNet) - 1 and arrNet[i]["state"] == "idle" and ticker.Sell > arrNet[i]["price"] and ticker.Sell < arrNet[i + 1]["price"]:

acc = _C(exchange.GetAccount)

if acc.Balance < minBalance : # 如果钱不够了,只能跳出,什么都不做了。

arrMsg.append("资金不足" + json.dumps(acc) + "!" + ", time:" + _D())

break

orderId = exchange.Buy(arrNet[i]["price"], arrNet[i]["amount"], arrNet[i], ticker) # 挂买单

if orderId :

arrNet[i]["state"] = "pending" # 如果买单挂单成功,更新网格节点状态等信息

arrNet[i]["id"] = orderId

else :

# 撤单

cancelOrder(arrNet[i]["price"], ORDER_TYPE_BUY) # 使用撤单函数撤单

arrMsg.append("挂单失败!" + json.dumps(arrNet[i]) + ", time:" + _D())

Sleep(1000)

orders = _C(exchange.GetOrders)

checkOpenOrders(orders, ticker) # 检测所有买单的状态,根据变化做出处理。

Sleep(1000)

orders = _C(exchange.GetOrders)

checkCoverOrders(orders, ticker) # 检测所有卖单的状态,根据变化做出处理。

# 以下为构造状态栏信息,可以查看FMZ API 文档。

tbl = {

"type" : "table",

"title" : "网格状态",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "记录",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

while len(arrMsg) > 20 :

arrMsg.pop(0)

for i in range(len(arrMsg)) :

errTbl["rows"].append([i, json.dumps(arrMsg[i])])

for i in range(len(orders)) :

orderTbl["rows"].append([i, json.dumps(orders[i])])

LogStatus(_D(), "\n", acc, "\n", "arrMsg length:", len(arrMsg), "\n", "`" + json.dumps([tbl, errTbl, orderTbl]) + "`")

def main (): # 策略执行从这里开始

global arrNet

for i in range(int((endPrice - beginPrice) / distance)): # for 这个循环根据参数构造了网格的数据结构,是一个列表,储存每个网格节点,每个网格节点的信息如下:

arrNet.append({

"price" : beginPrice + i * distance, # 该节点的价格

"amount" : amount, # 订单数量

"state" : "idle", # pending / cover / idle # 节点状态

"coverPrice" : beginPrice + i * distance + pointProfit, # 节点平仓价格

"id" : -1, # 节点当前相关的订单的ID

})

while True: # 构造好网格数据结构后,进入策略主要循环

onTick() # 主循环上的处理函数,主要处理逻辑

Sleep(500) # 控制轮询频率

The main design idea of the strategy is to compare the data structure of the grid that you maintain against the data structure of the grid that you maintain.GetOrdersThe interface returns the current list of pending orders. It analyzes the changes in the pending orders (whether or not they are executed), updates the grid data structure, and makes follow-up operations. And pending orders are not revoked until they are executed, even if the price deviates.

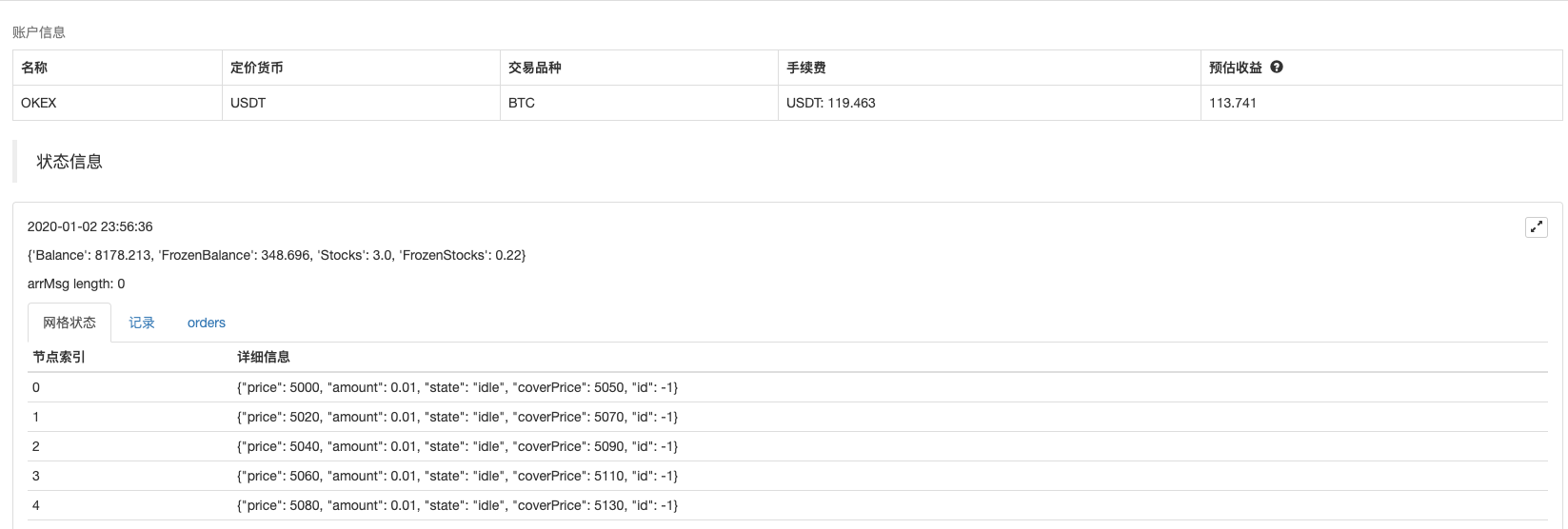

Strategy data visualized and usedLogStatusThe function displays the data in real time on the status bar.

tbl = {

"type" : "table",

"title" : "网格状态",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

for i in range(len(arrNet)) :

tbl["rows"].append([i, json.dumps(arrNet[i])])

errTbl = {

"type" : "table",

"title" : "记录",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

orderTbl = {

"type" : "table",

"title" : "orders",

"cols" : ["节点索引", "详细信息"],

"rows" : [],

}

Three tables were constructed, the first showing information for each node in the current grid data structure, the second showing information for anomalies, and the third showing information for the actual listing of the exchange.

Re-tested

Policy address

The strategy is for reference learning only, retesting tests, and interest in optimizing upgrades.

- Quantitative Practice of DEX Exchanges (2) -- Hyperliquid User Guide

- DEX exchange quantitative practices ((2) -- Hyperliquid user guide

- Quantitative Practice of DEX Exchanges (1) -- dYdX v4 User Guide

- Introduction to Lead-Lag Arbitrage in Cryptocurrency (3)

- DEX exchange quantitative practice ((1) -- dYdX v4 user guide

- Introduction to the Lead-Lag suite in digital currency (3)

- Introduction to Lead-Lag Arbitrage in Cryptocurrency (2)

- Introduction to the Lead-Lag suite in the digital currency (2)

- Discussion on External Signal Reception of FMZ Platform: A Complete Solution for Receiving Signals with Built-in Http Service in Strategy

- Discussing FMZ platform external signal reception: a complete set of strategies for the reception of signals from built-in HTTP services

- Introduction to Lead-Lag Arbitrage in Cryptocurrency (1)

- Timing start or stop widgets for quantified trading robots using Python

- Corrupt Sisters Speak at the First Session of the General Assembly

- Quantitative fractional rate trading strategy

- The Python spreadsheet platform balancing strategy

- The old farmer's journey to the pit

- The story of a post-95 coin collector

- Hands-on teaches you how to convert a Python single-variety policy into a multi-variety policy.

- My automation loss and FMZ shore trip

- FMZ heartbeat pathway - leap forward strategy included

- Python's chase and kill strategy

- Quantified trading tools for open-source digital currency options

- Handshake teaches you how to write a K-line syntax in Python

- Handshake teaches you how to add support for multiple charts to a policy

- Linear hang single-stream strategy based on data playback feature development

- Hands-on to teach you how to transplant a Macanese language strategy (progress)

- Q&A about how to get started with cryptocurrency

- Inventors Quantify FMex Mining Strategy and Use Guide

- Cross-currency hedging strategies in blockchain asset quantification

- Modified Deribit futures API to accommodate options quantitative trading

- The hand teaches you how to write a strategy -- to translate a strategy into my language.

The Millennial Squirrel# Withdrawal cancelOrder ((arrNet[i]["price", ORDER_TYPE_BUY) # Cancel with the withdrawal function What is the use of this price to cancel the order for index? fmz's api only shows id, ok exchange's current documentation only shows id or custom id...

fjabingThat's good!

The Millennial SquirrelHey, I see the def up there, sorry sorry.

Inventors quantify - small dreamsCancelOrder, this is my custom function.