Estrategia cuantitativa mejorada de ruptura de Bollinger con sistema de integración del filtro de impulso

El autor:¿ Qué pasa?, fecha: 2024-12-12 14:55:37Las etiquetas:- ¿ Qué?Indicador de riesgoEl EMAEl ATRRR

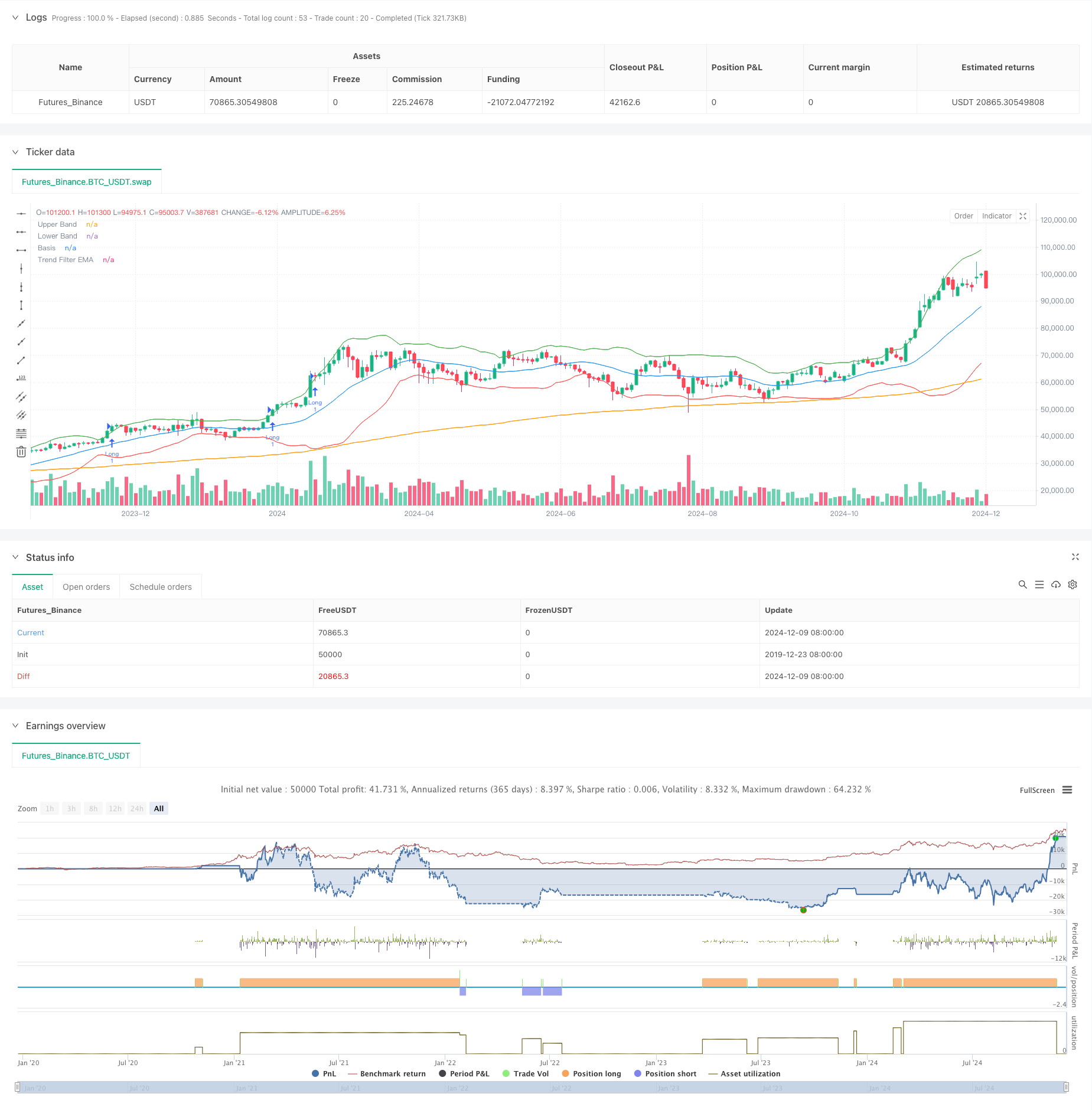

Resumen general

Esta estrategia es un sistema de negociación cuantitativo avanzado que combina bandas de Bollinger, indicador RSI y filtro de tendencia EMA de 200 períodos. A través de la sinergia de múltiples indicadores técnicos, captura oportunidades de ruptura de alta probabilidad en la dirección de la tendencia mientras filtra eficazmente señales falsas en mercados oscilantes.

Principio de la estrategia

La lógica central se basa en tres niveles: 1. señales de ruptura de bandas de Bollinger: utilizando bandas de Bollinger como canales de volatilidad, las rupturas de precios por encima de las entradas largas de la señal de banda superior, las rupturas por debajo de las entradas cortas de la señal de banda inferior. 2. Confirmación del impulso del RSI: el RSI por encima de 50 confirma el impulso alcista, por debajo de 50 confirma el impulso bajista, evitando operaciones sin tendencia. Filtración de tendencia de la EMA: Utilizando la EMA de 200 períodos para determinar la tendencia principal, solo se negocia en la dirección de la tendencia.

La confirmación del comercio requiere: - Condiciones de ruptura mantenidas durante dos velas consecutivas - Volumen superior a la media de 20 períodos Las pérdidas de liquidación derivadas de las pérdidas de liquidación derivadas de las pérdidas de liquidación derivadas de las pérdidas de liquidación derivadas de las pérdidas de liquidación - Objetivo de beneficio fijado en 1,5 veces la relación riesgo/beneficio

Ventajas estratégicas

- La sinergia de múltiples indicadores técnicos mejora significativamente la calidad de la señal

- El mecanismo dinámico de gestión de posiciones se adapta a la volatilidad del mercado

- El mecanismo estricto de confirmación de operaciones reduce eficazmente las señales falsas

- Sistema completo de control de riesgos, incluido el stop-loss dinámico y la relación riesgo-rendimiento fija

- Espacio de optimización de parámetros flexible y adaptable a diferentes entornos de mercado

Riesgos estratégicos

- La optimización excesiva de los parámetros puede conducir a un sobreajuste

- Los mercados volátiles pueden desencadenar frecuentes stop-loss

- Los mercados oscilantes pueden producir pérdidas consecutivas

- Las señales se retrasan en los puntos de inflexión de la tendencia

- Los indicadores técnicos pueden producir señales contradictorias

Sugerencias para el control de riesgos: - Ejecutar estrictamente la disciplina de stop-loss - Control del riesgo del comercio único - Validez de los parámetros del backtest regular - Integrar el análisis fundamental - Evita el exceso de comercio

Direcciones para la optimización de la estrategia

- Introducir más indicadores técnicos para la validación cruzada

- Desarrollar un mecanismo de optimización de parámetros adaptativos

- Añadir indicadores de confianza en el mercado

- Optimizar el mecanismo de confirmación del comercio

- Desarrollar un sistema de gestión de posiciones más flexible

Principales enfoques de optimización: - Ajustar dinámicamente los parámetros basados en los diferentes ciclos del mercado - Añadir filtros de comercio - Optimizar la configuración de la relación riesgo-recompensa - Mejorar el mecanismo de stop-loss - Desarrollar un sistema de confirmación de señales más inteligente

Resumen de las actividades

Esta estrategia construye un sistema comercial completo a través de una combinación orgánica de Bollinger Bands, RSI y indicadores técnicos EMA. Al tiempo que garantiza la calidad de la negociación, el sistema demuestra un fuerte valor práctico a través de un estricto control de riesgos y un espacio flexible de optimización de parámetros. Se aconseja a los operadores que validen cuidadosamente los parámetros en el comercio en vivo, ejecuten estrictamente la disciplina comercial y optimicen continuamente el rendimiento de la estrategia.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Improved Bollinger Breakout with Trend Filtering", overlay=true)

// === Inputs ===

length = input(20, title="Bollinger Bands Length", tooltip="The number of candles used to calculate the Bollinger Bands. Higher values smooth the bands, lower values make them more reactive.")

mult = input(2.0, title="Bollinger Bands Multiplier", tooltip="Controls the width of the Bollinger Bands. Higher values widen the bands, capturing more price movement.")

rsi_length = input(14, title="RSI Length", tooltip="The number of candles used to calculate the RSI. Shorter lengths make it more sensitive to recent price movements.")

rsi_midline = input(50, title="RSI Midline", tooltip="Defines the midline for RSI to confirm momentum. Higher values make it stricter for bullish conditions.")

risk_reward_ratio = input(1.5, title="Risk/Reward Ratio", tooltip="Determines the take-profit level relative to the stop-loss.")

atr_multiplier = input(1.5, title="ATR Multiplier for Stop-Loss", tooltip="Defines the distance of the stop-loss based on ATR. Higher values set wider stop-losses.")

volume_filter = input(true, title="Enable Volume Filter", tooltip="If enabled, trades will only execute when volume exceeds the 20-period average.")

trend_filter_length = input(200, title="Trend Filter EMA Length", tooltip="The EMA length used to filter trades based on the market trend.")

trade_direction = input.string("Both", title="Trade Direction", options=["Long", "Short", "Both"], tooltip="Choose whether to trade only Long, only Short, or Both directions.")

confirm_candles = input(2, title="Number of Confirming Candles", tooltip="The number of consecutive candles that must meet the conditions before entering a trade.")

// === Indicator Calculations ===

basis = ta.sma(close, length)

dev = mult * ta.stdev(close, length)

upper_band = basis + dev

lower_band = basis - dev

rsi_val = ta.rsi(close, rsi_length)

atr_val = ta.atr(14)

vol_filter = volume > ta.sma(volume, 20)

ema_trend = ta.ema(close, trend_filter_length)

// === Helper Function for Confirmation ===

confirm_condition(cond, lookback) =>

count = 0

for i = 0 to lookback - 1

count += cond[i] ? 1 : 0

count == lookback

// === Trend Filter ===

trend_is_bullish = close > ema_trend

trend_is_bearish = close < ema_trend

// === Long and Short Conditions with Confirmation ===

long_raw_condition = close > upper_band * 1.01 and rsi_val > rsi_midline and (not volume_filter or vol_filter) and trend_is_bullish

short_raw_condition = close < lower_band * 0.99 and rsi_val < rsi_midline and (not volume_filter or vol_filter) and trend_is_bearish

long_condition = confirm_condition(long_raw_condition, confirm_candles)

short_condition = confirm_condition(short_raw_condition, confirm_candles)

// === Trade Entry and Exit Logic ===

if long_condition and (trade_direction == "Long" or trade_direction == "Both")

strategy.entry("Long", strategy.long)

strategy.exit("Exit Long", "Long", stop=close - (atr_multiplier * atr_val), limit=close + (atr_multiplier * risk_reward_ratio * atr_val))

if short_condition and (trade_direction == "Short" or trade_direction == "Both")

strategy.entry("Short", strategy.short)

strategy.exit("Exit Short", "Short", stop=close + (atr_multiplier * atr_val), limit=close - (atr_multiplier * risk_reward_ratio * atr_val))

// === Plotting ===

plot(upper_band, color=color.green, title="Upper Band")

plot(lower_band, color=color.red, title="Lower Band")

plot(basis, color=color.blue, title="Basis")

plot(ema_trend, color=color.orange, title="Trend Filter EMA")

- Estrategia de cruce de media móvil exponencial de varios plazos con optimización de riesgo-recompensa

- Estrategia de negociación después de la ruptura abierta con gestión dinámica de posiciones basada en ATR

- Estrategia de cruce de impulso de tendencias múltiples con sistema de optimización de la volatilidad

- Tendencia de alta tasa de ganancia significa estrategia de negociación de inversión

- No hay estrategia de ruptura de vela alcista de parche superior

- Estrategia de negociación de tendencia de stop-loss dinámico de múltiples indicadores

- Tendencia compuesta de múltiples indicadores siguiendo la estrategia

- Estrategia de negociación de tendencia de impulso de múltiples indicadores: un sistema de negociación cuantitativo optimizado basado en bandas de Bollinger, Fibonacci y ATR

- Estrategia de integración de bandas RSI-Bollinger: un sistema de negociación dinámico y autoadaptable de múltiples indicadores

- Crossover de la EMA con la estrategia de doble entrada de bandas de Bollinger: un sistema de negociación cuantitativo que combina el seguimiento de tendencias y la ruptura de la volatilidad

- Tendencia de múltiples indicadores siguiendo una estrategia con canal dinámico y sistema de negociación de media móvil

- Tendencia de seguimiento de la estrategia multi-EMA con confirmación de SMMA

- Sistema de negociación de tendencias de múltiples indicadores con estrategia de análisis de impulso

- Estrategia de divergencia de impulso de la nube de seguimiento de tendencias

- Seguimiento de tendencias de múltiples indicadores y estrategia de ruptura de la volatilidad

- Tendencia multiindicador de adaptación a múltiples mercados siguiendo la estrategia

- Estrategia de gestión de posiciones y calendario dinámico basado en la volatilidad

- Estrategia compuesta EMA-MACD para el scalping de tendencias

- Seguimiento de tendencias y estrategia de impulso basada en indicadores técnicos múltiples

- Estrategia de negociación de sesiones cuantitativas de alta frecuencia: Sistema de gestión de posiciones dinámicas adaptativas basado en señales de ruptura

- Tendencia del impulso cruzado de Multi-EMA siguiendo la estrategia

- Estrategia de negociación de impulso de volumen inteligente multi-objetivo

- Las bandas de Bollinger de varios períodos tocan la inversión de tendencia Estrategia de negociación cuantitativa

- Estrategia de negociación de ruptura de alta frecuencia basada en la dirección de cierre del candelero

- Tendencia de retroceso dinámico avanzado de Fibonacci Estrategia de negociación cuantitativa

- Tendencia de las ganancias de varios niveles de índice variable promedio dinámico siguiendo la estrategia

- Sistema de negociación de media móvil múltiple con confirmación de impulso y volumen Estrategia de tendencia cuantitativa

- Estrategia de negociación equilibrada con toma de ganancias y stop-loss

- Sistema mejorado de seguimiento de tendencias: Identificación dinámica de tendencias basada en ADX y SAR parabólico

- Estrategia de negociación de impulso estocástico de doble marco de tiempo