Strategi Kuantitatif Breakout Bollinger yang ditingkatkan dengan Sistem Integrasi Filter Momentum

Penulis:ChaoZhang, Tanggal: 2024-12-12 14:55:37Tag:BBRSIEMAATRRR

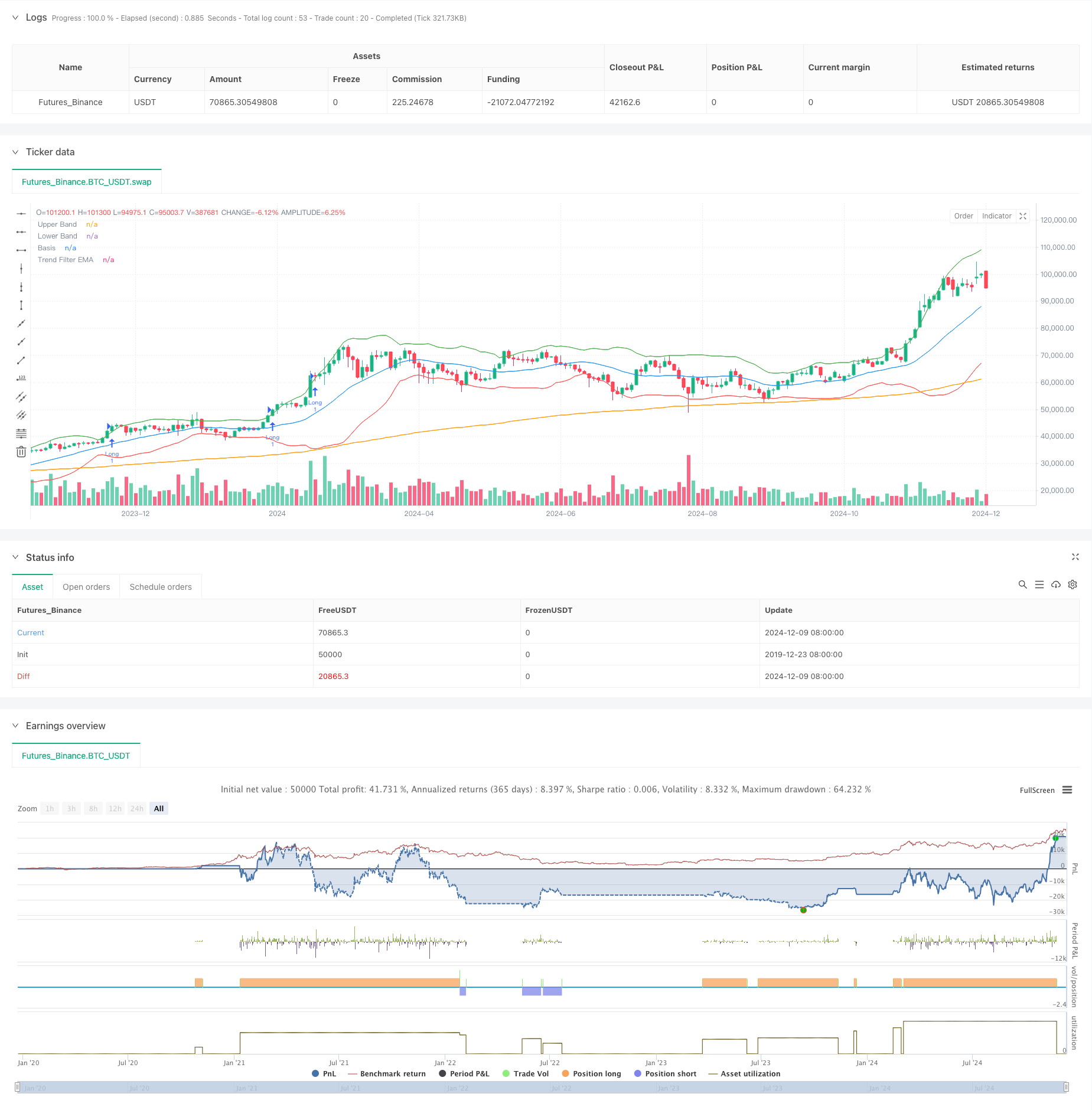

Gambaran umum

Strategi ini adalah sistem perdagangan kuantitatif canggih yang menggabungkan Bollinger Bands, indikator RSI, dan filter tren EMA 200 periode. Melalui sinergi dari beberapa indikator teknis, ia menangkap peluang breakout probabilitas tinggi ke arah tren sambil secara efektif menyaring sinyal palsu di pasar osilasi. Sistem ini menggunakan target stop-loss dan keuntungan dinamis berdasarkan rasio risiko-manfaat untuk mencapai kinerja perdagangan yang kuat.

Prinsip Strategi

Logika inti didasarkan pada tiga tingkat: 1. sinyal Bollinger Bands breakout: Menggunakan Bollinger Bands sebagai saluran volatilitas, harga pecah di atas entri panjang sinyal band atas, pecah di bawah entri pendek sinyal band bawah. 2. Konfirmasi momentum RSI: RSI di atas 50 mengkonfirmasi momentum bullish, di bawah 50 mengkonfirmasi momentum bearish, menghindari perdagangan tanpa tren. Filter tren EMA: Menggunakan EMA 200 periode untuk menentukan tren utama, hanya berdagang dalam arah tren.

Konfirmasi perdagangan membutuhkan: - Kondisi pecah dipertahankan untuk dua lilin berturut-turut - Volume di atas rata-rata 20 periode - Stop-loss dinamis yang dihitung berdasarkan ATR - Target keuntungan ditetapkan pada rasio risiko-manfaat 1,5 kali

Keuntungan Strategi

- Beberapa indikator teknis bekerja sama untuk meningkatkan kualitas sinyal secara signifikan

- Mekanisme manajemen posisi dinamis beradaptasi dengan volatilitas pasar

- Mekanisme konfirmasi perdagangan yang ketat secara efektif mengurangi sinyal palsu

- Sistem pengendalian risiko lengkap termasuk stop-loss dinamis dan rasio risiko-manfaat tetap

- Ruang optimasi parameter yang fleksibel yang dapat disesuaikan dengan lingkungan pasar yang berbeda

Risiko Strategi

- Optimasi parameter yang berlebihan dapat menyebabkan overfit

- Pasar yang tidak stabil dapat memicu seringnya stop loss

- Pasar osilasi dapat menghasilkan kerugian berturut-turut

- Sinyal tertinggal pada titik perubahan tren

- Indikator teknis dapat menghasilkan sinyal yang bertentangan

Saran pengendalian risiko: - Melakukan disiplin stop-loss yang ketat - Mengontrol risiko perdagangan tunggal - Validitas parameter backtest reguler - Mengintegrasikan analisis fundamental - Hindari overtrading

Arah Optimasi Strategi

- Memperkenalkan lebih banyak indikator teknis untuk penyangkalan silang

- Mengembangkan mekanisme optimasi parameter adaptif

- Tambahkan indikator sentimen pasar

- Mengoptimalkan mekanisme konfirmasi perdagangan

- Mengembangkan sistem manajemen posisi yang lebih fleksibel

Pendekatan optimasi utama: - Mengatur parameter secara dinamis berdasarkan siklus pasar yang berbeda - Tambahkan filter perdagangan - Mengoptimalkan pengaturan rasio risiko-balasan - Meningkatkan mekanisme stop-loss - Mengembangkan sistem konfirmasi sinyal yang lebih cerdas

Ringkasan

Strategi ini membangun sistem perdagangan yang lengkap melalui kombinasi organik dari Bollinger Bands, RSI dan indikator teknis EMA. Sementara memastikan kualitas perdagangan, sistem menunjukkan nilai praktis yang kuat melalui kontrol risiko yang ketat dan ruang optimasi parameter yang fleksibel. Pedagang disarankan untuk dengan hati-hati memvalidasi parameter dalam perdagangan langsung, secara ketat melaksanakan disiplin perdagangan, dan terus mengoptimalkan kinerja strategi.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Improved Bollinger Breakout with Trend Filtering", overlay=true)

// === Inputs ===

length = input(20, title="Bollinger Bands Length", tooltip="The number of candles used to calculate the Bollinger Bands. Higher values smooth the bands, lower values make them more reactive.")

mult = input(2.0, title="Bollinger Bands Multiplier", tooltip="Controls the width of the Bollinger Bands. Higher values widen the bands, capturing more price movement.")

rsi_length = input(14, title="RSI Length", tooltip="The number of candles used to calculate the RSI. Shorter lengths make it more sensitive to recent price movements.")

rsi_midline = input(50, title="RSI Midline", tooltip="Defines the midline for RSI to confirm momentum. Higher values make it stricter for bullish conditions.")

risk_reward_ratio = input(1.5, title="Risk/Reward Ratio", tooltip="Determines the take-profit level relative to the stop-loss.")

atr_multiplier = input(1.5, title="ATR Multiplier for Stop-Loss", tooltip="Defines the distance of the stop-loss based on ATR. Higher values set wider stop-losses.")

volume_filter = input(true, title="Enable Volume Filter", tooltip="If enabled, trades will only execute when volume exceeds the 20-period average.")

trend_filter_length = input(200, title="Trend Filter EMA Length", tooltip="The EMA length used to filter trades based on the market trend.")

trade_direction = input.string("Both", title="Trade Direction", options=["Long", "Short", "Both"], tooltip="Choose whether to trade only Long, only Short, or Both directions.")

confirm_candles = input(2, title="Number of Confirming Candles", tooltip="The number of consecutive candles that must meet the conditions before entering a trade.")

// === Indicator Calculations ===

basis = ta.sma(close, length)

dev = mult * ta.stdev(close, length)

upper_band = basis + dev

lower_band = basis - dev

rsi_val = ta.rsi(close, rsi_length)

atr_val = ta.atr(14)

vol_filter = volume > ta.sma(volume, 20)

ema_trend = ta.ema(close, trend_filter_length)

// === Helper Function for Confirmation ===

confirm_condition(cond, lookback) =>

count = 0

for i = 0 to lookback - 1

count += cond[i] ? 1 : 0

count == lookback

// === Trend Filter ===

trend_is_bullish = close > ema_trend

trend_is_bearish = close < ema_trend

// === Long and Short Conditions with Confirmation ===

long_raw_condition = close > upper_band * 1.01 and rsi_val > rsi_midline and (not volume_filter or vol_filter) and trend_is_bullish

short_raw_condition = close < lower_band * 0.99 and rsi_val < rsi_midline and (not volume_filter or vol_filter) and trend_is_bearish

long_condition = confirm_condition(long_raw_condition, confirm_candles)

short_condition = confirm_condition(short_raw_condition, confirm_candles)

// === Trade Entry and Exit Logic ===

if long_condition and (trade_direction == "Long" or trade_direction == "Both")

strategy.entry("Long", strategy.long)

strategy.exit("Exit Long", "Long", stop=close - (atr_multiplier * atr_val), limit=close + (atr_multiplier * risk_reward_ratio * atr_val))

if short_condition and (trade_direction == "Short" or trade_direction == "Both")

strategy.entry("Short", strategy.short)

strategy.exit("Exit Short", "Short", stop=close + (atr_multiplier * atr_val), limit=close - (atr_multiplier * risk_reward_ratio * atr_val))

// === Plotting ===

plot(upper_band, color=color.green, title="Upper Band")

plot(lower_band, color=color.red, title="Lower Band")

plot(basis, color=color.blue, title="Basis")

plot(ema_trend, color=color.orange, title="Trend Filter EMA")

- Strategi Crossover Rata-rata Bergerak Eksponensial Multi-Timeframe dengan Optimasi Risiko-Reward

- Strategi perdagangan setelah pembukaan dengan manajemen posisi berbasis ATR yang dinamis

- Strategi Crossover Momentum Multi-Trend dengan Sistem Optimasi Volatilitas

- Tren Tingkat Menang Tinggi Artinya Strategi Perdagangan Reversi

- Tidak ada Upper Wick Bullish Candle Breakout Strategi

- Strategi Trading Tren Stop-Loss Dinamis Multi-Indicator

- Tren Komposit Multi-Indikator Mengikuti Strategi

- Multi-Indikator Trend Momentum Trading Strategy: Sistem Trading Kuantitatif yang Dioptimalkan Berdasarkan Bollinger Bands, Fibonacci dan ATR

- Strategi Integrasi RSI-Bollinger Bands: Sistem Perdagangan Multi-Indikator yang Dinamis dan Beradaptasi Sendiri

- EMA Crossover dengan Bollinger Bands Double Entry Strategy: Sistem Trading Kuantitatif Menggabungkan Trend Following dan Volatility Breakout

- Tren Multi-Indikator Mengikuti Strategi dengan Saluran Dinamis dan Sistem Perdagangan Rata-rata Bergerak

- Multi-EMA Trend Mengikuti Strategi dengan Konfirmasi SMMA

- Sistem Perdagangan Tren Multi-Indikator dengan Strategi Analisis Momentum

- Strategi Divergensi Momentum Cloud yang Mengikuti Tren

- Trend Mengikuti Multi-Indikator dan Strategi Breakout Volatilitas

- Trend Multi-Pasar Adaptif Multi-Indikator Mengikuti Strategi

- Strategi Manajemen Posisi dan Waktu Dinamis Berdasarkan Volatilitas

- Strategi Komposit EMA-MACD untuk Trend Scalping

- Mengikuti tren dan strategi momentum berdasarkan indikator multi-teknis

- Strategi perdagangan sesi kuantitatif frekuensi tinggi: Sistem Manajemen Posisi Dinamis Adaptif Berdasarkan Sinyal Breakout

- Tren Momentum Crossover Multi-EMA Mengikuti Strategi

- Strategi Perdagangan Volume Momentum Multi-Target yang Cerdas

- Multi-Periode Bollinger Bands Touch Trend Reversal Strategi Perdagangan Kuantitatif

- Strategi perdagangan breakout frekuensi tinggi berdasarkan arah dekat candlestick

- Tren Retracement Fibonacci Dinamis Lanjutan Strategi Perdagangan Kuantitatif

- Variable Index Dynamic Average Multi-Tier Profit Trend Mengikuti Strategi

- Sistem perdagangan multi moving average dengan momentum dan konfirmasi volume Strategi tren kuantitatif

- Adaptive Trailing Drawdown Balanced Trading Strategy dengan Take Profit dan Stop Loss

- Sistem Pengamatan Tren yang Ditingkatkan: Identifikasi Tren Dinamis Berdasarkan ADX dan SAR Parabolik

- Strategi Trading Momentum Stochastic Dual Timeframe