MT-Coordination Trading Strategy

Author: ChaoZhang, Date: 2024-01-25 15:06:04Tags:

Overview

The MT-Coordination Trading Strategy is an advanced quantitative trading strategy integrating multiple technical indicators to identify short-term trading opportunities in financial markets. Designed by renowned trader I3ig_Trades, it is specialized for high-frequency trading.

Strategy Logic

The strategy incorporates three Smoothed Moving Averages (SMA) of different timeframes (21, 50, 200), the 14-day Relative Strength Index (RSI) and the Williams Fractals (2 days). The specific entry logic is defined as follows:

Long signal: Triggered when close is above all three SMAs, RSI is above 50 and current high is greater than the previous fractal up.

Short signal: Activated when close is below all three SMAs, RSI is below 50 and current low is less than the previous fractal down.

Position sizing is dynamically calculated based on selected percentage of equity and leverage level.

Advantage Analysis

This strategy combines multiple indicators to filter out false signals and identify high probability breakout levels, greatly reducing trading risk. Meanwhile, the position sizing is set according to a percentage of account equity, controlling single loss.

Specific strengths are:

Using multi timeframe indicators for confirmation to avoid traps. SMAs recognize trends across short, medium and long terms.

RSI avoids overbought and oversold zones. Values above 50 signal bullishness and below 50 signal bearishness.

Williams Fractals further verify the breakout, only entering on penetration of extremes.

Dynamic position sizing based on percentage of account balance strictly manages downside.

Customizable parameters suit different trading styles.

Risk Analysis

The main risks of this strategy include:

Failure to fully avoid whipsaws when SMAs diverge.

Inability to exit timely before trend reversal due to lagging indicators.

Risk of losing the full position in extreme moves when loss exceeds preset.

Solutions:

Optimize SMAs combinations to find best parameters.

Add candlestick filters to further avoid false breakouts.

Reduce percentage and leverage levels appropriately.

Optimization Directions

The strategy can be further enhanced by:

Testing different combinations of SMAs and RSI for optimal parameters.

Incorporating additional filters like Bollinger Bands width, traderjack signals etc.

Adding stop loss mechanisms to cut losses at a predefined level.

Integrating deep learning models for support and resistance detection.

Implementing adaptive position sizing scheme for sensible scaling of positions.

Conclusion

The MT-Coordination Trading Strategy is a mature breakout system leveraging multiple timeframes. By combining indicators to filter signals and dynamically managing position sizing, it is capable of consistent profits for capitalized funds and professional traders through continuous parameter tuning and model optimization.

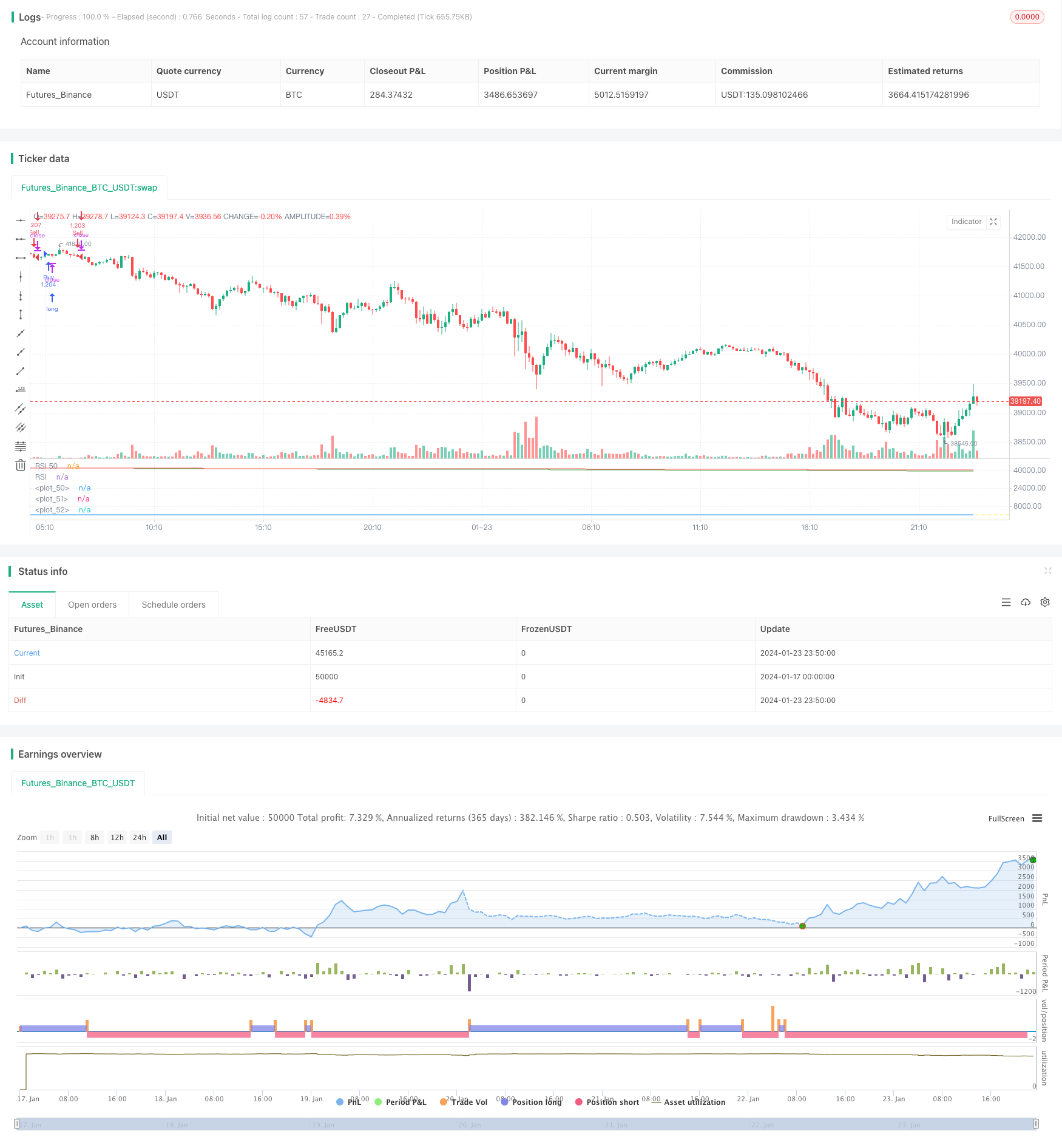

/*backtest

start: 2024-01-17 00:00:00

end: 2024-01-24 00:00:00

period: 10m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// Written by I3ig_Trades. Follow And Let Me Know Any Strategies You'd Like To See!

strategy("Best Scalping Strategy Period (TMA)", shorttitle="Best Scalping Strategy Period (TMA)", overlay=false,

initial_capital=100000,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100)

// Leverage Input

leverage = input.float(1, title="Leverage", minval=1, step=0.1)

// Calculate position size based on the percentage of the portfolio and leverage

percentOfPortfolio = input.float(100, title="Percent of Portfolio")

// Define input options

rsiLength = input.int(14, title="RSI Length", minval=1)

williamsLength = input.int(2, title="Williams Fractals Length", minval=1)

sma21Length = input.int(21, title="SMA 21 Length", minval=1)

sma50Length = input.int(50, title="SMA 50 Length", minval=1)

sma200Length = input.int(200, title="SMA 200 Length", minval=1)

// Smoothed Moving Averages

sma21 = ta.sma(close, sma21Length)

sma50 = ta.sma(close, sma50Length)

sma200 = ta.sma(close, sma200Length)

// RSI

rsiValue = ta.rsi(close, rsiLength)

// Williams Fractals

fractalUp = ta.highest(close, williamsLength)

fractalDown = ta.lowest(close, williamsLength)

// Conditions for Buy Entry

buyCondition = close > sma21 and close > sma50 and close > sma200 and rsiValue > 50 and high > fractalUp[1]

// Conditions for Sell Entry

sellCondition = close < sma21 and close < sma50 and close < sma200 and rsiValue < 50 and low < fractalDown[1]

positionSizePercent = percentOfPortfolio / 100 * leverage

positionSize = strategy.equity * positionSizePercent / close

// Executing strategy with dynamic position size

if buyCondition

strategy.entry("Buy", strategy.long, qty=positionSize)

if sellCondition

strategy.entry("Sell", strategy.short, qty=positionSize)

// Plotting the Smoothed Moving Averages

plot(sma21, color=color.white)

plot(sma50, color=color.green)

plot(sma200, color=color.red)

// Plotting RSI and Fractals for visual confirmation

hline(50, "RSI 50", color=color.yellow)

plot(rsiValue, color=color.blue, title="RSI")

// Input text boxes for trading actions

var buy_entry_params = input("", title="Buy Entry Parameters")

var buy_exit_params = input("", title="Buy Exit Parameters")

var sell_entry_params = input("", title="Sell Entry Parameters")

var sell_exit_params = input("", title="Sell Exit Parameters")

- Dual Reversal Oscillating Band Trend Following Strategy

- Trend Following Strategy Based on DMI and RSI

- Quantitative Support and Resistance Oscillation Strategy

- Trend-Following Strategy with 3 EMAs, DMI and MACD

- Dual Indicators Breakthrough Strategy

- Pete Wave Trading System Strategy

- Quantitative Strategy Based on Exponential Moving Average and Volume Weighting

- Origix Ashi Strategy Based on Smoothed Moving Average

- BlackBit Trader XO Macro Trend Scanner Strategy

- Crude Oil ADX Trend Following Strategy

- Combo Strategy of Double Factors Reversal and Improved Price Volume Trend

- Trend Angle Moving Average Crossover Strategy

- This strategy makes trading decisions based on the trend of MACD Histogram

- Momentum Oscillator & 123 Pattern Strategy

- Backtesting Strategy Based on Fisher Transform Indicator

- Oscillation Spectrum Moving Average Trading Strategy

- Reversal Trading Strategy Based on Moving Average Range

- Kalman Filter Based Trend Tracking Strategy

- Seasonal Reversal Intertemporal Trading Strategy

- Dual Exponential Moving Average Crossover Algorithmic Trading Strategy