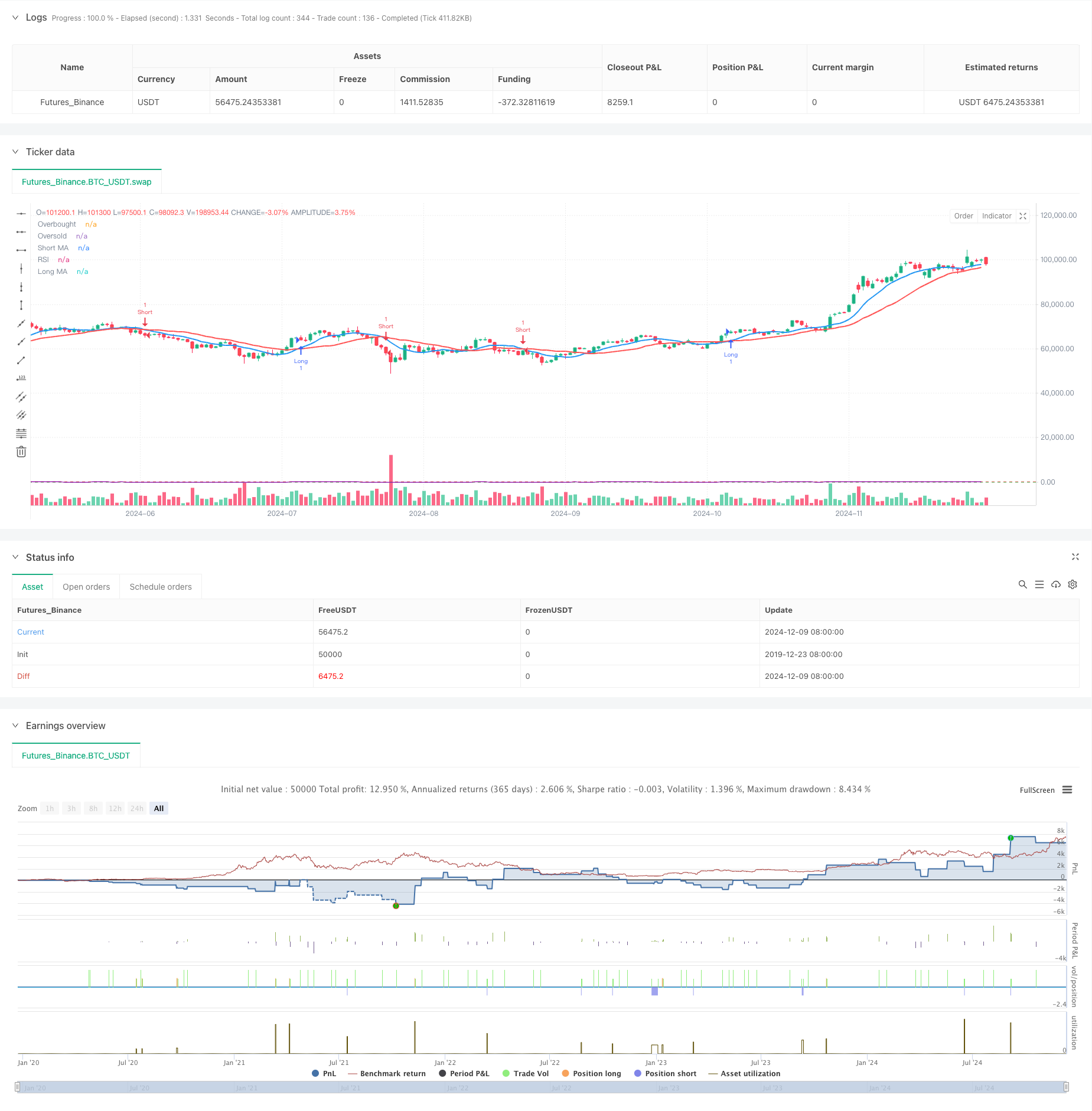

概述

这是一个结合均线交叉和相对强弱指标(RSI)的趋势跟踪策略。该策略通过短期和长期移动平均线的交叉来确定市场趋势方向,同时使用RSI作为动量过滤器来确认趋势的强度,从而提高交易信号的可靠性。策略还包含了百分比止损和止盈来进行风险管理。

策略原理

策略使用9周期和21周期的简单移动平均线(SMA)作为主要趋势指标。当短期均线向上穿越长期均线且RSI大于50时,系统产生做多信号;当短期均线向下穿越长期均线且RSI小于50时,系统产生做空信号。这种设计确保了交易方向与市场趋势和动量保持一致。系统通过设置1%的止损和2%的止盈来控制每笔交易的风险回报比。

策略优势

- 结合均线和RSI的双重确认机制提高了信号的可靠性。

- 使用百分比止损止盈,风险管理更加灵活和适应性强。

- 参数可调整性强,能够适应不同市场环境和交易品种。

- 策略逻辑简单明确,易于理解和维护。

- 通过RSI过滤减少了假突破带来的损失。

策略风险

- 在震荡市场中可能产生频繁的假信号。

- 固定百分比的止损可能在波动性较大的市场中不够灵活。

- 均线系统存在滞后性,可能错过最佳入场点。

- RSI指标在极端市场条件下可能失效。

- 需要仔细优化参数以适应不同市场环境。

策略优化方向

- 引入自适应的止损止盈机制,根据市场波动性动态调整。

- 添加成交量指标作为辅助确认信号。

- 优化均线周期选择,可考虑使用指数移动平均线(EMA)提高灵敏度。

- 引入趋势强度过滤器,在横盘市场自动降低仓位或暂停交易。

- 增加时间过滤器,避免在市场开盘和收盘时段交易。

总结

这是一个结构完整、逻辑清晰的趋势跟踪策略。通过均线交叉提供基本的趋势方向,RSI提供动量确认,再配合风险管理机制,形成了一个完整的交易系统。虽然存在一些固有的局限性,但通过持续优化和调整,该策略有望在不同市场环境下保持稳定的表现。策略的成功关键在于参数优化和风险控制的执行。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Moving Average Crossover + RSI Strategy", overlay=true, shorttitle="MA RSI Strategy")

// --- Input Parameters ---

shortMA = input.int(9, title="Short MA Period", minval=1)

longMA = input.int(21, title="Long MA Period", minval=1)

rsiLength = input.int(14, title="RSI Length", minval=1)

rsiOverbought = input.int(70, title="RSI Overbought Level", minval=50, maxval=100)

rsiOversold = input.int(30, title="RSI Oversold Level", minval=0, maxval=50)

stopLossPercent = input.float(1, title="Stop Loss Percentage", minval=0.1, maxval=10.0) / 100

takeProfitPercent = input.float(2, title="Take Profit Percentage", minval=0.1, maxval=10.0) / 100

// --- Calculate Moving Averages ---

shortMA_value = ta.sma(close, shortMA)

longMA_value = ta.sma(close, longMA)

// --- Calculate RSI ---

rsi_value = ta.rsi(close, rsiLength)

// --- Buy and Sell Conditions ---

longCondition = ta.crossover(shortMA_value, longMA_value) and rsi_value > 50

shortCondition = ta.crossunder(shortMA_value, longMA_value) and rsi_value < 50

// --- Plot Moving Averages ---

plot(shortMA_value, color=color.blue, linewidth=2, title="Short MA")

plot(longMA_value, color=color.red, linewidth=2, title="Long MA")

// --- Plot RSI (Optional) ---

hline(rsiOverbought, "Overbought", color=color.red)

hline(rsiOversold, "Oversold", color=color.green)

plot(rsi_value, color=color.purple, title="RSI")

// --- Strategy Execution ---

if (longCondition)

strategy.entry("Long", strategy.long)

if (shortCondition)

strategy.entry("Short", strategy.short)

// --- Risk Management (Stop Loss and Take Profit) ---

longStopLoss = close * (1 - stopLossPercent)

longTakeProfit = close * (1 + takeProfitPercent)

shortStopLoss = close * (1 + stopLossPercent)

shortTakeProfit = close * (1 - takeProfitPercent)

// Set the stop loss and take profit for long and short positions

strategy.exit("Long Exit", from_entry="Long", stop=longStopLoss, limit=longTakeProfit)

strategy.exit("Short Exit", from_entry="Short", stop=shortStopLoss, limit=shortTakeProfit)

相关推荐