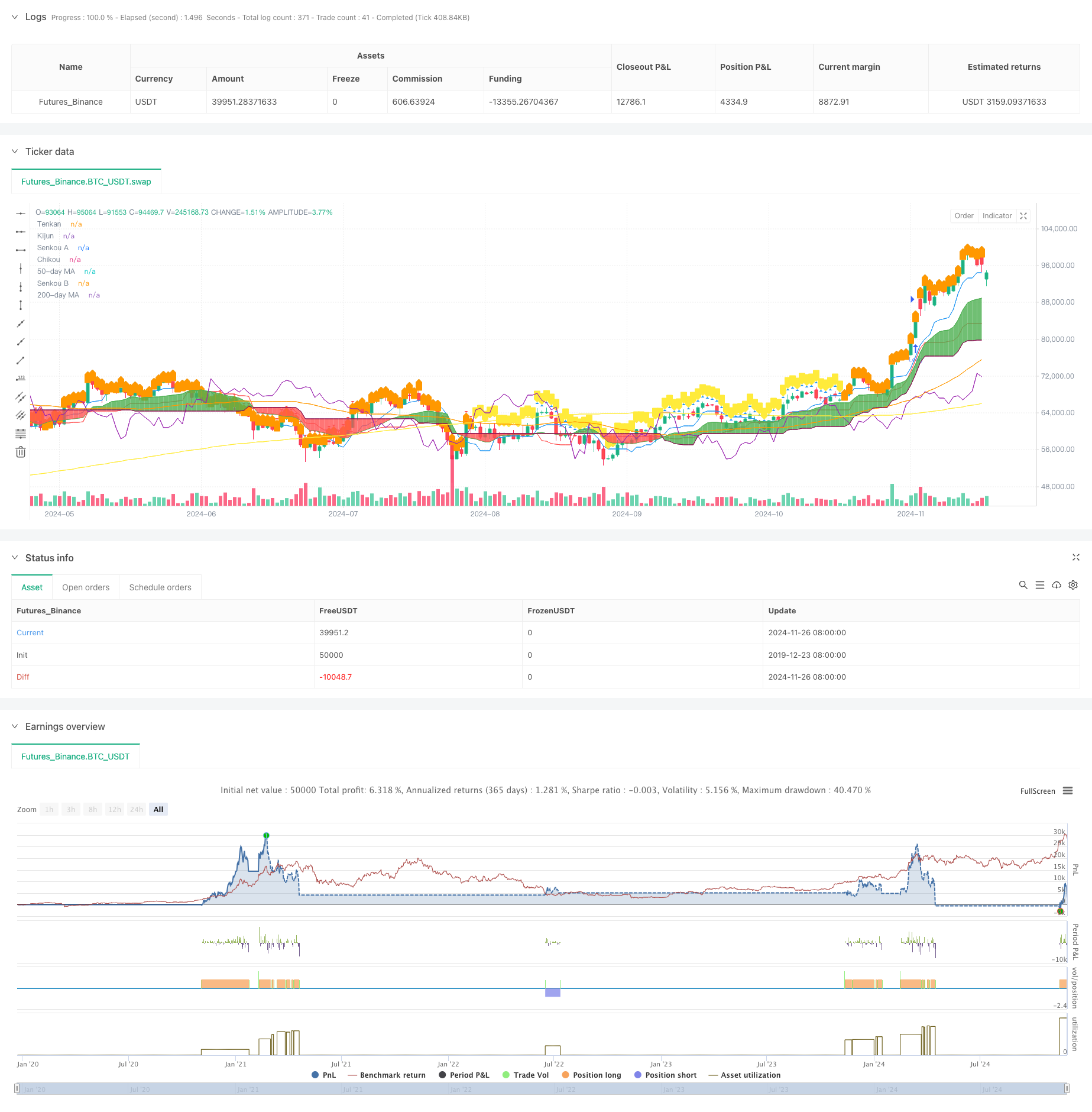

概要

この戦略は,一連の技術指標を組み合わせた完全な取引システムであり,主に一目瞭然のIchimoku Cloud指標に基づいて取引決定を行う.このシステムは,アンテナのTenkanとベースラインのKijunの交差によって入場タイミングを決定し,比較的強い指数 (RSI) と移動平均のMAを補助的なフィルタリング条件として組み合わせている.この戦略は,ダイナミックなストップ・ローズとしてクラウドの構成要素を採用し,完全なリスク制御システムを形成する.

戦略原則

戦略の中核となるロジックは、次の主要な要素に基づいています。

- 入場信号はアンテナと基准線の交差によって生成され,上穿は多信号で,下穿は空白信号で形成される

- 価格の位置と雲の関係 (Kumo) 傾向確認として,価格が雲の上の多し,価格が雲の下の空し

- 50日間の移動平均と200日間の移動平均の位置関係がトレンドフィルター条件として

- 周回RSIは市場の強弱を確認し,偽信号をフィルターする

- 雲層の上下境界を動的ストップロージャとして使用し,リスクの動的管理を実現する.

戦略的優位性

- 複数の技術指標の組み合わせにより,より信頼性の高い取引信号が提供され,偽信号の影響が著しく減少しました.

- ダイナミックなストップポイントとしてクラウドグラフを使用し,市場の波動に応じて自動的にストップポジションを調整し,利益を保護し,価格に十分な波動空間を与えることができます.

- 周回 RSI フィルタリングにより,過剰な超買いと超売り領域での不利な取引を効果的に回避します.

- 移動平均の交差は,トレンドの確認と取引の成功率を高めます.

- 入場,保有,出場の各節を含む完全なリスク管理システム

戦略リスク

- 複数の指標をフィルタリングすると,潜在的に良い機会を逃してしまう可能性があります.

- 不安定な市場では、誤ったブレイクアウトシグナルが頻繁に発生する可能性がある

- クラウドグラフの指標自体は遅滞しており,入学時期に影響を及ぼす可能性がある.

- ダイナミックなストップは,急激に波動する市場において,過度に緩やかになる可能性があります.

- 過剰なフィルタリング条件は,取引機会の減少につながり,戦略の全体的な利益に影響を与える可能性があります.

戦略最適化の方向性

- 波動率指標を導入し,市場の波動に応じて戦略パラメータを調整する

- 異なる市場環境に適したクラウドマップのパラメータ設定を最適化

- 取引量分析と信号の信頼性を向上させる

- タイムフィルタリングを導入し,波動的な時間帯を避けます.

- 戦略の動的調整を実現する自己適応のパラメータ最適化システムを開発

要約する

この戦略は,複数の技術指標を組み合わせて,完全な取引システムを構築している. この戦略は,信号の生成に注力するだけでなく,完全なリスク制御機構も含んでいる. 複数のフィルタリング条件の設定により,取引の成功率を効果的に向上させている. 同時に,ダイナミックな止損設計は,戦略に良好なリスク/利益の比率も提供している. いくつかの最適化の余地があるが,全体的には構造が整った,論理的に明確な戦略システムである.

ストラテジーソースコード

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-27 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Strategy with Optional RSI, MA Filters and Alerts", overlay=true)

// Input for date and time filter

startDate = input(timestamp("2020-01-01 00:00"), title="Start Date")

endDate = input(timestamp("2023-01-01 00:00"), title="End Date")

// Inputs for Ichimoku settings

tenkanPeriod = input.int(9, title="Tenkan Period")

kijunPeriod = input.int(26, title="Kijun Period")

senkouBPeriod = input.int(52, title="Senkou B Period")

// Inputs for Moving Average settings

useMAFilter = input.bool(true, title="Enable Moving Average Filter?")

ma50Period = input.int(50, title="50-day MA Period")

ma200Period = input.int(200, title="200-day MA Period")

// Inputs for RSI settings

useRSIFilter = input.bool(true, title="Enable RSI Filter?")

rsiPeriod = input.int(14, title="RSI Period")

rsiOverbought = input.int(70, title="RSI Overbought Level")

rsiOversold = input.int(30, title="RSI Oversold Level")

// Ichimoku Cloud components

tenkan = (ta.highest(high, tenkanPeriod) + ta.lowest(low, tenkanPeriod)) / 2

kijun = (ta.highest(high, kijunPeriod) + ta.lowest(low, kijunPeriod)) / 2

senkouA = ta.sma(tenkan + kijun, 2) / 2

senkouB = (ta.highest(high, senkouBPeriod) + ta.lowest(low, senkouBPeriod)) / 2

chikou = close[26]

// Moving Averages

ma50 = ta.sma(close, ma50Period)

ma200 = ta.sma(close, ma200Period)

// Weekly RSI

rsiSource = request.security(syminfo.tickerid, "W", ta.rsi(close, rsiPeriod))

// Plotting the Ichimoku Cloud components

pTenkan = plot(tenkan, color=color.blue, title="Tenkan")

pKijun = plot(kijun, color=color.red, title="Kijun")

pSenkouA = plot(senkouA, color=color.green, title="Senkou A")

pSenkouB = plot(senkouB, color=color.maroon, title="Senkou B")

plot(chikou, color=color.purple, title="Chikou")

plot(ma50, color=color.orange, title="50-day MA")

plot(ma200, color=color.yellow, title="200-day MA")

// Corrected fill function

fill(pSenkouA, pSenkouB, color=senkouA > senkouB ? color.green : color.red, transp=90)

// Debugging: Output values on the chart to see if conditions are ever met

plotshape(series=(tenkan > kijun), color=color.blue, style=shape.triangleup, title="Tenkan > Kijun")

plotshape(series=(tenkan < kijun), color=color.red, style=shape.triangledown, title="Tenkan < Kijun")

plotshape(series=(ma50 > ma200), color=color.orange, style=shape.labelup, title="MA 50 > MA 200")

plotshape(series=(ma50 < ma200), color=color.yellow, style=shape.labeldown, title="MA 50 < MA 200")

// Define the trailing stop loss using Kumo

var float trailingStopLoss = na

// Check for MA conditions (apply only if enabled)

maConditionLong = not useMAFilter or (useMAFilter and ma50 > ma200)

maConditionShort = not useMAFilter or (useMAFilter and ma50 < ma200)

// Check for Ichimoku Cloud conditions

ichimokuLongCondition = close > math.max(senkouA, senkouB)

ichimokuShortCondition = close < math.min(senkouA, senkouB)

// Check for RSI conditions (apply only if enabled)

rsiConditionLong = not useRSIFilter or (useRSIFilter and rsiSource > rsiOverbought)

rsiConditionShort = not useRSIFilter or (useRSIFilter and rsiSource < rsiOversold)

// Combine conditions for entry

longCondition = maConditionLong and tenkan > kijun and ichimokuLongCondition and rsiConditionLong

shortCondition = maConditionShort and tenkan < kijun and ichimokuShortCondition and rsiConditionShort

// Date and time filter

withinDateRange = true

// Check for Long Condition

if (longCondition and withinDateRange)

strategy.entry("Long", strategy.long)

trailingStopLoss := math.min(senkouA, senkouB)

alert("Buy Signal: Entering Long Position", alert.freq_once_per_bar_close)

// Check for Short Condition

if (shortCondition and withinDateRange)

strategy.entry("Short", strategy.short)

trailingStopLoss := math.max(senkouA, senkouB)

alert("Sell Signal: Entering Short Position", alert.freq_once_per_bar_close)

// Exit conditions

exitLongCondition = close < kijun or tenkan < kijun

exitShortCondition = close > kijun or tenkan > kijun

if (exitLongCondition and strategy.position_size > 0)

strategy.close("Long")

alert("Exit Signal: Closing Long Position", alert.freq_once_per_bar_close)

if (exitShortCondition and strategy.position_size < 0)

strategy.close("Short")

alert("Exit Signal: Closing Short Position", alert.freq_once_per_bar_close)

// Apply trailing stop loss

if (strategy.position_size > 0)

strategy.exit("Trailing Stop Long", stop=trailingStopLoss)

else if (strategy.position_size < 0)

strategy.exit("Trailing Stop Short", stop=trailingStopLoss)