Triple Bottom Rebound Momentum Breakthrough Strategy

Author: ChaoZhang, Date: 2025-01-10 15:49:30Tags: EMAATRMASMA

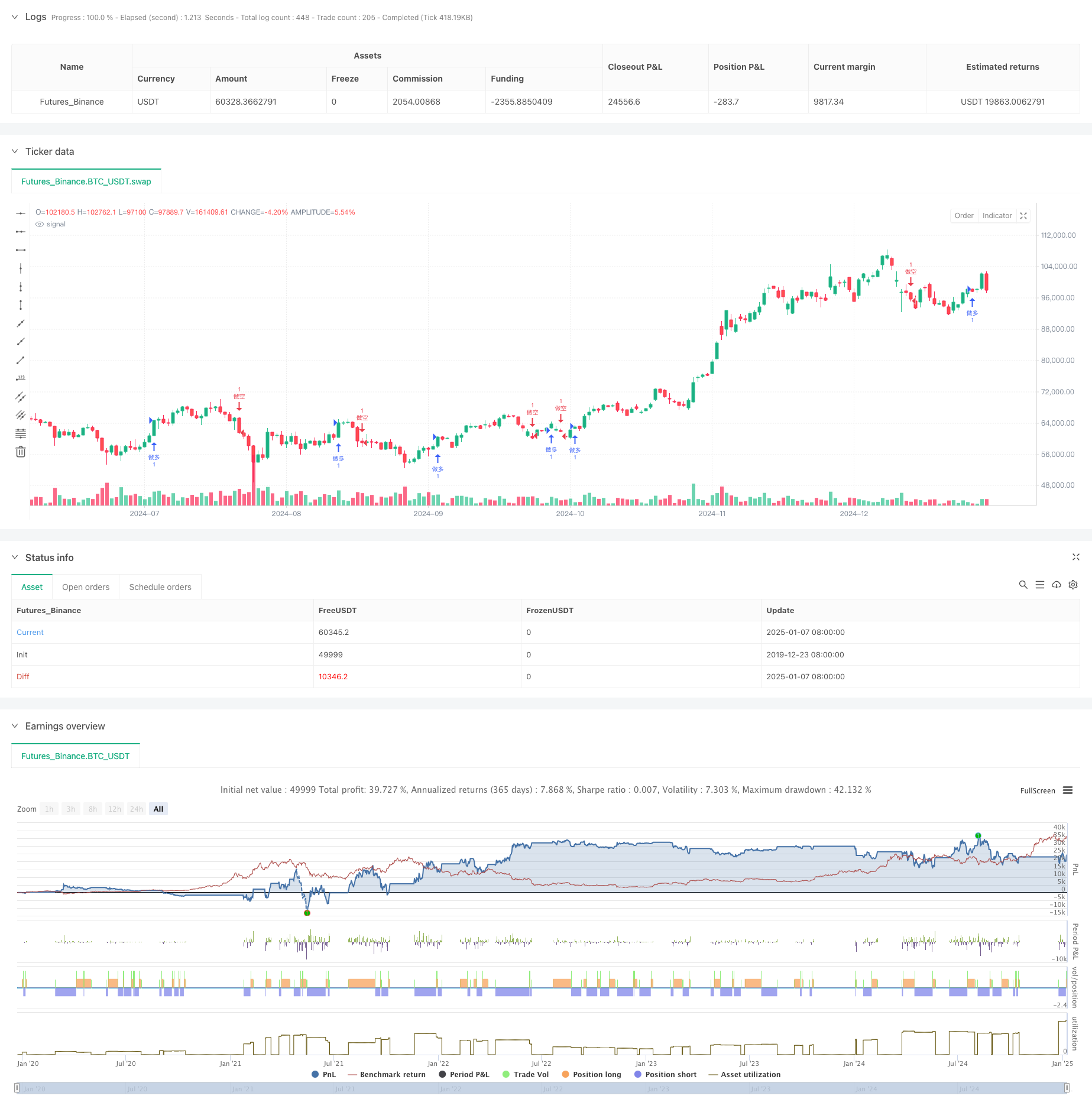

Overview

This strategy is a quantitative trading system based on technical analysis, primarily focusing on identifying triple bottom patterns and momentum breakthrough signals in the market. The strategy combines multiple technical indicators including Moving Average (MA) crossovers, Average True Range (ATR), and price channels to build a complete trading system. Through programmatic implementation, it achieves automated identification of triple bottom rebound patterns and trade execution.

Strategy Principles

The core logic includes the following key elements: 1. Using fast (5-period) and slow (20-period) moving average crossovers to confirm market trend direction 2. Automatically identifying three consecutive low points (low1, low2, low3) to form a triple bottom pattern 3. Utilizing ATR indicator to calculate volatility and set dynamic stop-loss and take-profit levels 4. Confirming long entry signals when price breaks above previous rebound high after the third bottom, combined with MA crossover signals 5. Establishing parallel channels to visualize price movement ranges for additional market reference 6. Implementing ATR-based dynamic stop-loss and take-profit conditions during trade execution

Strategy Advantages

- Combines multiple technical indicators to enhance signal reliability

- Uses ATR to dynamically adjust stop-loss and take-profit levels, adapting to market volatility changes

- Automates triple bottom pattern identification, reducing subjective judgment

- Implements trade interval restrictions to prevent overtrading

- Provides clear market structure reference through visualization tools (parallel channels and labels)

- Features clear strategy logic for easy maintenance and optimization

Strategy Risks

- May generate false signals in highly volatile markets

- Triple bottom pattern identification process may be affected by market noise

- Fixed ATR multipliers may not suit all market conditions

- May experience consecutive losses during trend reversal periods

- Trade interval settings might miss some valid signals

Strategy Optimization Directions

- Incorporate volume indicators to confirm rebound validity

- Dynamically adjust ATR multipliers based on different market conditions

- Add trend strength filters to improve trading signal quality

- Optimize triple bottom identification algorithm to increase accuracy

- Incorporate market cycle analysis to optimize trade interval settings

- Consider adding price pattern symmetry analysis

Summary

This strategy implements a triple bottom rebound breakthrough trading system programmatically, combining multiple technical indicators and risk management measures with good practicality. Through continuous optimization and improvement, the strategy shows promise for better performance in actual trading. It is recommended to conduct thorough backtesting before live trading and adjust parameters according to specific market conditions.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-08 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=5

strategy("反彈三次突破策略", overlay=true, initial_capital=100000, commission_value=0.001425, slippage=1)

// === 參數設定 ===

fast_length = input.int(5, title="快速均線週期")

slow_length = input.int(20, title="慢速均線週期")

atr_period = input.int(14, title="ATR 週期")

atr_factor = input.float(2.0, title="ATR 因子")

profit_factor = input.float(2.0, title="止盈因子")

// === 計算均線 ===

fast_ma = ta.ema(close, fast_length)

slow_ma = ta.ema(close, slow_length)

// === 均線交叉訊號 ===

long_signal = ta.crossover(fast_ma, slow_ma)

short_signal = ta.crossunder(fast_ma, slow_ma)

// === 計算 ATR ===

atr = ta.atr(atr_period)

// === 反彈三次突破策略 ===

var float low1 = na

var float low2 = na

var float low3 = na

var bool trend_down = false

var bool long_breakout = false

var line lower_line = na

var line upper_line = na

if (na(low1) or na(low2) or na(low3))

// 初始化低點

low1 := na

low2 := na

low3 := na

if (close < low3 or na(low3))

// 更新低點

low1 := low2

low2 := low3

low3 := close

trend_down := true

if (trend_down and close > low2 and close > low1)

// 確認反轉且第三次反彈比第二次高

trend_down := false

long_breakout := true

// 清除前一個反彈通道

if (not na(lower_line))

line.delete(lower_line)

if (not na(upper_line))

line.delete(upper_line)

// 繪製新的反彈通道

if (not na(low1) and not na(low3))

lower_line := line.new(x1=bar_index[2], y1=low1, x2=bar_index, y2=low3, color=color.yellow, width=2)

upper_line := line.new(x1=bar_index[2], y1=low1 + (low3 - low1), x2=bar_index, y2=low3 + (low3 - low1), color=color.yellow, width=2)

// === 進出場條件 ===

var float last_long_exit = na

var float last_short_exit = na

var float stop_loss_long = na

var float take_profit_long = na

var float stop_loss_short = na

var float take_profit_short = na

var label stop_loss_label_long = na

var label take_profit_label_long = na

var label stop_loss_label_short = na

var label take_profit_label_short = na

if (long_signal or long_breakout)

if na(last_short_exit) or (time - last_short_exit) > 2 * 60 * 60 * 1000 // 確保多頭出場後有一段時間間隔

// 做多

strategy.entry("做多", strategy.long)

// 止損設置為最近低點下方

stop_loss_long := low3 - atr_factor * atr

take_profit_long := close + profit_factor * atr // 設定止盈位置

strategy.exit("止盈/止損", "做多", stop=stop_loss_long, limit=take_profit_long)

last_long_exit := time // 記錄多頭出場時間

// 刪除之前的止盈止損標籤

if (not na(stop_loss_label_long))

label.delete(stop_loss_label_long)

if (not na(take_profit_label_long))

label.delete(take_profit_label_long)

// 繪製新的止盈止損標籤

stop_loss_label_long := label.new(x=bar_index, y=stop_loss_long, text=str.tostring(math.round(stop_loss_long * 10) / 10), color=color.red, style=label.style_label_down, textcolor=color.white, size=size.small)

take_profit_label_long := label.new(x=bar_index, y=take_profit_long, text=str.tostring(math.round(take_profit_long * 10) / 10), color=color.green, style=label.style_label_up, textcolor=color.white, size=size.small)

if (short_signal)

if na(last_long_exit) or (time - last_long_exit) > 2 * 60 * 60 * 1000 // 確保空頭出場後有一段時間間隔

// 做空

strategy.entry("做空", strategy.short)

// 止損設置為最近高點上方

stop_loss_short := high + atr_factor * atr

take_profit_short := close - profit_factor * atr // 設定止盈位置

strategy.exit("止盈/止損", "做空", stop=stop_loss_short, limit=take_profit_short)

last_short_exit := time // 記錄空頭出場時間

// 刪除之前的止盈止損標籤

if (not na(stop_loss_label_short))

label.delete(stop_loss_label_short)

if (not na(take_profit_label_short))

label.delete(take_profit_label_short)

// 繪製新的止盈止損標籤

stop_loss_label_short := label.new(x=bar_index, y=stop_loss_short, text=str.tostring(math.round(stop_loss_short * 10) / 10), color=color.red, style=label.style_label_down, textcolor=color.white, size=size.small)

take_profit_label_short := label.new(x=bar_index, y=take_profit_short, text=str.tostring(math.round(take_profit_short * 10) / 10), color=color.green, style=label.style_label_up, textcolor=color.white, size=size.small)

- Dynamic Moving Average Crossover Trend Following Strategy with ATR Risk Management System

- Multi-Indicator Fusion Mean Reversion Trend Following Strategy

- Enhanced Price-Volume Trend Momentum Strategy

- Adaptive Moving Average Crossover with Trailing Stop-Loss Strategy

- No Upper Wick Bullish Candle Breakout Strategy

- Multi-Level Intelligent Dynamic Trailing Stop Strategy Based on Bollinger Bands and ATR

- Elliott Wave Theory 4-9 Impulse Wave Automatic Detection Trading Strategy

- MA, SMA, MA Slope, Trailing Stop Loss, Re-Entry

- Dynamic ATR Stop Loss and Take Profit Moving Average Crossover Strategy

- Dynamic Trend Following Multi-Period Moving Average Crossover Strategy

- Multi-EMA Crossover Trend Following Quantitative Trading Strategy

- Multi-level Indicator Overlapping RSI Trading Strategy

- Bollinger Bands and Fibonacci Intraday Trend Following Strategy

- Dynamic Trend Following Dual Moving Average Channel Strategy with Risk Management System

- Multi-Mode Take Profit/Stop Loss Trend Following Strategy Based on EMA, Madrid Ribbon and Donchian Channel

- Multi-Indicator Trend Momentum Trading Strategy: An Optimized Quantitative Trading System Based on Bollinger Bands, Fibonacci and ATR

- Dynamic RSI-Price Divergence Detection and Adaptive Trading Strategy System

- Multi-Dimensional Trend Following Pyramid Trading Strategy

- Dual Timeframe Trend Reversal Candlestick Pattern Quantitative Trading Strategy

- High-Frequency Price-Volume Trend Following with Volume Analysis Adaptive Strategy

- Enhanced Price-Volume Trend Momentum Strategy

- Intelligent Moving Average Crossover Strategy with Dynamic Profit/Loss Management System

- Adaptive Multi-MA Momentum Breakthrough Trading Strategy

- Adaptive Momentum Mean-Reversion Crossover Strategy

- Adaptive Dual-Direction EMA Trend Trading System with Reverse Trade Optimization Strategy

- Dual EMA Pullback Trading System with ATR-Based Dynamic Stop-Loss Optimization

- Multi-Period Phase Crossover with EMA Trend Following Strategy

- Multi-Moving Average Cross Trend Following RSI Oscillation Strategy