概述

这是一个基于双均线交叉信号的量化交易策略,通过快速指数移动平均线(EMA)和慢速指数移动平均线(EMA)的交叉来判断市场趋势,同时结合动态止盈止损控制来管理风险。策略采用百分比仓位管理,默认使用10%的资金进行交易,通过设定动态的止盈和止损价格来保护利润和控制风险。

策略原理

策略的核心逻辑是通过监测20周期和50周期的指数移动平均线(EMA)的交叉来识别趋势变化。当快速EMA向上穿越慢速EMA时,系统产生做多信号。每次开仓后,系统会根据入场价格自动设置止盈价格(入场价格的1.3倍)和止损价格(入场价格的0.95倍)。这种动态止盈止损的设计能够根据不同的市场环境自适应调整,提高策略的灵活性。

策略优势

- 信号稳定性强 - 使用EMA而非简单移动平均线(SMA),能够更快速地响应价格变化,同时又能过滤掉部分市场噪音。

- 风险管理完善 - 采用动态止盈止损机制,止盈止损价格会随着入场价格的变化而调整。

- 资金管理合理 - 使用固定比例仓位管理,避免了全仓操作的高风险。

- 自动化程度高 - 从信号生成到仓位管理都实现了自动化,减少了人为干预。

- 适应性强 - 策略可以适应不同的市场环境,参数可根据实际情况灵活调整。

策略风险

- 均线滞后性 - EMA虽然反应较快,但仍存在一定的滞后性,可能导致入场时机略有延迟。

- 震荡市不适用 - 在市场横盘震荡时,可能会产生频繁的假突破信号。

- 固定倍数止盈止损 - 使用固定的倍数设置止盈止损,可能不适合所有市场环境。

- 回撤风险 - 在剧烈波动的市场中,5%的止损可能不足以应对大幅波动。

策略优化方向

- 引入波动率指标 - 建议添加ATR指标来动态调整止盈止损倍数,使其更适应市场波动。

- 增加趋势确认 - 可以结合RSI、MACD等指标来过滤交易信号,提高胜率。

- 优化仓位管理 - 可以根据市场波动率动态调整仓位大小,实现更精细的风险控制。

- 添加时间过滤 - 考虑增加交易时间窗口的限制,避开波动较大的时段。

- 完善止盈机制 - 可以实现移动止盈,在行情持续向好时获取更多收益。

总结

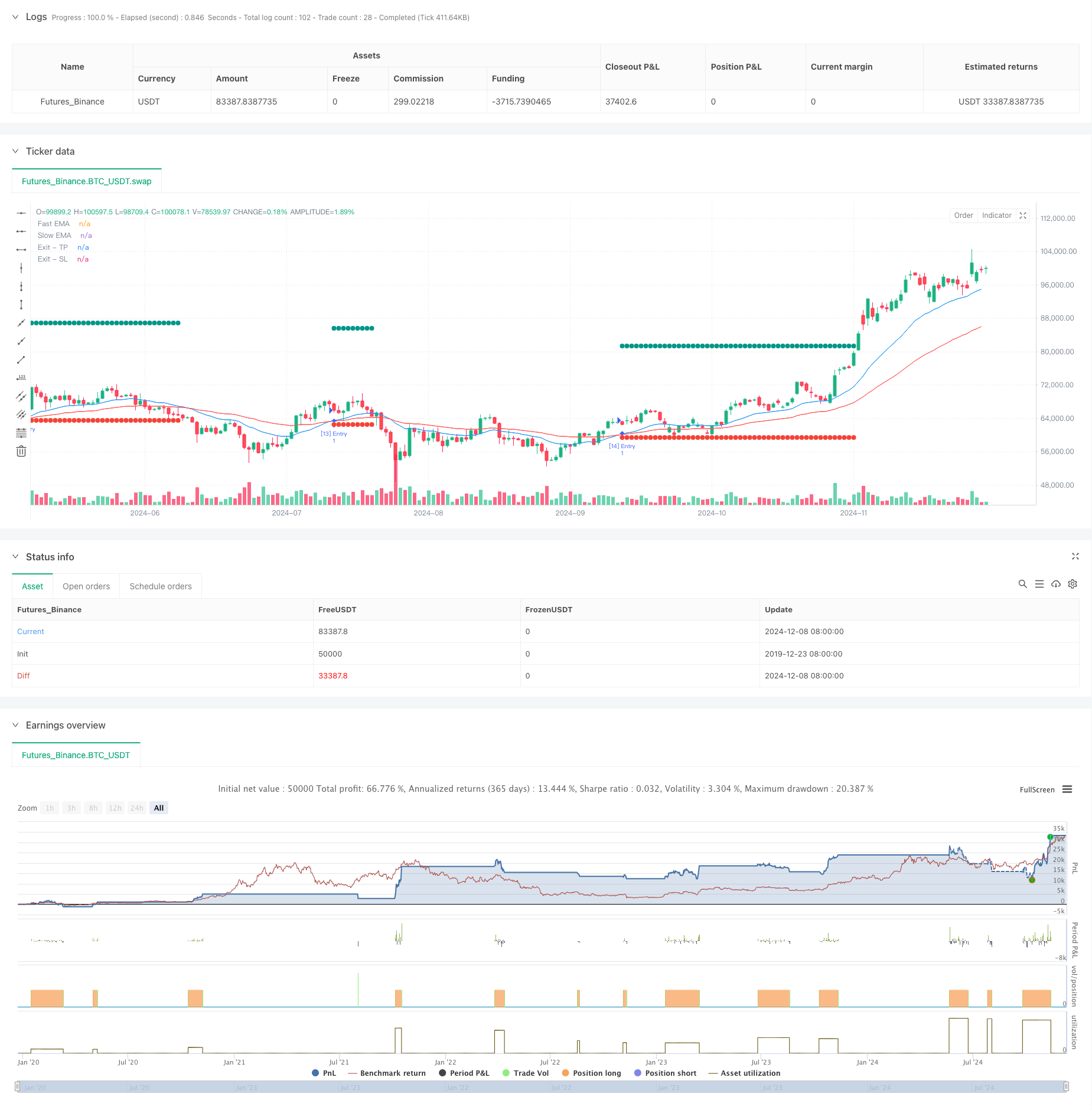

这是一个设计合理、逻辑清晰的趋势跟踪策略,通过双均线交叉捕捉趋势,使用动态止盈止损来管理风险。策略的优势在于操作规则明确、风险可控,适合作为中长期交易系统的基础框架。通过添加更多的过滤条件和优化止盈止损机制,该策略还有较大的优化空间。建议交易者在实盘使用前,先通过回测验证策略在不同市场环境下的表现,并根据自己的风险承受能力调整参数。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Pineify

//======================================================================//

// ____ _ _ __ //

// | _ \(_)_ __ ___(_)/ _|_ _ //

// | |_) | | '_ \ / _ \ | |_| | | | //

// | __/| | | | | __/ | _| |_| | //

// |_| |_|_| |_|\___|_|_| \__, | //

// |___/ //

//======================================================================//

//@version=5

strategy(title="TQQQ EMA Strategy", overlay=true)

//#region —————————————————————————————————————————————————— Common Dependence

p_comm_time_range_to_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int start_unix_time = na

int end_unix_time = na

int start_time_hour = na

int start_time_minute = na

int end_time_hour = na

int end_time_minute = na

if str.length(time_range) == 11

// Format: hh:mm-hh:mm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 3, 5)))

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 6, 8)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 9, 11)))

else if str.length(time_range) == 9

// Format: hhmm-hhmm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 2, 4)))

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 5, 7)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 7, 9)))

start_unix_time := timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), start_time_hour, start_time_minute, 0)

end_unix_time := timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), end_time_hour, end_time_minute, 0)

[start_unix_time, end_unix_time]

p_comm_time_range_to_start_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int start_time_hour = na

int start_time_minute = na

if str.length(time_range) == 11

// Format: hh:mm-hh:mm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 3, 5)))

else if str.length(time_range) == 9

// Format: hhmm-hhmm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 2, 4)))

timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), start_time_hour, start_time_minute, 0)

p_comm_time_range_to_end_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int end_time_hour = na

int end_time_minute = na

if str.length(time_range) == 11

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 6, 8)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 9, 11)))

else if str.length(time_range) == 9

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 5, 7)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 7, 9)))

timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), end_time_hour, end_time_minute, 0)

p_comm_timeframe_to_seconds(simple string tf) =>

float seconds = 0

tf_lower = str.lower(tf)

value = str.tonumber(str.substring(tf_lower, 0, str.length(tf_lower) - 1))

if str.endswith(tf_lower, 's')

seconds := value

else if str.endswith(tf_lower, 'd')

seconds := value * 86400

else if str.endswith(tf_lower, 'w')

seconds := value * 604800

else if str.endswith(tf_lower, 'm')

seconds := value * 2592000

else

seconds := str.tonumber(tf_lower) * 60

seconds

p_custom_sources() =>

[open, high, low, close, volume]

//#endregion —————————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Ta Dependence

//#endregion —————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Constants

// Input Groups

string P_GP_1 = ""

//#endregion —————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Inputs

// Default

int p_inp_1 = input.int(defval=20, title="Fast EMA Length", group=P_GP_1)

int p_inp_2 = input.int(defval=50, title="Slow EMA Length", group=P_GP_1)

float p_inp_3 = input.float(defval=1.3, title="Take Profit Price Multiplier", group=P_GP_1, step=0.01)

float p_inp_4 = input.float(defval=0.95, title="Stop Loss Price Multiplier", group=P_GP_1, step=0.01)

//#endregion ———————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Price Data

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Indicators

p_ind_1 = ta.ema(close, p_inp_1) // Fast EMA

p_ind_2 = ta.ema(close, p_inp_2) // Slow EMA

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Conditions

p_cond_1 = (ta.crossover(p_ind_1, p_ind_2))

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Strategy

// Strategy Order Variables

string p_st_name_1 = "Entry"

string p_st_name_2 = "Exit"

var float p_st_name_2_tp = na

var bool p_st_name_2_tp_can_drawing = true

var float p_st_name_2_sl = na

var bool p_st_name_2_sl_can_drawing = true

// Strategy Global

open_trades_number = strategy.opentrades

pre_bar_open_trades_number = na(open_trades_number[1]) ? 0 : open_trades_number[1]

var p_entry_order_id = 1

p_can_place_entry_order() =>

strategy.equity > 0

get_entry_id_name(int current_order_id, string name) =>

"[" + str.tostring(current_order_id) + "] " + name

is_entry_order(string order_id, string name) =>

str.startswith(order_id, "[") and str.endswith(order_id, "] " + name)

get_open_trades_entry_ids() =>

int p_open_trades_count = strategy.opentrades

string[] p_entry_ids = array.new_string(0, "")

if p_open_trades_count > 0

for i = 0 to p_open_trades_count - 1

array.push(p_entry_ids, strategy.opentrades.entry_id(i))

p_entry_ids

// Entry (Entry)

if p_cond_1 and p_can_place_entry_order()

p_st_name_1_id = get_entry_id_name(p_entry_order_id, p_st_name_1)

p_entry_order_id := p_entry_order_id + 1

string entry_message = ""

strategy.entry(id=p_st_name_1_id, direction=strategy.long, alert_message=entry_message, comment=p_st_name_1_id)

// TP/SL Exit (Exit)

float p_st_name_2_limit = close * p_inp_3

if p_st_name_2_tp_can_drawing

p_st_name_2_tp_can_drawing := false

p_st_name_2_tp := p_st_name_2_limit

float p_st_name_2_stop = close * p_inp_4

if p_st_name_2_sl_can_drawing

p_st_name_2_sl_can_drawing := false

p_st_name_2_sl := p_st_name_2_stop

string p_st_name_2_alert_message = ""

strategy.exit(id=p_st_name_1_id + "_0", from_entry=p_st_name_1_id, qty_percent=100, limit=p_st_name_2_limit, stop=p_st_name_2_stop, comment_profit=p_st_name_2 + " - TP", comment_loss=p_st_name_2 + " - SL", alert_message=p_st_name_2_alert_message)

if high >= p_st_name_2_tp or (pre_bar_open_trades_number > 0 and open_trades_number == 0)

p_st_name_2_tp_can_drawing := true

p_st_name_2_sl_can_drawing := true

p_st_name_2_tp := na

p_st_name_2_sl := na

plot(p_st_name_2_tp, title="Exit - TP", color=color.rgb(0, 150, 136, 0), linewidth=1, style = plot.style_circles)

if low <= p_st_name_2_sl or (pre_bar_open_trades_number > 0 and open_trades_number == 0)

p_st_name_2_sl_can_drawing := true

p_st_name_2_tp_can_drawing := true

p_st_name_2_sl := na

p_st_name_2_tp := na

plot(p_st_name_2_sl, title="Exit - SL", color=color.rgb(244, 67, 54, 0), linewidth=1, style = plot.style_circles)

//#endregion —————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Indicator Plots

// Fast EMA

plot(p_ind_1, "Fast EMA", color.rgb(33, 150, 243, 0), 1)

// Slow EMA

plot(p_ind_2, "Slow EMA", color.rgb(255, 82, 82, 0), 1)

//#endregion ————————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Custom Plots

//#endregion —————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Alert

//#endregion ——————————————————————————————————————————————————————

相关推荐