Stratégie de négociation dynamique à arrêt de traîneau multi-indicateur

Auteur:ChaoZhang est là., Date: 2025-01-06 11:51:53 Je suis désoléLes étiquettes:Réanimation cardiaqueLe taux d'intérêtIndice de résistanceATRR2R

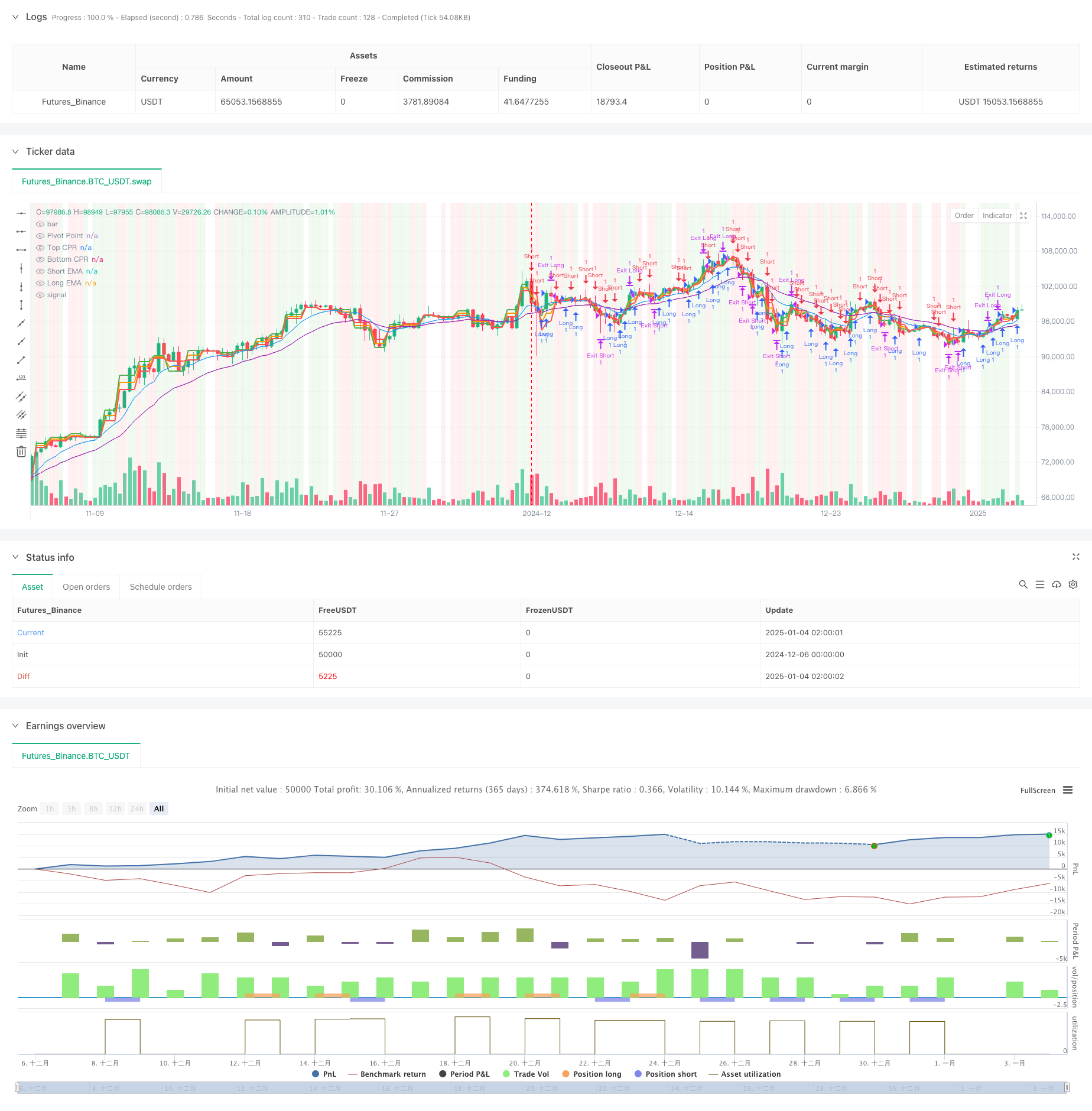

Résumé

Cette stratégie est un système de trading complet qui combine la plage centrale pivot (CPR), la moyenne mobile exponentielle (EMA), l'indice de force relative (RSI) et la logique de rupture.

Principes de stratégie

La stratégie repose sur plusieurs éléments essentiels:

- Indicateur CPR pour déterminer les niveaux de support et de résistance clés, calculer les points de pivotement quotidiens, les niveaux supérieurs et inférieurs.

- Système EMA double (9 jours et 21 jours) pour l'identification de la direction de la tendance par des croisements.

- Indicateur RSI (14 jours) pour confirmer les conditions de surachat/survente et le filtrage des signaux.

- Logique de rupture intégrant des ruptures de prix de points pivots pour la confirmation du signal.

- Indicateur ATR pour le stop-loss dynamique, ajustant adaptivement les distances de stop en fonction de la volatilité du marché.

Les avantages de la stratégie

- L'intégration de plusieurs indicateurs techniques améliore la fiabilité du signal.

- Le mécanisme de stop-loss dynamique de trailing bloque efficacement les bénéfices et contrôle les risques.

- L'indicateur CPR fournit des points de référence importants pour le positionnement précis de la structure du marché.

- La stratégie démontre une bonne adaptabilité avec des paramètres réglables pour différentes conditions de marché.

- Le filtre RSI et la confirmation de rupture renforcent la qualité du signal de trading.

Risques stratégiques

- Plusieurs indicateurs peuvent générer des signaux de retard et de faux signaux sur des marchés instables.

- Les arrêts de trailing peuvent être déclenchés prématurément pendant les périodes de forte volatilité.

- L'optimisation des paramètres nécessite la prise en compte des caractéristiques du marché; des réglages inappropriés peuvent affecter les performances de la stratégie.

- Les conflits de signaux peuvent avoir une incidence sur l'exactitude des décisions.

Directions d'optimisation de la stratégie

- Incorporer des indicateurs de volume pour confirmer la validité de l'éclatement des prix.

- Ajouter des filtres de force de tendance pour améliorer la précision de suivi de tendance.

- Optimiser le mécanisme d'ajustement dynamique des paramètres de stop-loss pour améliorer la protection.

- Mettre en œuvre un mécanisme d'adaptation à la volatilité du marché pour l'ajustement des paramètres dynamiques.

- Envisagez d'ajouter des indicateurs de sentiment pour améliorer le timing du marché.

Résumé

La stratégie construit un système de trading complet grâce à l'effet synergique de plusieurs indicateurs techniques. Le mécanisme de stop-loss dynamique et la confirmation de signal multidimensionnel fournissent des caractéristiques de risque-rendement favorables. Le potentiel d'optimisation de la stratégie réside principalement dans l'amélioration de la qualité du signal et le raffinement de la gestion des risques.

/*backtest

start: 2024-12-06 00:00:00

end: 2025-01-04 08:00:00

period: 7h

basePeriod: 7h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Enhanced CPR + EMA + RSI + Breakout Strategy", overlay=true)

// Inputs

ema_short = input(9, title="Short EMA Period")

ema_long = input(21, title="Long EMA Period")

cpr_lookback = input.timeframe("D", title="CPR Timeframe")

atr_multiplier = input.float(1.5, title="ATR Multiplier")

rsi_period = input(14, title="RSI Period")

rsi_overbought = input(70, title="RSI Overbought Level")

rsi_oversold = input(30, title="RSI Oversold Level")

breakout_buffer = input.float(0.001, title="Breakout Buffer (in %)")

// Calculate EMAs

short_ema = ta.ema(close, ema_short)

long_ema = ta.ema(close, ema_long)

// Request Daily Data for CPR Calculation

high_cpr = request.security(syminfo.tickerid, cpr_lookback, high)

low_cpr = request.security(syminfo.tickerid, cpr_lookback, low)

close_cpr = request.security(syminfo.tickerid, cpr_lookback, close)

// CPR Levels

pivot = (high_cpr + low_cpr + close_cpr) / 3

bc = (high_cpr + low_cpr) / 2

tc = pivot + (pivot - bc)

// ATR for Stop-Loss and Take-Profit

atr = ta.atr(14)

// RSI Calculation

rsi = ta.rsi(close, rsi_period)

// Entry Conditions with RSI Filter and Breakout Logic

long_condition = ((close > tc) and (ta.crossover(short_ema, long_ema)) and (rsi > 50 and rsi < rsi_overbought)) or (rsi > 80) or (close > (pivot + pivot * breakout_buffer))

short_condition = ((close < bc) and (ta.crossunder(short_ema, long_ema)) and (rsi < 50 and rsi > rsi_oversold)) or (rsi < 20) or (close < (pivot - pivot * breakout_buffer))

// Dynamic Exit Logic

long_exit = short_condition

short_exit = long_condition

// Trailing Stop-Loss Implementation

if long_condition

strategy.entry("Long", strategy.long)

strategy.exit("Exit Long", from_entry="Long",

trail_points=atr * atr_multiplier,

trail_offset=atr * atr_multiplier / 2)

if short_condition

strategy.entry("Short", strategy.short)

strategy.exit("Exit Short", from_entry="Short",

trail_points=atr * atr_multiplier,

trail_offset=atr * atr_multiplier / 2)

// Plot CPR Levels and EMAs

plot(pivot, title="Pivot Point", color=color.orange, linewidth=2)

plot(tc, title="Top CPR", color=color.green, linewidth=2)

plot(bc, title="Bottom CPR", color=color.red, linewidth=2)

plot(short_ema, title="Short EMA", color=color.blue, linewidth=1)

plot(long_ema, title="Long EMA", color=color.purple, linewidth=1)

// Highlight Buy and Sell Signals

bgcolor(long_condition ? color.new(color.green, 90) : na, title="Buy Signal Highlight")

bgcolor(short_condition ? color.new(color.red, 90) : na, title="Sell Signal Highlight")

Relationnée

- La stratégie de négociation quantitative multi-temporelle basée sur le RSI lissé par l'EMA et sur l'ATR Dynamic Stop Loss/Take Profit

- RSI50_EMA Stratégie à long terme uniquement

- Stratégie d'inversion de la dynamique du canal de tendance de l'or

- Stratégie de trading de modèle englobant 4 heures avec optimisation dynamique du profit et de l'arrêt des pertes

- La valeur de l'indicateur de volatilité est la valeur de l'indicateur de volatilité de l'indicateur de volatilité de l'indicateur de volatilité.

- Système de négociation ATR-RSI amélioré en fonction de la tendance

- Stratégie de croisement des indicateurs de risque de l'EMA

- Han Yue - Stratégie de négociation basée sur des EMA multiples, ATR et RSI

- Stratégie de pyramide intelligente à indicateurs multiples

- Stratégie de négociation AlphaTradingBot

Plus de

- Stratégie de négociation croisée à double dynamique moyenne mobile exponentielle

- RSI et bandes de Bollinger Stratégie synergique de swing trading

- Tendance de l' élan Stratégie de trading dans le cloud Ichimoku

- Supertrend de moyenne mobile multiple avec stratégie de négociation de rupture de Bollinger

- Stratégie quantitative croisée de moyenne mobile dynamique à indicateurs multiples

- Moyenne mobile à deux périodes avec dynamique RSI et tendance de volume suivant la stratégie

- Stratégie de négociation de rupture de tendance et d'amélioration de l'élan des indicateurs de risque

- Tendance dynamique croisée à la double EMA suite à une stratégie de négociation quantitative

- Stratégie de négociation de flux de tendance adaptatif à filtres multiples

- Indicateur technique double dynamique Stratégie de négociation de confirmation de survente-surachat

- Système d'oscillateur stochastique double EMA: modèle de négociation quantitatif combinant suivi de tendance et dynamique

- Stratégie de négociation dynamique de volatilité à indicateurs multiples

- Théorie de la négociation dynamique: stratégie de croisement de période de moyenne mobile exponentielle et de volume cumulé

- Stratégie de croisement dynamique EMA avec système de filtrage de la force de tendance ADX

- Stratégie de négociation quantitative de tendance linéaire englobante à plusieurs périodes

- Stratégie de rupture de canal adaptative avec système de négociation dynamique de support et de résistance

- Filtrage dynamique Stratégie croisée EMA pour l'analyse des tendances quotidiennes

- Le système de négociation des tendances de support/résistance Camarilla

- Stratégie de négociation dynamique à tendance multi-signaux améliorée

- Système de négociation de Martingale à dynamique adaptative