Advanced Composite Moving Average and Market Momentum Trend Capture Strategy

Author: ChaoZhang, Date: 2024-07-30 16:27:16Tags: HMAWMASMA

Overview

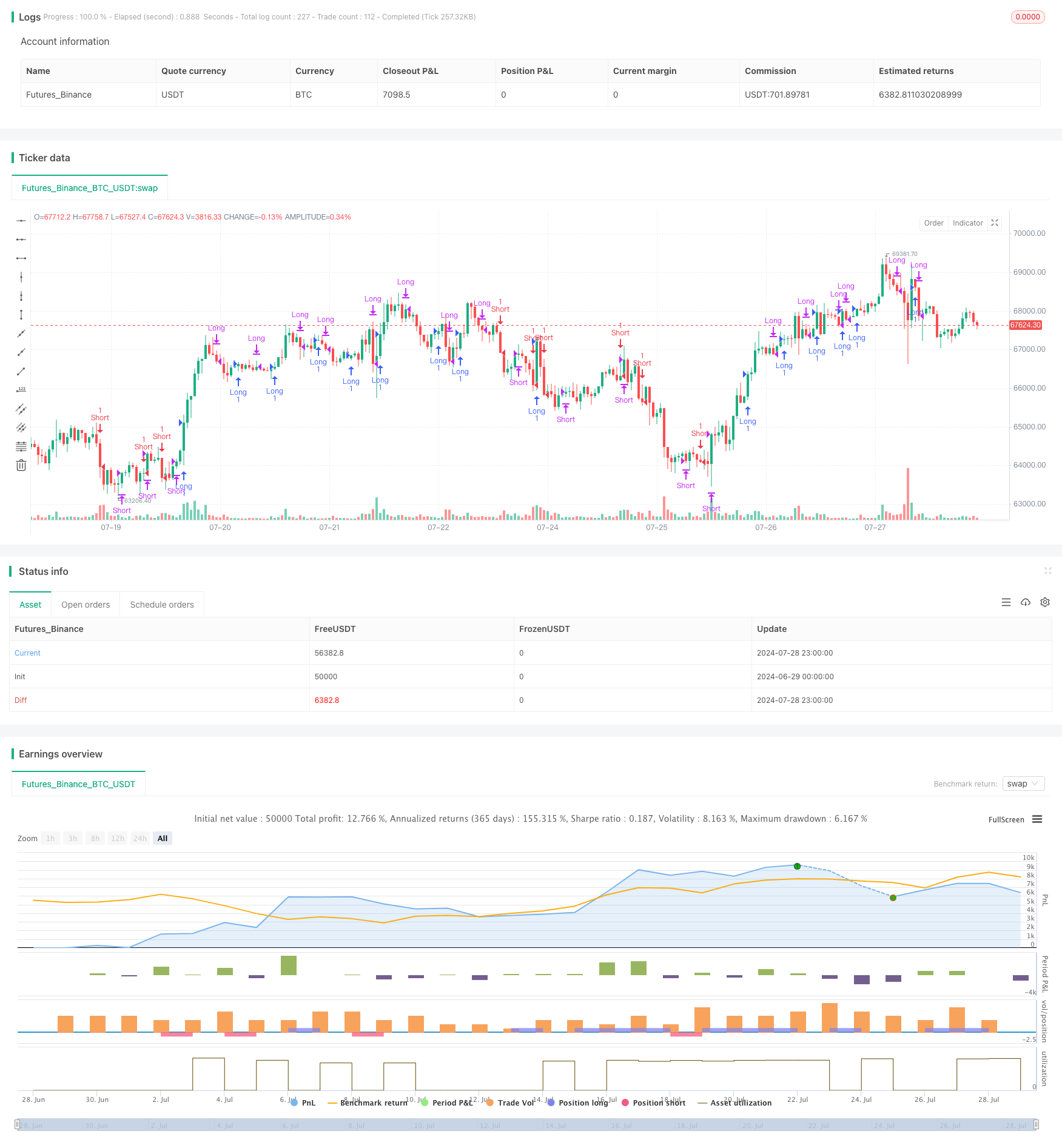

The Advanced Composite Moving Average and Market Momentum Trend Capture Strategy is a sophisticated trading system that combines multiple technical indicators. This strategy primarily utilizes the Hull Moving Average (HMA), Ichimoku Kinko Hyo, and Donchian Channel indicators to analyze price momentum and trend strength in order to identify potential trading opportunities. This approach aims to capture major market trends while filtering out short-term market noise, thereby improving trading accuracy and profitability.

Strategy Principle

The core of this strategy is to determine market trends by comparing Hull Moving Averages of different periods. The Hull Moving Average is an improved weighted moving average that responds more quickly to price changes and reduces lag. The strategy uses two Hull Moving Averages of different periods (n1 and n2) for cross-comparison to determine trend direction.

Simultaneously, the strategy incorporates multiple components of the Ichimoku Kinko Hyo, including the Conversion Line (Tenkan-sen), Base Line (Kijun-sen), Leading Span A (Senkou Span A), Leading Span B (Senkou Span B), and Lagging Span (Chikou Span). These indicators collectively provide a comprehensive analysis of market trends, support, and resistance levels.

Additionally, the strategy employs the Donchian Channel to calculate certain components within the Ichimoku Kinko Hyo, which helps identify price range volatility and potential breakout points.

Trade signals are generated based on a combination of the following conditions:

Long Entry Conditions:

- n1 > n2 (Hull Moving Average indicates an uptrend)

- Closing price > n2

- Closing price > Lagging Span

- Closing price > Leading Span high point

- Conversion Line >= Base Line or Closing price > Base Line

Short Entry Conditions:

- n1 < n2 (Hull Moving Average indicates a downtrend)

- Closing price < n2

- Closing price < Lagging Span

- Closing price < Leading Span low point

- Conversion Line <= Base Line or Closing price < Base Line

Long Exit Conditions:

- n1 < n2 or

- Closing price < n2 or

- Conversion Line < Base Line or

- Closing price < Conversion Line or

- Closing price < Base Line or

- Closing price < Leading Span high point or

- Closing price < Lagging Span

Short Exit Conditions:

- n1 > n2 or

- Closing price > n2 or

- Conversion Line > Base Line or

- Closing price > Conversion Line or

- Closing price > Base Line or

- Closing price > Leading Span low point or

- Closing price > Lagging Span

This combination of multiple conditions is designed to ensure that trade signals are triggered only when multiple technical indicators consistently point in the same direction, thereby increasing the reliability of trades.

Strategy Advantages

Multi-indicator Integration: By combining Hull Moving Average, Ichimoku Kinko Hyo, and Donchian Channel, the strategy can analyze the market from multiple perspectives, enhancing signal reliability.

Trend Following Capability: The use of Hull Moving Average allows the strategy to quickly capture trend changes, while Ichimoku Kinko Hyo provides insights into medium to long-term trends.

Noise Filtering: The setup of multiple conditions helps filter out short-term market noise, generating trade signals only when multiple indicators confirm together.

Dynamic Adaptability: The strategy’s parameters can be adjusted according to different market conditions, making it adaptable to various trading instruments and time frames.

Risk Management: By setting clear entry and exit conditions, the strategy helps control risk and avoid sustained losses in unfavorable market environments.

Comprehensive Market Perspective: Ichimoku Kinko Hyo provides predictions of potential future market directions, aiding traders in making more forward-looking decisions.

Objectivity: The strategy is based on clear mathematical models and technical indicators, reducing the impact of subjective judgment on trading decisions.

Strategy Risks

Over-optimization Risk: The strategy uses multiple parameters, and excessive optimization of these parameters to fit historical data may lead to poor future performance.

Lag Risk: Although Hull Moving Average reduces lag, all strategies based on moving averages still have a certain degree of lag, which may result in significant drawdowns during trend reversals.

False Breakout Risk: In ranging markets, the strategy may generate multiple false breakout signals, leading to frequent trading and unnecessary costs.

Market Environment Dependency: This strategy performs well in strong trend markets but may underperform in oscillating markets or markets with rapid reversals.

Parameter Sensitivity: The strategy’s performance may be highly sensitive to parameter settings, with different parameter combinations potentially leading to significantly different results.

Computational Complexity: The strategy uses multiple complex technical indicators, which may cause delays or execution issues in real-time trading.

Overtrading Risk: While the multiple condition setup increases signal reliability, it may also reduce trading opportunities, affecting overall returns.

Strategy Optimization Directions

Dynamic Parameter Adjustment: Implement a dynamic parameter adjustment mechanism that automatically adjusts Hull Moving Average and Ichimoku Kinko Hyo parameters based on market volatility and trend strength to adapt to different market environments.

Incorporate Machine Learning Algorithms: Utilize machine learning techniques such as Support Vector Machines (SVM) or Random Forests to optimize the signal generation process and improve prediction accuracy.

Integrate Fundamental Analysis: Introduce fundamental factors, such as economic data releases or company earnings reports, on top of technical analysis to enhance the comprehensiveness of trading decisions.

Improve Risk Management: Implement dynamic stop-loss and profit target settings that automatically adjust risk management parameters based on market volatility and trend strength.

Multi-timeframe Analysis: Introduce multi-timeframe analysis to ensure trade direction aligns with larger timeframe trends, reducing the risk of counter-trend trading.

Volatility Filtering: Add volatility indicators, such as Average True Range(ATR), to reduce trading frequency during low volatility periods and avoid trading in unclear market environments.

Sentiment Analysis Integration: Introduce market sentiment indicators, such as the VIX fear index or social media sentiment analysis, to capture the psychological state of market participants and improve timing of trades.

Optimize Computational Efficiency: Use more efficient algorithms or parallel computing techniques to optimize the strategy’s computational process, reducing latency in real-time trading.

Summary

The Advanced Composite Moving Average and Market Momentum Trend Capture Strategy is a comprehensive trading system that aims to accurately capture market trends and provide reliable trading signals by integrating multiple technical indicators including Hull Moving Average, Ichimoku Kinko Hyo, and Donchian Channel. The strategy’s strengths lie in its ability to analyze the market from multiple angles and its sensitivity to trend changes. However, it also faces risks such as over-optimization and market environment dependency.

Through continuous optimization and improvement, such as introducing dynamic parameter adjustment, machine learning algorithms, and multi-timeframe analysis, this strategy has the potential to become a more robust and adaptive trading system. Future development should focus on enhancing the strategy’s flexibility and intelligence to better cope with ever-changing market environments.

Overall, this strategy provides traders with a powerful tool for capturing market trends and managing risks. However, like all trading strategies, it is not infallible. When using this strategy, traders still need to combine their own market insights and risk management principles to achieve long-term stable trading performance.

//@version=4

strategy("Private Strategy TradingView", shorttitle="Private Strategy TradingView", overlay=true)

keh = input(title="Double HullMA", type=input.integer, defval=12, minval=1)

n2ma = 2 * wma(close, round(keh / 2))

nma = wma(close, keh)

diff = n2ma - nma

sqn = round(sqrt(keh))

n2ma1 = 2 * wma(close[1], round(keh / 2))

nma1 = wma(close[1], keh)

diff1 = n2ma1 - nma1

sqn1 = round(sqrt(keh))

n1 = wma(diff, sqn)

n2 = wma(diff1, sqn)

TenkanSenPeriods = input(9, minval=1, title="Tenkan Sen Periods")

KijunSenPeriods = input(24, minval=1, title="Kijun Sen Periods")

SenkouSpanBPeriods = input(51, minval=1, title="Senkou Span B Periods")

displacement = input(24, minval=1, title="Displacement")

donchian(len) => avg(lowest(low, len), highest(high, len))

TenkanSen = donchian(TenkanSenPeriods)

KijunSen = donchian(KijunSenPeriods)

SenkouSpanA = avg(TenkanSen, KijunSen)

SenkouSpanB = donchian(SenkouSpanBPeriods)

SenkouSpanH = max(SenkouSpanA[displacement - 1], SenkouSpanB[displacement - 1])

SenkouSpanL = min(SenkouSpanA[displacement - 1], SenkouSpanB[displacement - 1])

ChikouSpan = close[displacement - 1]

longCondition = n1 > n2 and close > n2 and close > ChikouSpan and close > SenkouSpanH and (TenkanSen >= KijunSen or close > KijunSen)

if (longCondition)

strategy.entry("Long", strategy.long)

shortCondition = n1 < n2 and close < n2 and close < ChikouSpan and close < SenkouSpanL and (TenkanSen <= KijunSen or close < KijunSen)

if (shortCondition)

strategy.entry("Short", strategy.short)

closelong = n1 < n2 and (close < n2 or TenkanSen < KijunSen or close < TenkanSen or close < KijunSen or close < SenkouSpanH or close < ChikouSpan)

if (closelong)

strategy.close("Long")

closeshort = n1 > n2 and (close > n2 or TenkanSen > KijunSen or close > TenkanSen or close > KijunSen or close > SenkouSpanL or close > ChikouSpan)

if (closeshort)

strategy.close("Short")

- RedK Momentum Bars

- Advanced Flexible Multi-Period Moving Average Crossover Strategy

- Optimized Multi-Timeframe HMA Quantitative Trading Strategy with Dynamic Stop-Loss

- Momentum-based ZigZag

- RSI and MA Combination Strategy

- Multi-Indicator Dynamic Moving Average Crossover Quantitative Strategy

- VWMA-ADX Momentum and Trend-Based Bitcoin Long Strategy

- Hull Moving Average Swing Trader

- Dual Hull Moving Average Crossover Quantitative Strategy

- Multi-Timeframe Hull Moving Average Crossover Strategy

- Multi-EMA Crossover Momentum Strategy

- Multi-Order Breakout Trend Following Strategy

- Multi-EMA Crossover with Time Interval Integration Strategy

- Dual Moving Average Crossover Confirmation Strategy with Volume-Price Integration Optimization Model

- Dual Dynamic Indicator Optimization Strategy

- VWAP Crossover Dynamic Profit Target Trading Strategy

- Bollinger Bands Breakout Quantitative Trading Strategy

- Fibonacci Extension and Retracement Channel Breakout Strategy

- Multi-Dimensional Order Flow Analysis and Trading Strategy

- Multi-Moving Average Trend Following and Reversal Pattern Recognition Strategy

- Advanced Fibonacci Retracement and Volume-Weighted Price Action Trading Strategy

- Adaptive Standard Deviation Breakout Trading Strategy: Multi-Period Optimization System Based on Dynamic Volatility

- Dynamic Position Dual Moving Average Crossover Strategy

- Dynamic Signal Line Trend Following Strategy Combining ATR and Volume

- Multi-Indicator Dynamic Volatility Alert Trading System

- Dynamic Trend-Following Trading Strategy Based on Gann Angles

- VWAP-ATR Trend Following and Price Reversal Strategy

- Bollinger Bands RSI Neutral Market Quantitative Trading Strategy

- Multi-Level Oversold Oscillator Buy Strategy

- Adaptive Trend Following Strategy Combining AlphaTrend and KAMA with Risk Management