Momentum Breakout Backtesting Support Resistance Strategy

Author: ChaoZhang, Date: 2024-02-22 16:07:14Tags:

Overview

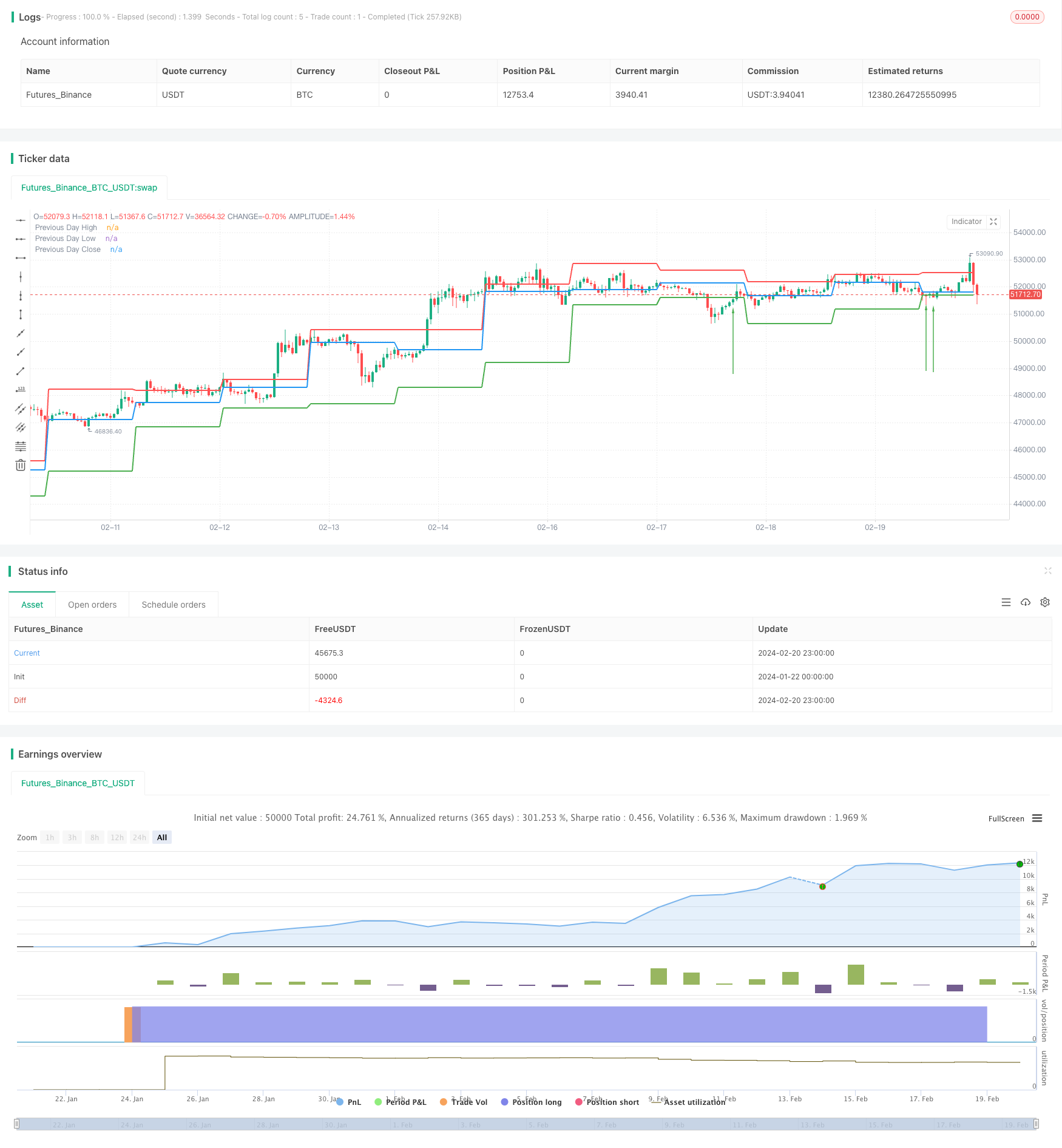

This strategy mainly uses the previous trading day’s high, low and close prices as the support and resistance levels for the current day. It goes long when the resistance level is broken and goes short when the support level is backtested. It belongs to a typical breakout strategy.

Strategy Principle

The code first defines a function calculateSupportResistance to calculate the support and resistance levels, which extracts the previous trading day’s high, low and close prices as the current day’s support and resistance levels.

Then in the main logic, this function is called to get these three price levels and plot them.

In the backtesting logic, if the close price is lower than the previous day’s low while the current price is higher than that low forming a breakout, it goes long. If the close price is higher than the previous day’s high while the current price is lower than that high forming a breakout, it goes short.

Through this breakout model, the judgment of trend and generation of trading signals are implemented.

Advantages

-

Use previous trading day’s data to build current day’s support and resistance levels, avoiding the parameter optimization problem

-

Support and resistance levels come from real market trading data, with some reference value

-

Simple and straightforward backtesting model, easy to understand and implement

-

Visual display of support and resistance levels forms perception of prices

-

Real-time monitoring of breakouts, timely catching trading opportunities

Risks

-

Support and resistance levels change over time, hard to determine validity

-

Unable to predict trend direction, risk of missing reversals

-

Easily affected by false breakouts, premature entry risk

-

Unable to determine persistence of breakouts, early stop loss likely

-

Individual support and resistance failure more likely under huge market fluctuation

Countermeasures:

-

Combine more factors to judge validity of breakouts

-

Appropriately expand stop loss range to catch trends

-

Open positions in batches, reduce impact of individual fluctuations

Optimizations

-

Add more historical data like 5-day, 10-day lines to determine levels

-

Incorporate other indicators like volume to judge breakout validity

-

Set stop loss based on actual volatility

-

Optimize capital management, control single loss

Summary

Overall this is a typical breakout strategy, simple and intuitive. By building current day’s support and resistance with previous day’s data and backtesting breakouts of those levels for long/short. Pros are easy to understand and directly visualize levels; cons are false breakout risks and uncertainty of persistence. Next steps are improving breakout validity, controlling risks, optimizing capital management etc.

/*backtest

start: 2024-01-22 00:00:00

end: 2024-02-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Support and Resistance with Backtesting", overlay=true)

// Function to calculate support and resistance levels

calculateSupportResistance() =>

highPrevDay = request.security(syminfo.tickerid, "D", high[1], lookahead=barmerge.lookahead_on)

lowPrevDay = request.security(syminfo.tickerid, "D", low[1], lookahead=barmerge.lookahead_on)

closePrevDay = request.security(syminfo.tickerid, "D", close[1], lookahead=barmerge.lookahead_on)

[highPrevDay, lowPrevDay, closePrevDay]

// Call the function to get support and resistance levels

[supResHigh, supResLow, supResClose] = calculateSupportResistance()

// Plotting support and resistance levels

plot(supResHigh, color=color.red, linewidth=2, title="Previous Day High")

plot(supResLow, color=color.green, linewidth=2, title="Previous Day Low")

plot(supResClose, color=color.blue, linewidth=2, title="Previous Day Close")

// Backtesting logic

backtestCondition = close[1] < supResLow and close > supResLow

strategy.entry("Long", strategy.long, when=backtestCondition)

// Plotting buy/sell arrows for backtesting

plotarrow(backtestCondition ? 1 : na, colorup=color.green, offset=-1, transp=0)

- Adaptive Fluctuation Strategy Based on Quantitative Range Breakthrough

- Bull Flag Breakout Strategy

- The Moving Average Crossover Trading Strategy

- Moving Average Crossover Gold Trading Strategy

- EMA and MACD Trend Following Strategy

- Moving Average Crossover MACD Trading Strategy

- Super Trend Daily Reversal Strategy

- Dual EMA Crossover Strategy

- Trend Tracking Strategy Based on RSI and ZigZag Indicators

- Moving Average Crossover Breakout Strategy

- MyQuant Trend Identifier Strategy

- Dual Trendlines Breakout Golden Cross Death Cross Trend Following Strategy

- Nifty 50 Quantitative Trading Strategy Based on Dynamic Position Adjustment with Support and Resistance Levels

- Dynamic Channel Moving Average Trend Tracking Strategy

- Harmonic Dual System Strategy

- Breakthrough Callback Long Strategy

- MA Crossover Trading Strategy Based on Short-term and Long-term Moving Average Crossovers

- Dual Moving Average Crossover MACD Quantitative Strategy

- Dual Moving Average Pressure Rebound Strategy

- Four WMA Trend Tracking Strategy