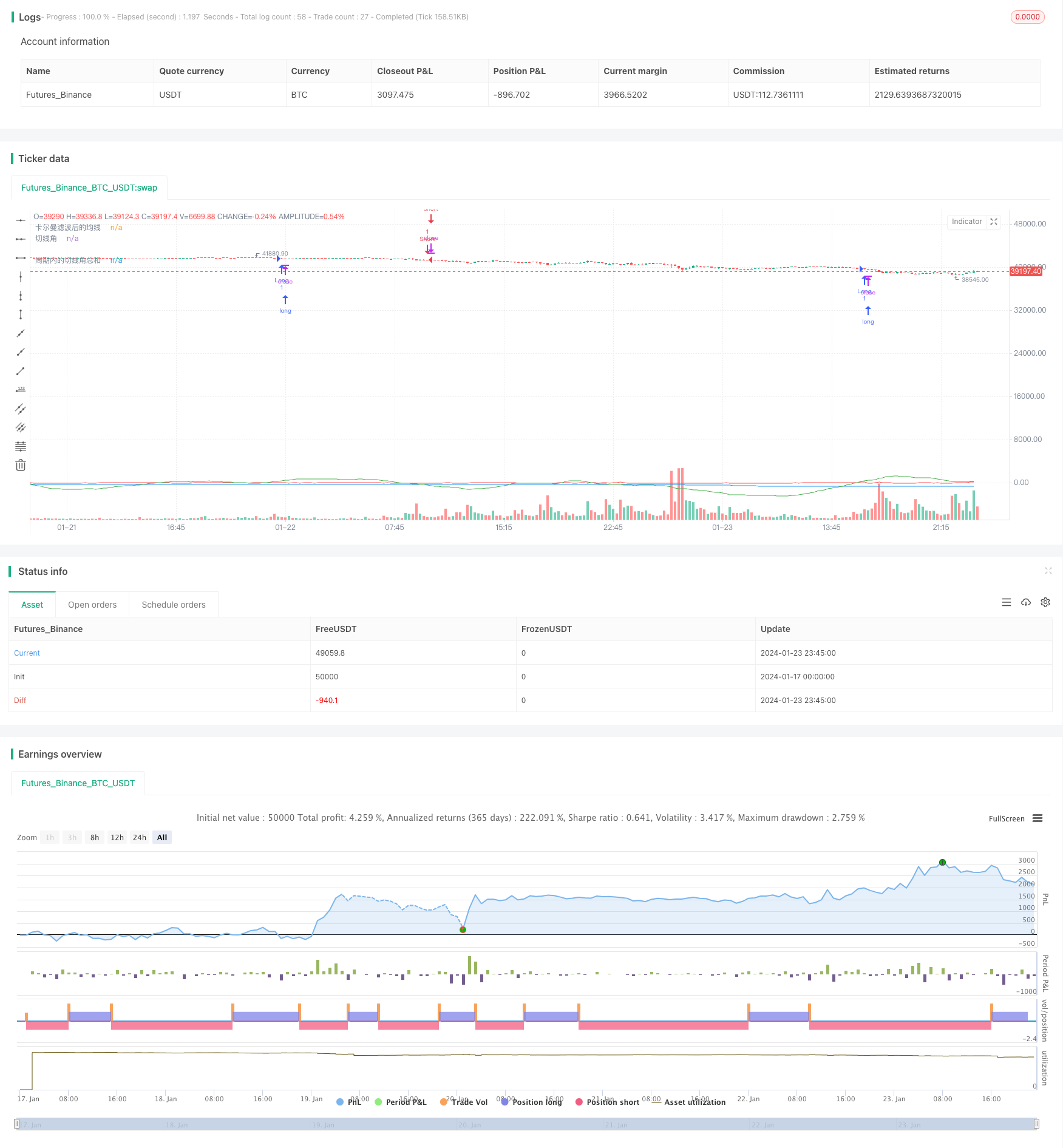

Overview

The core of this strategy is to use Kalman filter technology to smooth the price moving average, and generate trading signals when the tangent angle of the smoothed moving average exceeds a certain threshold within a specified period. The strategy aims to track medium and long term trends by using Kalman filter technology to reduce the impact of noise, so as to obtain clearer and more reliable trend signals.

Strategy Principle

The core logic of this strategy mainly includes the following steps:

Calculate the simple moving average (SMA) of the 1-minute price as the original moving average;

Kalman filter the original moving average to output a smoothed moving average;

Calculate the tangent angle of the smoothed moving average;

Define the parameter period and statistically sum the tangent angles within the period;

Generate a buy signal when the sum of tangent angles within the period is greater than 360 degrees; generate a sell signal when less than -360 degrees.

With this design, when the price shows an upward or downward trend, the tangent angle of the moving average will gradually accumulate. When it accumulates to a certain extent, trading signals will be generated. Therefore, it can effectively track medium and long term trends.

Among them, the Kalman filter is the key. The Kalman filter is a recursive algorithm that predicts the value of process noise and measurement noise while predicting the current state, and uses these noise values to correct the prediction of the current state to obtain a more accurate and reliable state estimation.

In this strategy, the SMA of the price can be seen as the measurement of the state. Affected by market noise, the Kalman filter will recursively estimate the true trend of prices, greatly reduce the impact of noise, make the subsequent moving average calculation more reliable, and thus produce more stable and accurate trading signals.

Advantage Analysis

Compared with simple moving average and other technical indicator strategies, the biggest advantage of this strategy is that it uses Kalman filter to reduce the impact of noise, making trading signals clearer and more reliable. The specific advantages are mainly reflected in the following aspects:

Reduce false signals. Kalman filtering effectively filters out a lot of false signals caused by random fluctuations by adaptively estimating and eliminating noise, making the trading signals generated more reliable.

Better tracking effect. The smoothed moving average shape is smoother and better reflects the medium and long term trend of prices, thus achieving better trend tracking effect.

Flexible adjustable parameters. Adjustable parameters include the length of moving average, parameters of Kalman filter and statistical cycle, which can flexibly adapt to different market environments.

Controllable risk. This strategy focuses more on medium and long term trends rather than short term fluctuations, achieving good risk-return balance.

Easy to implement and expand. The core algorithm of this strategy is quite concise and easy to implement and test. It also provides room for expansion, such as introducing machine learning algorithms to automatically optimize parameters.

Risk Analysis

The main risks of this strategy also include:

Trend reversal risk. This strategy focuses on trend tracking. In case of a sharp trend reversal, it will lead to greater losses. This can be mitigated by appropriately shortening the statistical cycle to reduce per trade loss.

Parameter optimization risk. Inappropriate parameter settings may lead to frequent trading or signal lagging. It requires sufficient testing and optimization. It can be combined with machine learning algorithms for automatic optimization.

Over-optimization risk. Excessive optimization on historical data may also lead to ineffective parameters. Out-of-sample validity needs to be controlled.

Increased complexity risk. Introducing Kalman filter and tangent angle algorithms increases code complexity. Correct implementation needs to be ensured.

Optimization Directions

Considering the above risks, the optimization directions of this strategy include:

Introduce stop loss and position sizing. Appropriate stop loss can effectively control the risk of single trade loss; dynamic position sizing can also adjust positions to hedge risks according to market conditions.

Automatic parameter optimization. Machine learning optimization algorithms can achieve automatic parameter optimization to avoid over-optimization risks.

Integrate other indicators. Some other indicators can be integrated into the strategy to form indicator combinations to enhance strategy stability.

Increase efficiency evaluation. Introduce more risk-adjusted metrics to evaluate the efficiency and stability of strategies for a more comprehensive and accurate conclusion.

Expand to more products. If effective, it can be considered to expand to more products. In the medium and long term, it accumulates richer samples and facilitates cross-product parameter optimization.

Conclusion

In general, this strategy is a relatively simple and practical trend tracking strategy. Compared with traditional moving average strategies, the introduction of the Kalman filter algorithm is its biggest innovation point, which also enables the strategy to produce clearer and more reliable trading signals. With further optimization, this strategy is expected to achieve better results. Overall, this strategy provides a new idea for quantitative trading strategies and is worth further research and application.

/*backtest

start: 2024-01-17 00:00:00

end: 2024-01-24 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//@library=math

strategy("策略360°(测试)", overlay=true)

// 定义1分钟均线

ma1 = request.security(syminfo.tickerid, "1", ta.sma(close, 1)) // 在这里使用了 math.sma() 函数

//plot(ma1, color=color.yellow, title="原始均线")

// 定义卡尔曼滤波函数,参考了[1](https://www.tradingview.com/pine-script-docs/en/v5/language/Methods.html)和[2](https://www.tradingview.com/pine-script-docs/en/v5/language/Operators.html)的代码

kalman(x, g) =>

kf = 0.0

dk = x - nz(kf[1], x) // 在这里使用了 nz() 函数

smooth = nz(kf[1], x) + dk * math.sqrt(g * 2) // 在这里使用了 math.sqrt() 函数

velo = 0.0

velo := nz(velo[1], 0) + g * dk // 在这里使用了 nz() 函数

kf := smooth + velo

kf

// 定义卡尔曼滤波后的均线

ma2 = kalman(ma1, 0.01)

plot(ma2, color=color.blue, title="卡尔曼滤波后的均线")

// 定义切线角

angle = math.todegrees(math.atan(ma2 - ma2[1])) // 在这里使用了 math.degrees() 和 math.atan() 函数

// 定义累加的切线角

cum_angle = 0.0

cum_angle := nz(cum_angle[1], 0) + angle // 在这里使用了 nz() 函数

// 定义30分钟周期

period = 30 // 您可以根据您的需要修改这个参数

// 定义周期内的切线角总和

sum_angle = 0.0

sum_angle := math.sum(angle, period) // 在这里使用了 math.sum() 函数,把周期内的切线角总和改成简单地把 5 个切线角相加

// 定义买入和卖出条件

buy = sum_angle > 360// 在这里使用了 math.radians() 函数

sell = sum_angle < -360

// 执行买入和卖出操作

strategy.entry("Long", strategy.long, when=buy)

strategy.close("Short", when=buy)

strategy.entry("Short", strategy.short, when=sell)

strategy.close("Long", when=sell)

// 绘制曲线图

plot(sum_angle, color=color.green, title="周期内的切线角总和")

plot(angle, color=color.red, title="切线角") // 这是我为您添加的代码,用于显示实时计算的切线角