Daily Open Reversal Strategy

Author: ChaoZhang, Date: 2024-01-26 14:35:22Tags:

Overview

The Daily Open Reversal Strategy is an intraday mean-reversion strategy based on the real body size of the previous candlestick to determine reversal opportunities in the current candlestick. It will trigger long or short trade signals if there is a significant gap between the open price of the current candlestick and the close price of the previous one, provided the real body size exceeds the threshold set in the parameters.

The best trading assets for this strategy are GBP and AUD daily charts, but other assets and timeframes can also be tested. The parameters include start and end dates, real body size of the previous candle, stop loss (in pips), and take profit (in pips).

Strategy Logic

The core logic behind Daily Open Reversal Strategy is to capture short-term overbought and oversold scenarios. Prices tend to retrace and correct after excessive movements in the market. This strategy aims to capitalize on such mean reversion tendency for profits.

Specifically, the strategy checks if there is a significant gap between the open price of the current candlestick and the close price of the previous one. If the real body size of the previous candle exceeds the threshold set in parameters, and the current candle shows an opening gap, long or short signals will be triggered. The long signal triggers when open > previous close with a down gap. The short signal triggers when open < previous close with an up gap.

Once entered into a position, stop loss and take profit levels are set. The position will be closed if hitting the stop loss level to control losses or take profit level to lock in gains.

Advantage Analysis

The Daily Open Reversal Strategy has the following key advantages:

- Capture market short-term reversals, higher profitability

It takes full advantage of short-term price reversals, opening positions after overbought/oversold scenarios for higher chance of gains.

- Controllable risk, effective stop loss to limit losses

The stop loss mechanism can effectively limit trading losses once they hit the preset maximum value.

- Flexibility across assets

It is applicable to various FX pairs, especially those volatile ones like GBP and AUD. Parameters can also be adjusted for optimization flexibility.

- Simplicity, suits intraday trading

With high trading frequency and short timeframe, it has simple and clear rules that fit intraday or day trading very well.

Risk Analysis

There are also some inherent risks in Daily Open Reversal Strategy:

- Trend continuation risks losses

Persistent one-sided trends increase the chance of failed reversals and thus losses.

- Higher trading costs

Increased number of trades can eat up gains due to more trading costs.

- Parameter optimization needed

Parameters like previous candle real body size, stop loss and take profit levels require sufficient optimization for best results.

- Close monitoring required

The short holding period requires close tracking of the markets for timely entries and stop losses.

Optimization Directions

The Daily Open Reversal Strategy can be optimized in the following aspects:

- Optimize parameters for best combination

Run backtests and demo trading to determine the optimal previous candle real body size, stop loss level, take profit level for higher efficiency.

- Incorporate multiple time frame analysis

Establish overall trend direction in higher timeframes to avoid counter-trend trades. Optimize specific entry and exit levels in lower timeframes.

- Enhance stop loss mechanisms

Employ volatility indicators to improve stop loss strategy for better protection in volatile markets, or trailing stop order etc.

- Add filters

Add filters like volume, volatility to ensure reversal signals are reliable enough to trade. Avoid unnecessary reverse trades.

- Improve position sizing

Optimize trade size and allocation to prevent oversized position leading to large losses. Experiment with gradual entries and exits to reduce risks.

Conclusion

The Daily Open Reversal is a typical short-term mean-reverting strategy that captures overbought and oversold scenarios for reverse trading. It has the advantage of controllable risks and simplicity. But trend continuation risk and high trading frequency should be noted. Further improvements can be made through parameter optimization, stop loss enhancement, adding filters and position sizing to boost its stability and profitability. It suits investors who prefer intraday trading.

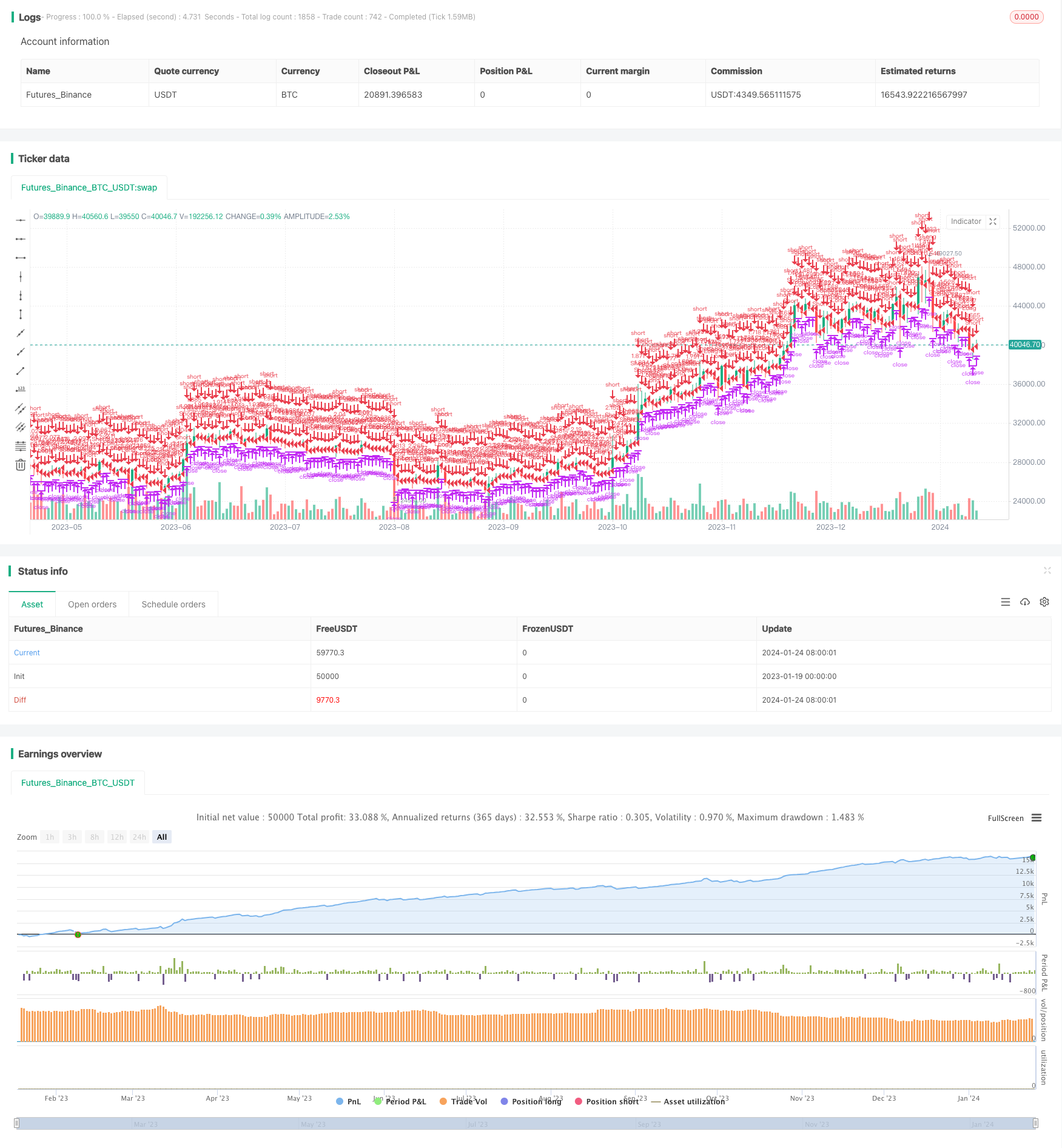

/*backtest

start: 2023-01-19 00:00:00

end: 2024-01-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=4

strategy("Daily Open Strategy", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital = 10000)

PrevRange = input(0.0100, type=input.float, title="Previous Candle Range")

TP = input(200, title="Take Profit in pips")

SL = input(1000, title="Stop Loss in pips")

startDate = input(title="Start Date", type=input.integer,

defval=1, minval=1, maxval=31)

startMonth = input(title="Start Month", type=input.integer,

defval=1, minval=1, maxval=12)

startYear = input(title="Start Year", type=input.integer,

defval=2015, minval=1800, maxval=2100)

endDate = input(title="End Date", type=input.integer,

defval=31, minval=1, maxval=31)

endMonth = input(title="End Month", type=input.integer,

defval=12, minval=1, maxval=12)

endYear = input(title="End Year", type=input.integer,

defval=2020, minval=1800, maxval=2100)

isLong = strategy.position_size > 0

isShort = strategy.position_size < 0

longTrigger = (open-close) > PrevRange and close<open

shortTrigger = (close-open) > PrevRange and close>open

inDateRange = true

strategy.entry(id = "Long", long = true, when = (longTrigger and not isShort and inDateRange))

strategy.exit("Exit Long", "Long", loss=SL, profit=TP)

strategy.entry(id = "Short", long = false, when = (shortTrigger and not isLong and inDateRange))

strategy.exit("Exit Short", "Short", loss=SL, profit=TP)

- Price Crossing Moving Average Trend Following Strategy

- Dual EMA Golden Cross Breakout Strategy

- Gradual BB KC Trend Strategy

- Triple SMA Auto-Tracking Strategy

- Bitcoin Futures Position Trading Strategy

- Price EMA with stochastic optimization based on machine learning

- Dynamic Bollinger Breakout Strategy

- Two Year New High Retracement Moving Average Strategy

- Dual Moving Average Trading Strategy

- Dynamic Position Rebalancing Trend Tracking System

- Golden Cross SMA Trading Strategy

- Golden Cross Moving Average Strategy

- MACD Crypto Trading Strategy

- Linear Regression and Dual Moving Average Short-Term Strategy

- Triple Overlapping Stochastic Momentum Strategy

- Momentum Trend Strategy

- Momentum Moving Average Crossover Quant Strategy

- Combination Strategy of Dual Moving Average Reversal and ATR Trailing Stop

- Leveraged Martingale Futures Trading Strategy

- Momentum Pullback Strategy