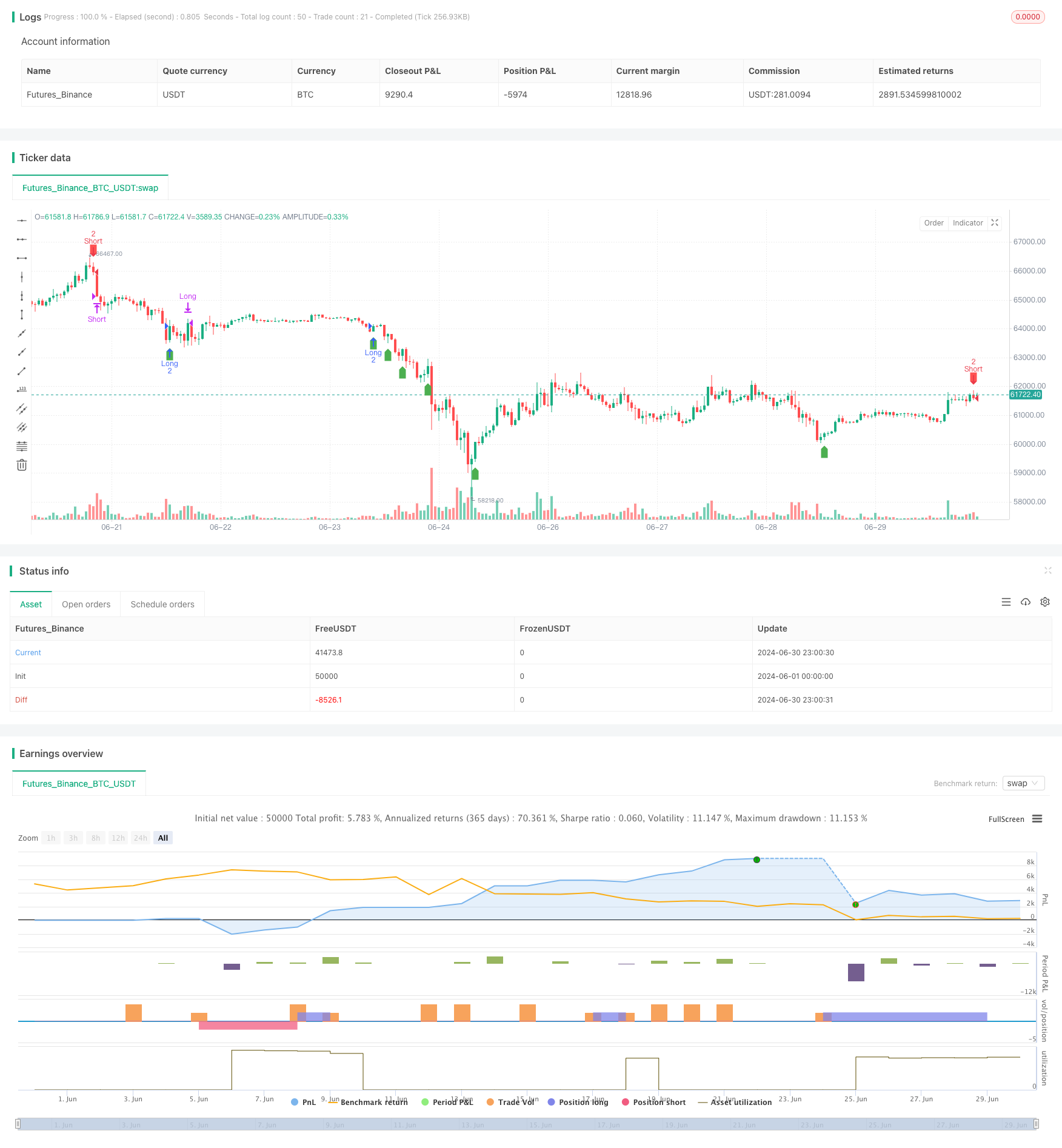

Overview

This strategy is a reversal cross momentum trading system based on the Relative Strength Index (RSI), combined with a fixed profit target exit mechanism. It primarily targets the 30-minute timeframe, utilizing the RSI indicator’s overbought and oversold regions to identify potential market reversal opportunities. The core idea of the strategy is to enter long positions when the RSI crosses above a specific threshold from the oversold area, and to enter short positions when the RSI crosses below a specific threshold from the overbought area. Additionally, the strategy sets a fixed profit target, automatically closing positions once the target is reached to lock in profits.

Strategy Principles

RSI Calculation: Uses the 14-period RSI indicator as the primary technical indicator.

Entry Conditions:

- Long: Triggers a buy signal when the RSI crosses above 31 after being below 30.

- Short: Triggers a sell signal when the RSI crosses below 69 after being above 70.

Exit Conditions:

- Long: Closes the position when profit reaches $2500.

- Short: Closes the position when profit reaches $2500.

Profit Target: Calculates the specific exit price level based on the entry price and target profit.

Trade Size: Fixed at 10 lots per trade.

Chart Display: Clearly marks entry points, exit points, and expected closing positions.

Strategy Advantages

Simple and Effective: The strategy logic is straightforward, easy to understand and implement, while maintaining high effectiveness.

Reversal Capture: Effectively captures potential market reversal points using the RSI indicator, improving entry timing accuracy.

Risk Control: Setting a fixed profit target helps to lock in profits promptly and control risk.

High Adaptability: Can be adjusted for different market characteristics by modifying RSI parameters and profit targets.

Clear Visualization: The strategy clearly marks entry points, exit points, and expected closing positions on the chart, facilitating intuitive understanding and monitoring for traders.

High Degree of Automation: The strategy can be fully automated, reducing human intervention and emotional influence.

Favorable Risk-Reward Ratio: The fixed profit target setting helps maintain a good risk-reward ratio.

Strategy Risks

False Breakout Risk: RSI may produce false breakouts, leading to incorrect trading signals.

Insufficient Trend Following: Fixed profit targets may result in premature closing of positions during strong trends, missing out on larger gains.

Overtrading: Frequent RSI crossovers may lead to overtrading, increasing transaction costs.

Slippage Risk: In fast-moving markets, it may be impossible to precisely reach the profit target due to slippage.

Parameter Sensitivity: Strategy performance may be sensitive to RSI period and threshold parameter settings, requiring careful optimization.

Market Environment Dependency: May underperform in trending markets, more suitable for range-bound markets.

Fixed Position Risk: Fixed trade size may not be suitable for all market conditions, increasing money management risk.

Strategy Optimization Directions

Dynamic Parameter Adjustment: Consider dynamically adjusting RSI parameters and entry thresholds based on market volatility to adapt to different market environments.

Introduce Trend Filters: Combine with other trend indicators, such as moving averages, to avoid counter-trend trading in strong trends.

Optimize Profit Targets: Consider using dynamic profit targets, such as volatility-adaptive targets based on ATR, to better adapt to market changes.

Introduce Stop-Loss Mechanism: Add stop-loss conditions, such as fixed stop-loss or trailing stop-loss, to further control risk.

Position Management Optimization: Implement more flexible position management strategies, such as percentage-based positions relative to account equity.

Multi-Timeframe Analysis: Incorporate RSI signals from higher timeframes to enhance trading decision reliability.

Add Filtering Conditions: Consider adding additional filtering conditions such as volume and price action patterns to improve signal quality.

Backtesting and Optimization: Conduct extensive historical backtesting and parameter optimization to find the best parameter combinations.

Conclusion

The RSI Reversal Cross Momentum Profit Target Quantitative Trading Strategy is a simple yet effective trading system that cleverly combines RSI indicator reversal signals with fixed profit target risk management. The strategy identifies potential market reversal opportunities by capturing RSI crossovers in overbought and oversold areas while using preset profit targets to control risk and lock in profits.

The main advantages of the strategy lie in its simplicity, clear trading logic, and high automation potential. However, it also faces challenges such as false breakout risks and potential underperformance in strongly trending markets. By introducing dynamic parameter adjustments, trend filters, optimizing profit targets, and improving position management, the strategy’s robustness and adaptability can be further enhanced.

Overall, this strategy provides traders with a good starting point that can be further customized and optimized according to individual trading styles and market characteristics. Through careful backtesting and continuous improvement, it has the potential to become a reliable trading tool, especially in range-bound market environments. However, traders should still exercise caution when applying it in practice and combine it with other analytical methods and risk management techniques to achieve optimal trading results.

/*backtest

start: 2024-06-01 00:00:00

end: 2024-06-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("1H RSI Reversal Scalping Bot with Profit Target", overlay=true)

// Input settings

rsiPeriod = input(14, title="RSI Period")

overboughtLevel = input(70, title="Overbought Level")

oversoldLevel = input(30, title="Oversold Level")

entryOverbought = input(69, title="Entry Overbought Level")

entryOversold = input(31, title="Entry Oversold Level")

profitTarget = input(2000, title="Profit Target (in USD)")

tradeSize = input(2, title="Trade Size (Lots)")

// RSI Calculation

rsi = ta.rsi(close, rsiPeriod)

// Entry conditions

longCondition = ta.crossover(rsi, entryOversold) and ta.valuewhen(ta.crossunder(rsi, oversoldLevel), rsi, 0) < entryOversold

shortCondition = ta.crossunder(rsi, entryOverbought) and ta.valuewhen(ta.crossover(rsi, overboughtLevel), rsi, 0) > entryOverbought

// Calculate profit in ticks

tickValue = syminfo.pointvalue

profitTicks = profitTarget / (tickValue * tradeSize)

// Determine the profit target level in price units

longExitPrice = strategy.position_avg_price + profitTicks * syminfo.mintick

shortExitPrice = strategy.position_avg_price - profitTicks * syminfo.mintick

// Plotting entry and exit points

plotshape(series=longCondition, location=location.belowbar, color=color.green, style=shape.labelup, title="Buy Signal")

plotshape(series=shortCondition, location=location.abovebar, color=color.red, style=shape.labeldown, title="Sell Signal")

// Strategy execution

if (longCondition)

strategy.entry("Long", strategy.long, qty=tradeSize)

if (shortCondition)

strategy.entry("Short", strategy.short, qty=tradeSize)

// Close long position if profit target met

if (strategy.position_size > 0 and close >= longExitPrice)

strategy.close("Long")

// Close short position if profit target met

if (strategy.position_size < 0 and close <= shortExitPrice)

strategy.close("Short")

// Plot expected close markers

var label expectedCloseMarker = na

if (longCondition)

expectedCloseMarker := label.new(x=bar_index, y=longExitPrice, text="Expected Close", style=label.style_label_down, color=color.blue, textcolor=color.white, size=size.small)

if (shortCondition)

expectedCloseMarker := label.new(x=bar_index, y=shortExitPrice, text="Expected Close", style=label.style_label_up, color=color.blue, textcolor=color.white, size=size.small)

// Plot RSI for reference

// hline(overboughtLevel, "Overbought", color=color.red)

// hline(oversoldLevel, "Oversold", color=color.green)

// plot(rsi, color=color.purple, title="RSI")