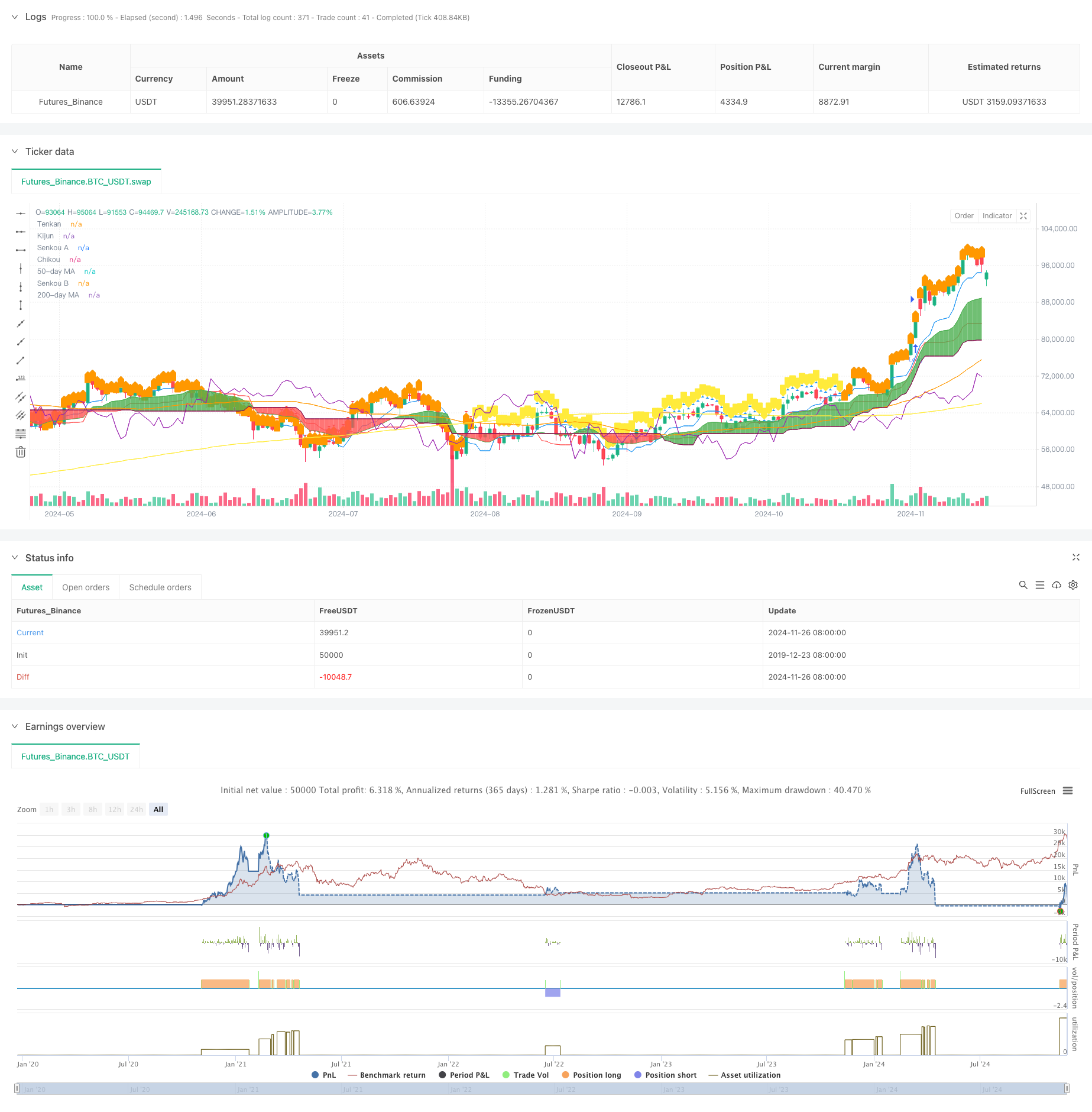

Überblick

Die Strategie ist ein vollständiges Handelssystem, das eine Reihe von technischen Indikatoren kombiniert, um Handelsentscheidungen zu treffen, die hauptsächlich auf den Indikatoren der Ichimoku Cloud basieren. Das System ermittelt den Einstiegsmoment durch die Kreuzung der Antenne Tenkan mit der Basislinie Kijun, während der relativ starke Index RSI und der Moving Average Ma als unterstützende Filterbedingungen verwendet werden. Die Strategie verwendet die Cloud-Komponente als dynamische Stop-Loss-Position und bildet ein vollständiges Risikokontrollsystem.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Schlüsselelementen:

- Das Eingangssignal wird durch die Kreuzung der Antenne mit der Basislinie erzeugt, wobei das obere Durchschnittssignal als Mehrsignal und das untere Durchschnittssignal als Leerzeichen gebildet wird.

- Die Beziehung zwischen der Preisposition und der Wolke (Kumo) als Trendbestätigung, der Preis über der Wolke und der Preis unter der Wolke

- Die Positionsbeziehung zwischen 50- und 200-Tage-Moving Averages als Trendfilterbedingungen

- Der Kreis-RSI als Bestätigung der Marktstärke und Filterung falscher Signale

- Nutzung der oberen und unteren Grenze der Cloud als dynamische Stop-Loss-Position, um das dynamische Risikomanagement zu ermöglichen

Strategische Vorteile

- Die Kombination von mehreren technischen Indikatoren bietet zuverlässigere Handelssignale und reduziert die Auswirkungen von Falschsignalen erheblich

- Die Verwendung von Cloud Charts als dynamische Stop-Loss-Position, die automatisch die Stop-Loss-Position an die Marktbewegung anpassen kann, um sowohl die Gewinne zu schützen als auch den Preisen genügend Spielraum zu geben

- Durch die Umlauf-RSI-Filterung wird ein ungünstiger Handel in einem übertrieben überkauften Bereich vermieden.

- Die Kreuzung von Moving Averages bietet zusätzliche Trendbestätigung und erhöht die Erfolgsrate des Handels.

- Ein vollständiges Risikokontrollsystem, das Eintritts-, Haltungs- und Ausstiegssysteme umfasst

Strategisches Risiko

- Mehrfache Filterung könnte dazu führen, dass potenzielle Chancen verpasst werden

- In einem volatilen Markt können häufig falsche Ausbruchssignale auftreten

- Der Cloud Graph Index selbst hat eine gewisse Verzögerung, die den Eintritt beeinträchtigen könnte.

- In einem schnelllebigen Markt könnte ein dynamischer Stop-Loss zu locker sein

- Zu viele Filterbedingungen können zu weniger Handelsmöglichkeiten führen und die Gesamtergebnisse der Strategie beeinträchtigen

Richtung der Strategieoptimierung

- Einführung eines Volatilitätsindikators, der die Strategieparameter an Marktschwankungen anpasst

- Optimierung der Parameter-Einstellungen der Cloud Graph, um sie für unterschiedliche Marktumgebungen zu optimieren

- Erhöhung der Analyse der Transaktionsvolumen und der Signalsicherheit

- Einführung eines Zeitfiltermechanismus, um schwankende Zeiträume zu vermeiden

- Entwickeln Sie anpassungsfähige Parameteroptimierungssysteme, um eine dynamische Anpassung der Strategie zu ermöglichen

Zusammenfassen

Die Strategie baut durch die Kombination mehrerer technischer Kennzahlen ein vollständiges Handelssystem auf. Die Strategie konzentriert sich nicht nur auf die Erzeugung von Signalen, sondern enthält auch eine ausgezeichnete Risikokontrolle. Durch die Einstellung mehrerer Filterbedingungen wird die Erfolgsrate des Handels wirksam erhöht.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-27 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Strategy with Optional RSI, MA Filters and Alerts", overlay=true)

// Input for date and time filter

startDate = input(timestamp("2020-01-01 00:00"), title="Start Date")

endDate = input(timestamp("2023-01-01 00:00"), title="End Date")

// Inputs for Ichimoku settings

tenkanPeriod = input.int(9, title="Tenkan Period")

kijunPeriod = input.int(26, title="Kijun Period")

senkouBPeriod = input.int(52, title="Senkou B Period")

// Inputs for Moving Average settings

useMAFilter = input.bool(true, title="Enable Moving Average Filter?")

ma50Period = input.int(50, title="50-day MA Period")

ma200Period = input.int(200, title="200-day MA Period")

// Inputs for RSI settings

useRSIFilter = input.bool(true, title="Enable RSI Filter?")

rsiPeriod = input.int(14, title="RSI Period")

rsiOverbought = input.int(70, title="RSI Overbought Level")

rsiOversold = input.int(30, title="RSI Oversold Level")

// Ichimoku Cloud components

tenkan = (ta.highest(high, tenkanPeriod) + ta.lowest(low, tenkanPeriod)) / 2

kijun = (ta.highest(high, kijunPeriod) + ta.lowest(low, kijunPeriod)) / 2

senkouA = ta.sma(tenkan + kijun, 2) / 2

senkouB = (ta.highest(high, senkouBPeriod) + ta.lowest(low, senkouBPeriod)) / 2

chikou = close[26]

// Moving Averages

ma50 = ta.sma(close, ma50Period)

ma200 = ta.sma(close, ma200Period)

// Weekly RSI

rsiSource = request.security(syminfo.tickerid, "W", ta.rsi(close, rsiPeriod))

// Plotting the Ichimoku Cloud components

pTenkan = plot(tenkan, color=color.blue, title="Tenkan")

pKijun = plot(kijun, color=color.red, title="Kijun")

pSenkouA = plot(senkouA, color=color.green, title="Senkou A")

pSenkouB = plot(senkouB, color=color.maroon, title="Senkou B")

plot(chikou, color=color.purple, title="Chikou")

plot(ma50, color=color.orange, title="50-day MA")

plot(ma200, color=color.yellow, title="200-day MA")

// Corrected fill function

fill(pSenkouA, pSenkouB, color=senkouA > senkouB ? color.green : color.red, transp=90)

// Debugging: Output values on the chart to see if conditions are ever met

plotshape(series=(tenkan > kijun), color=color.blue, style=shape.triangleup, title="Tenkan > Kijun")

plotshape(series=(tenkan < kijun), color=color.red, style=shape.triangledown, title="Tenkan < Kijun")

plotshape(series=(ma50 > ma200), color=color.orange, style=shape.labelup, title="MA 50 > MA 200")

plotshape(series=(ma50 < ma200), color=color.yellow, style=shape.labeldown, title="MA 50 < MA 200")

// Define the trailing stop loss using Kumo

var float trailingStopLoss = na

// Check for MA conditions (apply only if enabled)

maConditionLong = not useMAFilter or (useMAFilter and ma50 > ma200)

maConditionShort = not useMAFilter or (useMAFilter and ma50 < ma200)

// Check for Ichimoku Cloud conditions

ichimokuLongCondition = close > math.max(senkouA, senkouB)

ichimokuShortCondition = close < math.min(senkouA, senkouB)

// Check for RSI conditions (apply only if enabled)

rsiConditionLong = not useRSIFilter or (useRSIFilter and rsiSource > rsiOverbought)

rsiConditionShort = not useRSIFilter or (useRSIFilter and rsiSource < rsiOversold)

// Combine conditions for entry

longCondition = maConditionLong and tenkan > kijun and ichimokuLongCondition and rsiConditionLong

shortCondition = maConditionShort and tenkan < kijun and ichimokuShortCondition and rsiConditionShort

// Date and time filter

withinDateRange = true

// Check for Long Condition

if (longCondition and withinDateRange)

strategy.entry("Long", strategy.long)

trailingStopLoss := math.min(senkouA, senkouB)

alert("Buy Signal: Entering Long Position", alert.freq_once_per_bar_close)

// Check for Short Condition

if (shortCondition and withinDateRange)

strategy.entry("Short", strategy.short)

trailingStopLoss := math.max(senkouA, senkouB)

alert("Sell Signal: Entering Short Position", alert.freq_once_per_bar_close)

// Exit conditions

exitLongCondition = close < kijun or tenkan < kijun

exitShortCondition = close > kijun or tenkan > kijun

if (exitLongCondition and strategy.position_size > 0)

strategy.close("Long")

alert("Exit Signal: Closing Long Position", alert.freq_once_per_bar_close)

if (exitShortCondition and strategy.position_size < 0)

strategy.close("Short")

alert("Exit Signal: Closing Short Position", alert.freq_once_per_bar_close)

// Apply trailing stop loss

if (strategy.position_size > 0)

strategy.exit("Trailing Stop Long", stop=trailingStopLoss)

else if (strategy.position_size < 0)

strategy.exit("Trailing Stop Short", stop=trailingStopLoss)