Enhanced Price-Volume Trend Momentum Strategy

Author: ChaoZhang, Date: 2025-01-10 15:40:37Tags: MACDATRMAEMASMA

Overview

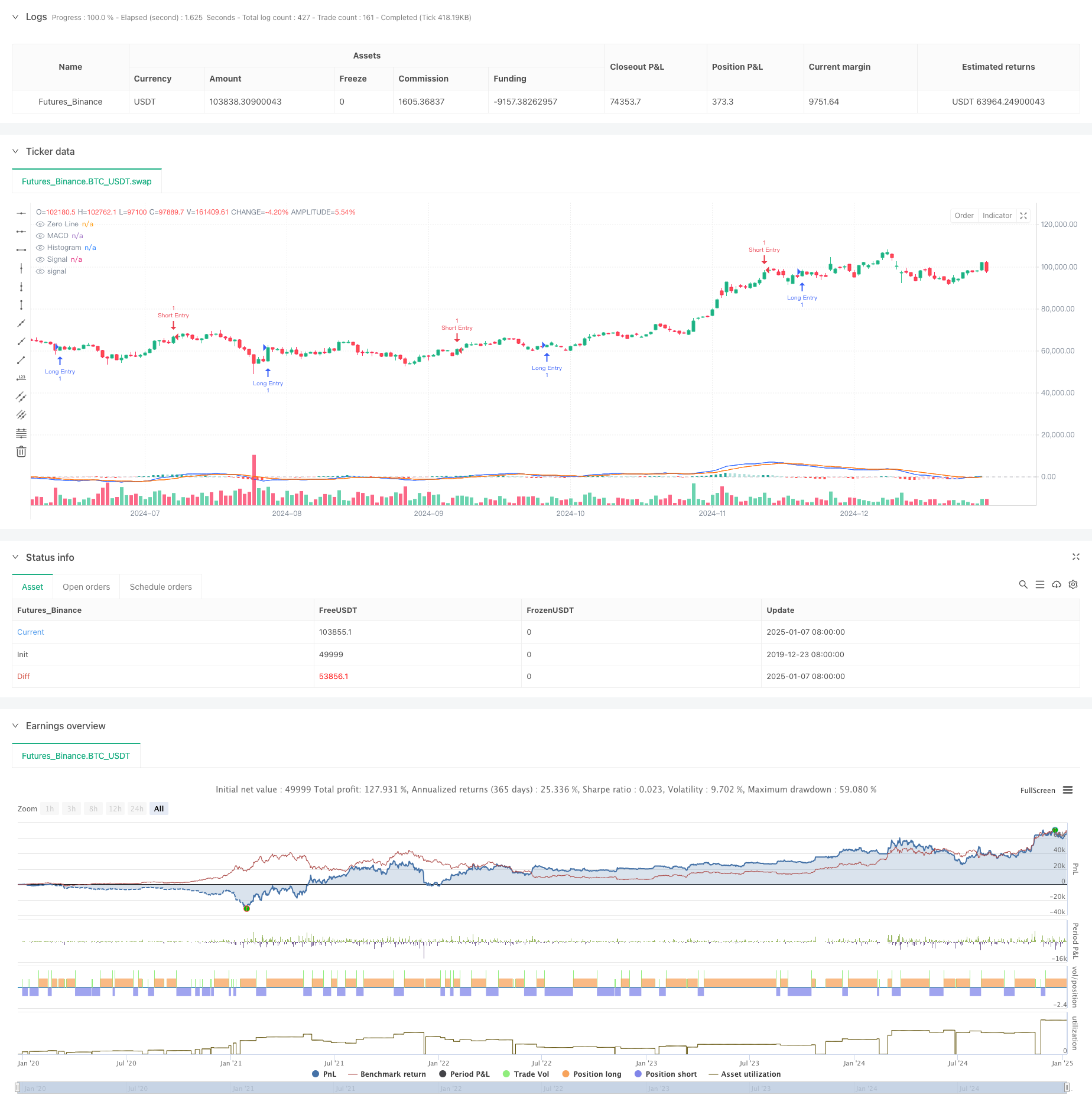

This strategy is a trading system based on MACD indicator and price-volume relationship, which identifies market trend reversal points by observing changes in MACD histogram patterns. The strategy employs a dynamic profit-taking and stop-loss mechanism using the ATR indicator to adapt to market volatility and effectively control risk.

Strategy Principle

The core logic of the strategy is built on the color changes of MACD histogram, combined with dual EMA and SMA moving average systems. When the MACD histogram transitions from dark to light color, it indicates a momentum shift, triggering the system to execute trades. Specifically: 1. Calculate MACD values using fast(12) and slow(26) moving averages 2. Smooth MACD with a 9-period signal line 3. Monitor color depth changes in MACD histogram 4. Set dynamic profit targets and stop losses using 14-period ATR

Strategy Advantages

- Scientific combination of indicators, with MACD effectively capturing trends and ATR adapting to volatility

- Flexible profit-taking and stop-loss settings adjustable through multiplier parameters for different market characteristics

- Clear trading signals with intuitive entry timing based on histogram color changes

- Accommodates both long and short trading, increasing strategy versatility and profit opportunities

Strategy Risks

- MACD as a lagging indicator may miss optimal entry points in rapid market movements

- May generate false signals in ranging markets, leading to frequent trading

- Improper ATR multiplier settings can result in stops being too loose or too tight

- Requires proper money management to avoid excessive single-trade losses

Strategy Optimization Directions

- Incorporate volume confirmation signals to improve signal reliability

- Add trend filters to reduce false signals in ranging markets

- Optimize profit-taking and stop-loss multipliers with dynamic adjustment based on different timeframes

- Include volatility filtering to reduce trading frequency during highly volatile periods

- Consider implementing time filters to avoid trading during unfavorable periods

Summary

This is a comprehensive strategy combining classic technical analysis indicator MACD with modern risk control methods. It captures market momentum shifts by observing MACD histogram pattern changes while using ATR for dynamic risk control. The strategy is well-designed with clear operational logic and practical value. Through continuous optimization and improvement, this strategy shows promise for better performance in real trading conditions.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-08 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=5

strategy(title="軒割MACD 空心量能不足策略", shorttitle="軒割MACD 空心量能不足策略", overlay=true)

//=== 1) 參數 ===//

fast_length = input.int(title="Fast Length", defval=12)

slow_length = input.int(title="Slow Length", defval=26)

src = input.source(title="MACD Source", defval=close)

signal_length = input.int(title="Signal Smoothing", defval=9, minval=1, maxval=50)

sma_source = input.string(title="Oscillator MA Type", defval="EMA", options=["SMA","EMA"])

sma_signal = input.string(title="Signal MA Type", defval="EMA", options=["SMA","EMA"])

// 啟用多單 / 空單

useLong = input.bool(title="啟用多單?(底部紅色)", defval=true)

useShort = input.bool(title="啟用空單?(頂部綠色)", defval=true)

// 止盈倍數 (1~10倍 ATR)

tpATRmult = input.int(title="止盈 ATR 倍數 (1~10)", defval=10, minval=1, maxval=500)

// 止損倍數 (1~10倍 ATR)

slATRmult = input.int(title="止損 ATR 倍數 (1~10)", defval=3, minval=1, maxval=500)

//=== 2) MACD 計算 ===//

fast_ma = sma_source == "SMA" ? ta.sma(src, fast_length) : ta.ema(src, fast_length)

slow_ma = sma_source == "SMA" ? ta.sma(src, slow_length) : ta.ema(src, slow_length)

macd = fast_ma - slow_ma

signal = sma_signal == "SMA" ? ta.sma(macd, signal_length) : ta.ema(macd, signal_length)

hist = macd - signal

//=== 3) 判斷深色/淺色(用於變化訊號)===//

darkGreen = hist >= 0 and hist <= hist[1] // 上方,柱子縮小或持平

lightGreen = hist >= 0 and hist > hist[1] // 上方,柱子變大

darkRed = hist < 0 and hist <= hist[1] // 下方,柱子(絕對值)變大或持平

lightRed = hist < 0 and hist > hist[1] // 下方,柱子(絕對值)變小

// 由「深 → 淺」是否發生在上一根

colorChangeToLightGreen = darkGreen[1] and lightGreen

colorChangeToLightRed = darkRed[1] and lightRed

//=== 4) ATR 計算 (用於止盈止損) ===//

atrPeriod = 14

atrValue = ta.atr(atrPeriod)

//=== 5) 多單策略:深紅 → 淺紅 (底部紅色) ===//

if useLong and colorChangeToLightRed

// 以當前 K 線 low - ATR倍數 作為多單止損

longStopLoss = low - (slATRmult * atrValue)

// 以當前 close + ATR倍數 作為多單止盈

longTakeProfit = close + (tpATRmult * atrValue)

// 進多單

strategy.entry("Long Entry", strategy.long, comment="多", qty=1)

strategy.exit("平多", "Long Entry", stop=longStopLoss, limit=longTakeProfit)

//=== 6) 空單策略:深綠 → 淺綠 (頂部綠色) ===//

if useShort and colorChangeToLightGreen

// 以當前 K 線 high + ATR倍數 作為空單止損

shortStopLoss = high + (slATRmult * atrValue)

// 以當前 close - ATR倍數 作為空單止盈

shortTakeProfit = close - (tpATRmult * atrValue)

// 進空單

strategy.entry("Short Entry", strategy.short, comment="空", qty=1)

strategy.exit("平空", "Short Entry", stop=shortStopLoss, limit=shortTakeProfit)

//=== 7) 繪製 MACD 與直方圖 ===//

hline(0, "Zero Line", color=color.new(#787B86, 50))

// 長條圖顏色:

// - 上方 (hist >= 0) 時:hist 比前一根大 (淺綠) 或小 (深綠)

// - 下方 (hist < 0) 時:hist 比前一根大 (淺紅) 或小 (深紅)

plot(hist,title="Histogram",style=plot.style_columns,color = hist >= 0? (hist > hist[1] ? #26A69A : #B2DFDB) : (hist > hist[1] ? #FFCDD2 : #FF5252) )

// 繪製 MACD 與 Signal

plot(macd, title="MACD", color=#2962FF)

plot(signal, title="Signal", color=#FF6D00)

- Multi-Indicator Fusion Mean Reversion Trend Following Strategy

- No Upper Wick Bullish Candle Breakout Strategy

- Elliott Wave Theory 4-9 Impulse Wave Automatic Detection Trading Strategy

- Triple Bottom Rebound Momentum Breakthrough Strategy

- Dual Moving Average MACD Crossover Date-Adjustable Quantitative Trading Strategy

- MACD and Martingale Combination Strategy for Optimized Long Trading

- MACD Multi-Interval Dynamic Stop-Loss and Take-Profit Trading System

- MACD-ATR-EMA Multi-Indicator Dynamic Trend Following Strategy

- Dynamic Moving Average Crossover Trend Following Strategy with ATR Risk Management System

- Dual EMA Trend Momentum Trading Strategy

- Multi-level Indicator Overlapping RSI Trading Strategy

- Bollinger Bands and Fibonacci Intraday Trend Following Strategy

- Dynamic Trend Following Dual Moving Average Channel Strategy with Risk Management System

- Multi-Mode Take Profit/Stop Loss Trend Following Strategy Based on EMA, Madrid Ribbon and Donchian Channel

- Multi-Indicator Trend Momentum Trading Strategy: An Optimized Quantitative Trading System Based on Bollinger Bands, Fibonacci and ATR

- Dynamic RSI-Price Divergence Detection and Adaptive Trading Strategy System

- Multi-Dimensional Trend Following Pyramid Trading Strategy

- Triple Bottom Rebound Momentum Breakthrough Strategy

- Dual Timeframe Trend Reversal Candlestick Pattern Quantitative Trading Strategy

- High-Frequency Price-Volume Trend Following with Volume Analysis Adaptive Strategy

- Intelligent Moving Average Crossover Strategy with Dynamic Profit/Loss Management System

- Adaptive Multi-MA Momentum Breakthrough Trading Strategy

- Adaptive Momentum Mean-Reversion Crossover Strategy

- Adaptive Dual-Direction EMA Trend Trading System with Reverse Trade Optimization Strategy

- Dual EMA Pullback Trading System with ATR-Based Dynamic Stop-Loss Optimization

- Multi-Period Phase Crossover with EMA Trend Following Strategy

- Multi-Moving Average Cross Trend Following RSI Oscillation Strategy

- Multi-Period Bollinger Bands Trend Breakout Strategy with Volatility Risk Control Model

- Dynamic Support and Resistance Adaptive Pivot Trading Strategy

- Dual EMA-RSI Divergence Strategy: A Trend Capture System Based on Exponential Moving Average and Relative Strength