概述

单边趋势震荡突破策略(Single Side Trend Shock Breakout Strategy)是一个利用价格通道和趋势判断的突破策略。它旨在识别趋势方向,在震荡区间突破入场,达到设置的获利目标后退出。

策略原理

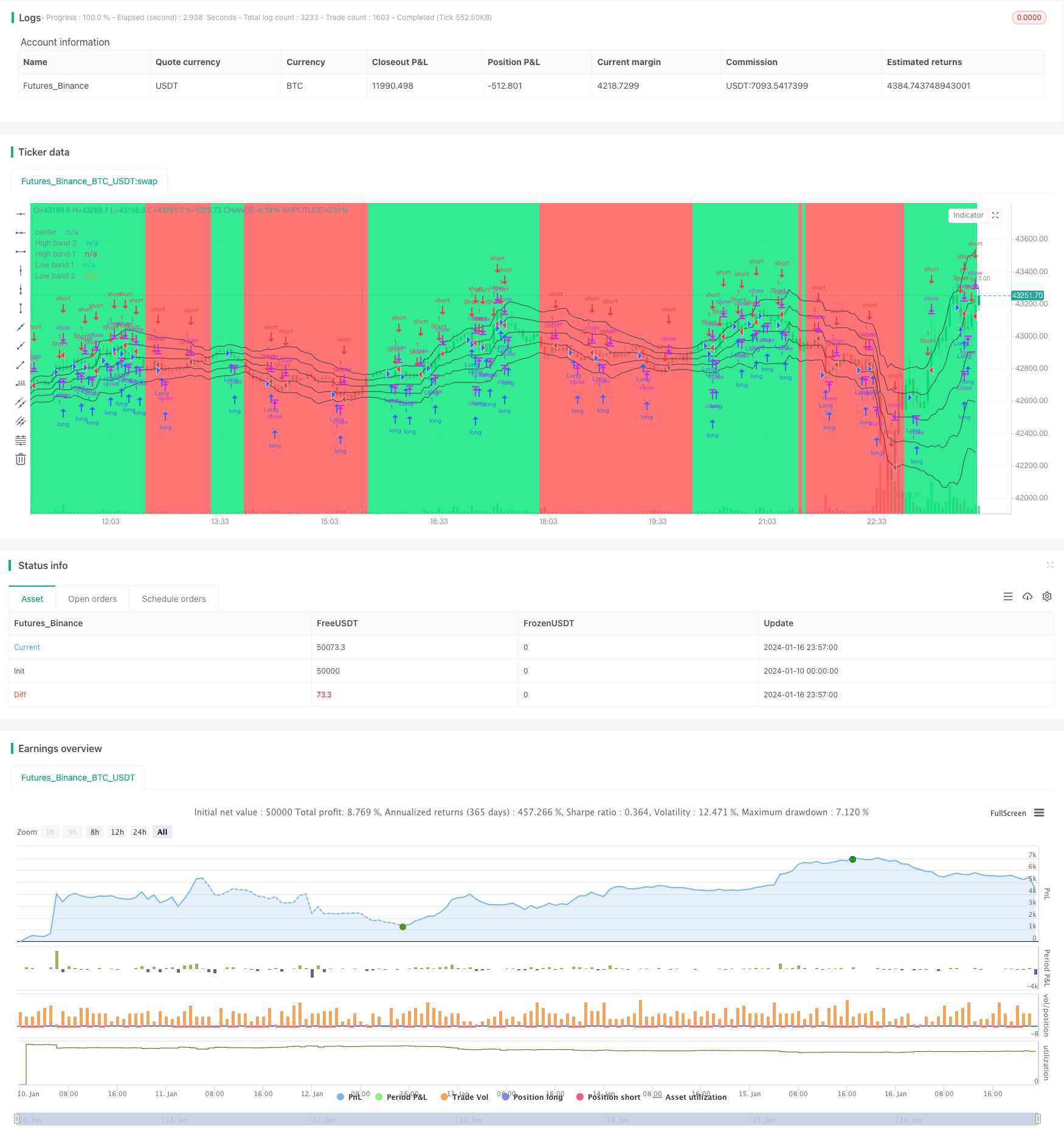

该策略通过计算价格通道的上下轨,判断价格是否突破通道进行操作。具体来说,策略首先计算最近N周期的最高价、最低价,并计算价格中线。然后计算价格与中线的平均绝对距离,得到上下轨。

在判断趋势时,策略检查最近几根K线是否全部收于通道之上(多头信号)或通道之下(空头信号)。当判断到趋势后,strategy等待价格震荡,在通道上轨或下轨附近突破形成信号,采取反向入场的方式进入场内。

此外,策略还会判断K线实体突破,作为补充的入场信号。当实体长度突破平均实体长度的一定倍数时 Generates signal. 策略会在入场后设置一个获利目标,当价格达到目标时主动止盈。

优势分析

该策略有以下几个优势:

- 利用价格通道判断趋势方向,可以减少假突破的概率

- 反向入场,可在趋势震荡的时候获利

- 实体突破作为补充信号,提高入场精确度

- 设置止盈目标,可以主动止盈

风险分析

该策略也存在一些风险:

- 价格通道参数设置不当,可能导致通道范围太大或太小

- 强势趋势中反向操作可能造成较大亏损

- 实体突破容易形成头假信号

- 止盈设置不当,可能损失部分利润

为了降低风险,可以调整参数缩小通道范围,避免强势趋势中反向建仓,优化止盈逻辑等。

优化方向

该策略还可以从以下几个方向进行优化:

- 增加趋势判断指标,确保趋势判断准确性

- 优化实体突破的参数,降低头假信号率

- 结合更多指标过滤入场时机

- 动态调整止盈位置

总结

单边趋势震荡突破策略通过价格通道和趋势判断,在震荡区间反向建仓的方法获利。它有判断趋势、止盈主动的优点,但也存在一定风险。通过多指标确认,参数优化等手段可以减少风险提高盈利空间。该策略适用于短线交易,可以作为趋势策略的补充。

策略源码

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("Noro's Bands Scalper Strategy v1.5", shorttitle = "Scalper str 1.5", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

//Settings

needlong = input(true, defval = true, title = "Long")

needshort = input(true, defval = true, title = "Short")

takepercent = input(0, defval = 0, minval = 0, maxval = 1000, title = "take, %")

needbe = input(true, defval = true, title = "Bands Entry")

needct = input(false, defval = false, title = "Counter-trend entry")

bodylen = input(10, defval = 10, minval = 0, maxval = 50, title = "Body length")

trb = input(1, defval = 1, minval = 1, maxval = 5, title = "Trend bars")

len = input(20, defval = 20, minval = 2, maxval = 200, title = "Period")

needbb = input(true, defval = true, title = "Show Bands")

needbg = input(true, defval = true, title = "Show Background")

src = close

//PriceChannel 1

lasthigh = highest(src, len)

lastlow = lowest(src, len)

center = (lasthigh + lastlow) / 2

//Distance

dist = abs(src - center)

distsma = sma(dist, len)

hd = center + distsma

ld = center - distsma

hd2 = center + distsma * 2

ld2 = center - distsma * 2

//Trend

chd = close > hd

cld = close < ld

uptrend = trb == 1 and chd ? 1 : trb == 2 and chd and chd[1] ? 1 : trb == 3 and chd and chd[1] and chd[2] ? 1 : trb == 4 and chd and chd[1] and chd[2] and chd[3] ? 1 : trb == 5 and chd and chd[1] and chd[2] and chd[3] and chd[4] ? 1 : 0

dntrend = trb == 1 and cld ? 1 : trb == 2 and cld and cld[1] ? 1 : trb == 3 and cld and cld[1] and cld[2] ? 1 : trb == 4 and cld and cld[1] and cld[2] and cld[3] ? 1 : trb == 5 and cld and cld[1] and cld[2] and cld[3] and cld[4] ? 1 : 0

trend = dntrend == 1 and high < center ? -1 : uptrend == 1 and low > center ? 1 : trend[1]

//trend = close < ld and high < center ? -1 : close > hd and low > center ? 1 : trend[1]

//Lines

colo = needbb == false ? na : black

plot(hd2, color = colo, linewidth = 1, transp = 0, title = "High band 2")

plot(hd, color = colo, linewidth = 1, transp = 0, title = "High band 1")

plot(center, color = colo, linewidth = 1, transp = 0, title = "center")

plot(ld, color = colo, linewidth = 1, transp = 0, title = "Low band 1")

plot(ld2, color = colo, linewidth = 1, transp = 0, title = "Low band 2")

//Background

col = needbg == false ? na : trend == 1 ? lime : red

bgcolor(col, transp = 80)

//Body

body = abs(close - open)

smabody = ema(body, 30) / 10 * bodylen

//Signals

bar = close > open ? 1 : close < open ? -1 : 0

up7 = trend == 1 and ((bar == -1 and bar[1] == -1) or (body > smabody and bar == -1)) ? 1 : 0

dn7 = trend == 1 and ((bar == 1 and bar[1] == 1) or (close > hd and needbe == true)) and close > strategy.position_avg_price * (100 + takepercent) / 100 ? 1 : 0

up8 = trend == -1 and ((bar == -1 and bar[1] == -1) or (close < ld2 and needbe == true)) and close < strategy.position_avg_price * (100 - takepercent) / 100 ? 1 : 0

dn8 = trend == -1 and ((bar == 1 and bar[1] == 1) or (body > smabody and bar == 1)) ? 1 : 0

if up7 == 1 or up8 == 1

strategy.entry("Long", strategy.long, needlong == false ? 0 : trend == -1 and needct == false ? 0 : na)

if dn7 == 1 or dn8 == 1

strategy.entry("Short", strategy.short, needshort == false ? 0 : trend == 1 and needct == false ? 0 : na)