Multi Timeframe Strategy

Author: ChaoZhang, Date: 2024-02-19 11:13:22Tags:

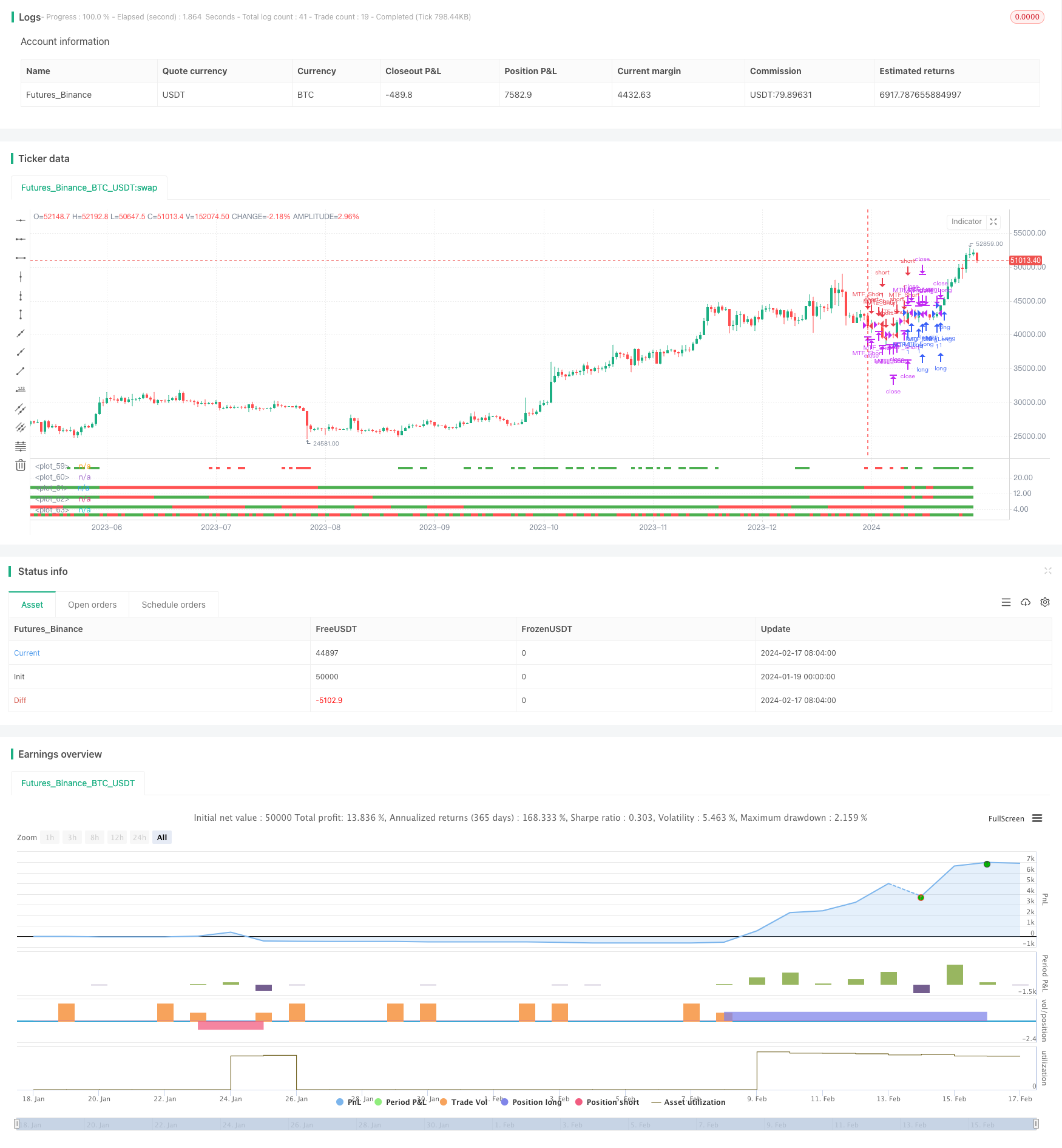

Overview

This strategy utilizes the agreement of indicators across multiple timeframes to track trends. It goes long or short when the daily, 10-day, 15-day and 30-day timeframes simultaneously give bullish or bearish signals, with dynamic stop loss.

Strategy Logic

The strategy judges trend direction using four timeframes - daily, 10-day, 15-day and 30-day. When the closing prices are higher than the opening prices across all four timeframes, it indicates a bullish signal. When the closing prices are lower than the opening prices across all four timeframes, it indicates a bearish signal.

When the signal is bullish, it goes long. When the signal is bearish, it goes short. After entering, KC channel is used for dynamic stop loss.

Specifically, the strategy compares the opening prices and closing prices across different timeframes to determine the trend direction. If closing price is higher than opening price, the timeframe is considered bullish and plotted in green. If closing price is lower than opening price, the timeframe is considered bearish and plotted in red.

When all four timeframes agree on a bullish signal, the strategy will open a long position. When all four timeframes agree on a bearish signal, the strategy will open a short position. It will exit when hit the stop loss or the trend reverses.

Advantages

Using multiple timeframes to confirm trends can effectively filter false breakouts and determine trend direction.

Dynamic stop loss can maximize capital protection.

Strict entry criteria reduces unnecessary trades and slippage costs.

Combining multiple timeframes balances profit speed and stability.

Risks

Entry criteria may be too strict, missing some opportunities.

Improper stop loss setting may be too aggressive or conservative.

Inappropriate timeframe selections may not align with longer or shorter term trends.

Sudden reversals from events may not trigger stop loss.

Enhancement Areas

Optimize timeframe selections to balance profit speed and stability.

Test different parameter settings to optimize stop loss levels.

Add machine learning algorithms to assist in judging reversal points.

Monitor significant events to avoid losses from sudden reversals.

Summary

This strategy integrates judgments across multiple timeframes, with strict entry criteria and dynamic stops, aiming for steady returns. It has the risk of missing opportunities and improper risk control. Next step is to continue optimizing parameters for higher stability.

/*backtest

start: 2024-01-19 00:00:00

end: 2024-02-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("[RichG] Easy MTF Strategy v1.1", overlay=false)

TF_1_time = input("D", "Timeframe 1")

TF_2_time = input("10D", "Timeframe 2")

TF_3_time = input("15D", "Timeframe 3")

TF_4_time = input("30D", "Timeframe 4")

lengthKC=input(20, title="KC Length")

multKC = input(1.5, title="KC MultFactor")

lengthBB=input(20, title="BB Length")

transaction_size = input(1, "Contract/Share Amount")

src = close, len = 20

out = sma(src, len)

width = 5

upcolor = green

downcolor = red

neutralcolor = blue

linestyle = line

kc() =>

ma = sma(close, lengthKC)

range = tr

rangema = sma(range, lengthKC)

upperKC = ma + rangema * multKC

lowerKC = ma - rangema * multKC

[lowerKC, upperKC]

bb() =>

source = close

basis = sma(source, lengthBB)

dev = multKC * stdev(source, lengthBB)

upperBB = basis + dev

lowerBB = basis - dev

[upperBB, lowerBB]

TF_1 = request.security(syminfo.tickerid, TF_1_time, open) < request.security(syminfo.tickerid, TF_1_time, close) ? true:false

TF_1_color = TF_1 ? upcolor:downcolor

TF_2 = request.security(syminfo.tickerid, TF_2_time, open) < request.security(syminfo.tickerid, TF_2_time, close) ? true:false

TF_2_color = TF_2 ? upcolor:downcolor

TF_3 = request.security(syminfo.tickerid, TF_3_time, open) < request.security(syminfo.tickerid, TF_3_time, close) ? true:false

TF_3_color = TF_3 ? upcolor:downcolor

TF_4 = request.security(syminfo.tickerid, TF_4_time, open) < request.security(syminfo.tickerid, TF_4_time, close) ? true:false

TF_4_color = TF_4 ? upcolor:downcolor

TF_global = TF_1 and TF_2 and TF_3 and TF_4

TF_global_bear = TF_1 == false and TF_2 == false and TF_3 == false and TF_4 == false

TF_global_color = TF_global ? green : TF_global_bear ? red : white

TF_trigger_width = TF_global ? 6 : width

plot(1, style=linestyle, linewidth=width, color=TF_1_color)

plot(5, style=linestyle, linewidth=width, color=TF_2_color)

plot(10, style=linestyle, linewidth=width, color=TF_3_color)

plot(15, style=linestyle, linewidth=width, color=TF_4_color)

plot(25, style=linestyle, linewidth=4, color=TF_global_color)

exitCondition_Long = TF_global_bear

exitCondition_Short = TF_global

longCondition = TF_global

if (longCondition)

strategy.entry("MTF_Long", strategy.long, qty=transaction_size)

shortCondition = TF_global_bear

if (shortCondition)

strategy.entry("MTF_Short", strategy.short, qty=transaction_size)

[kc_lower,kc_upper] = kc()

strategy.close("MTF_Long", when=close < kc_upper)

strategy.close("MTF_Short", when=close > kc_lower)

- Moving Average Breakout and Bollinger Band Breakout Strategy

- Absolute Momentum Indicator Strategy

- Supertrend and Moving Average Crossover Strategy

- Dual Trend Breakout Strategy

- SSL Channel and Wave Trend Quantitative Trading Strategy

- Super ATR Trend Following Strategy

- Trading-oriented Ichimoku Cloud Nine Strategy

- LPB Microcycles Adaptive Oscillation Contour Tracking Strategy

- Best ABCD Pattern Trading Strategy with Stop Loss and Take Profit Tracking

- Major Trend Indicator Long

- Dynamic Balancing Leveraged ETF Investment Strategy

- Multi-timeframe MACD Indicator Crossover Trading Strategy

- Gem Forest 1 Minute Breakout Strategy

- Three High Candle Reversal Strategy

- MACD Moving Average Combination Cross-Period Dynamic Trend Strategy

- Gem Forest One Minute Scalping Strategy

- Signal Smoothing Ehlers Cyber Cycle Strategy

- EMA Crossover Trend Following Trading Strategy

- Trend Following Strategy Based on Candlestick Direction

- Dual Confirmation MACD and RSI Strategy