Estrategia de negociación de media móvil dual basada en CMO y WMA

Descripción general

La estrategia es una estrategia de negociación de doble línea media basada en el indicador de movimiento de precios Chandre Movement Oscillator (CMO) y su media móvil ponderada (WMA). Attempts to identify trend reversals and continuation Using CMO crossover (WMA).

Principio de estrategia

La estrategia primero calcula el CMO, un indicador que mide el cambio de la dinámica en línea de los precios. Un valor positivo indica un impulso ascendente y un valor negativo indica un impulso descendente. Luego calcula el WMA del CMO.

Los pasos clave para calcular el CMO son:

- Calcula el cambio diario en el precio (xMom)

- El SMA de n días para el cambio de precio, como la dinámica de precios real de la moneda (xSMA_mom)

- Calcula el cambio de precio neto en n días (xMomLength)

- Para estandarizar el cambio de precio neto (nRes), el método es dividir por SMA

- Para estandarizar el cambio de precio neto, se solicita m días WMA, obteniendo CMO ((xWMACMO)

La ventaja de esta estrategia es que captura los puntos de inflexión de la tendencia de los precios a medio plazo. El tamaño absoluto del CMO refleja la intensidad de la tendencia de los precios, y la WMA es favorable para la ruptura de la hipótesis de la onda.

Análisis de las ventajas

La mayor ventaja de esta estrategia es que utiliza los valores absolutos de los indicadores de CMO para juzgar el sentimiento de las masas en el mercado, las ondas WMA para identificar los puntos de inflexión de las tendencias a mediano plazo. En comparación con la estrategia de media móvil única, es más capaz de capturar las tendencias a mediano plazo con más espacio de elasticidad.

El CMO estandariza los cambios de precio y los mapea en un rango de entre 100 y 100 para ayudar a juzgar el estado de ánimo de las masas en el mercado; el tamaño absoluto representa la intensidad de la tendencia actual. La WMA hace un filtro adicional sobre el CMO para evitar demasiadas señales falsas.

Análisis de riesgos

Los principales riesgos que podría tener esta estrategia son:

- Los parámetros CMO y WMA están mal configurados, lo que genera demasiadas señales falsas

- La incapacidad de responder eficazmente a la oscilación de las tendencias generará una frecuencia de negociación excesivamente alta y costos de deslizamiento.

- La incapacidad para identificar las tendencias reales a largo plazo y el riesgo de pérdidas en las posiciones a largo plazo

Los métodos de optimización son los siguientes:

- Ajustar los parámetros de CMO y WMA para encontrar la combinación óptima de parámetros

- Añadir condiciones de filtración adicionales, como el indicador de energía de volumen de transacción, para evitar el comercio en situaciones de crisis

- Combine indicadores de períodos más largos, como la línea de 90 días, para evitar pérdidas en tendencias largas

Dirección de optimización

El enfoque de optimización de la estrategia se centra en la optimización de parámetros, el filtrado de señales y el deterioro:

Optimización de parámetros de CMO y WMA: encontrar la combinación óptima de parámetros por recorrido

Filtración de señales en combinación con indicadores auxiliares como volumen de transacciones, indicadores de fortaleza y debilidad para evitar falsas rupturas

Aumentar el mecanismo de stop loss dinámico, que detiene la salida cuando el precio vuelve a caer por debajo de CMO y WMA

Se puede considerar el modelo de fracaso de ruptura como una señal de entrada, es decir, el CMO y el WMA que rompen el punto crítico primero, pero vuelven a caer rápidamente

Se puede combinar con indicadores de ciclo más largos para determinar la tendencia general y evitar la negociación en contra

Resumir

La estrategia en su conjunto utiliza los indicadores de CMO para determinar la fuerza de la tendencia y los puntos de inflexión, en combinación con WMA para generar señales de negociación de fluctuación, pertenece a un sistema típica de doble línea de equilibrio. En comparación con la estrategia de una sola MA, tiene la ventaja de una tendencia intermedia de captura de mayor elasticidad. Sin embargo, hay espacio para la optimización en la configuración de parámetros y fluctuación, el control adecuado de la frecuencia de negociación e introducir paros dinámicos, lo que puede mejorar aún más la estabilidad del sistema.

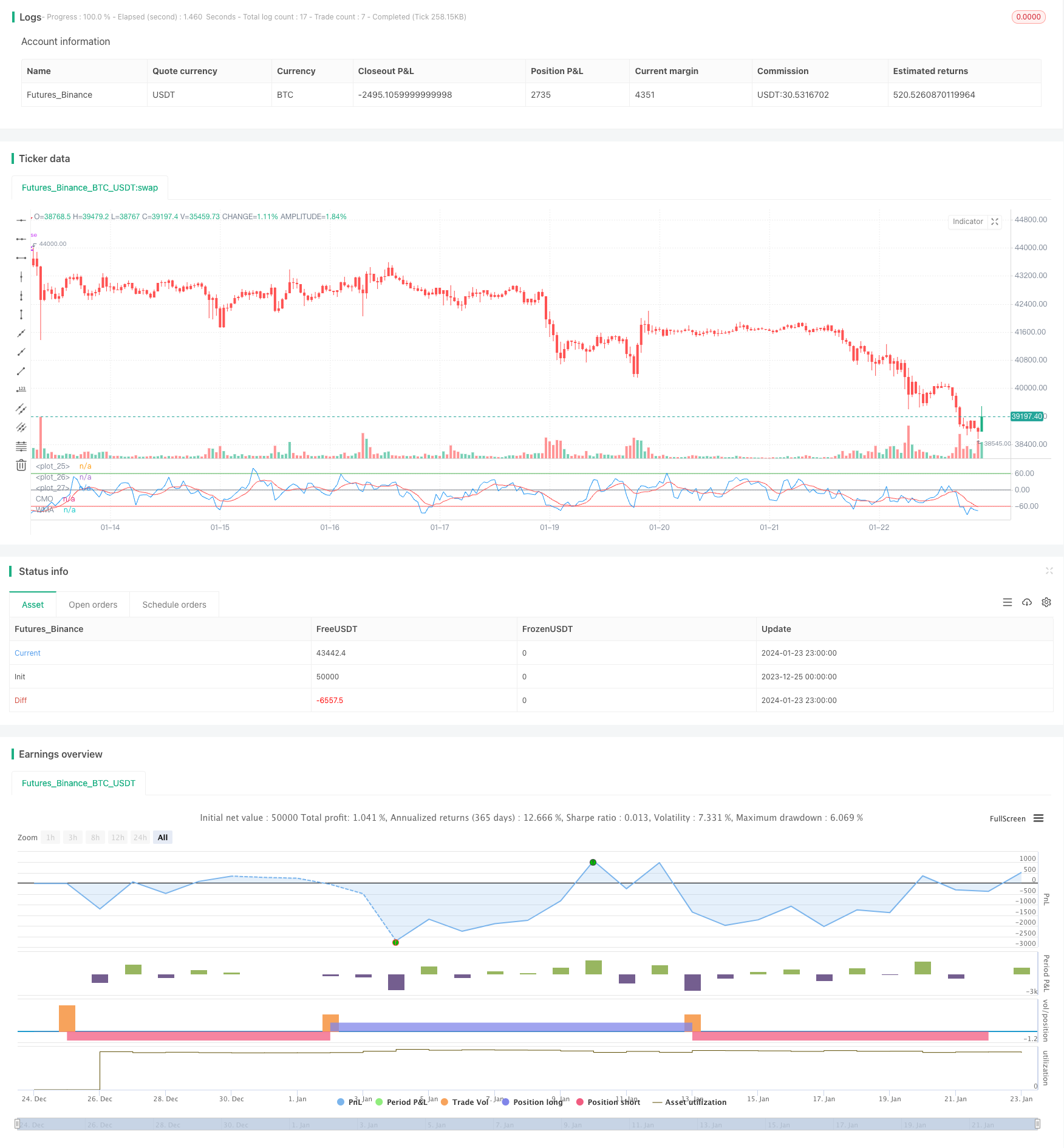

/*backtest

start: 2023-12-25 00:00:00

end: 2024-01-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 18/10/2018

// This indicator plots Chandre Momentum Oscillator and its WMA on the

// same chart. This indicator plots the absolute value of CMO.

// The CMO is closely related to, yet unique from, other momentum oriented

// indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

// etc. It is most closely related to Welles Wilder?s RSI, yet it differs

// in several ways:

// - It uses data for both up days and down days in the numerator, thereby

// directly measuring momentum;

// - The calculations are applied on unsmoothed data. Therefore, short-term

// extreme movements in price are not hidden. Once calculated, smoothing

// can be applied to the CMO, if desired;

// - The scale is bounded between +100 and -100, thereby allowing you to clearly

// see changes in net momentum using the 0 level. The bounded scale also allows

// you to conveniently compare values across different securities.

////////////////////////////////////////////////////////////

strategy(title="CMO & WMA Backtest ver 2.0", shorttitle="CMO & WMA")

Length = input(9, minval=1)

LengthWMA = input(9, minval=1)

BuyZone = input(60, step = 0.01)

SellZone = input(-60, step = 0.01)

reverse = input(false, title="Trade reverse")

hline(BuyZone, color=green, linestyle=line)

hline(SellZone, color=red, linestyle=line)

hline(0, color=gray, linestyle=line)

xMom = abs(close - close[1])

xSMA_mom = sma(xMom, Length)

xMomLength = close - close[Length]

nRes = 100 * (xMomLength / (xSMA_mom * Length))

xWMACMO = wma(nRes, LengthWMA)

pos = 0.0

pos := iff(xWMACMO > BuyZone, 1,

iff(xWMACMO < SellZone, -1, nz(pos[1], 0)))

possig = iff(reverse and pos == 1, -1,

iff(reverse and pos == -1, 1, pos))

if (possig == 1)

strategy.entry("Long", strategy.long)

if (possig == -1)

strategy.entry("Short", strategy.short)

barcolor(possig == -1 ? red: possig == 1 ? green : blue )

plot(nRes, color=blue, title="CMO")

plot(xWMACMO, color=red, title="WMA")