Dual EMA Crossover Momentum Trend Following Strategy

Author: ChaoZhang, Date: 2024-12-05 16:51:42Tags: EMAMACDRSI

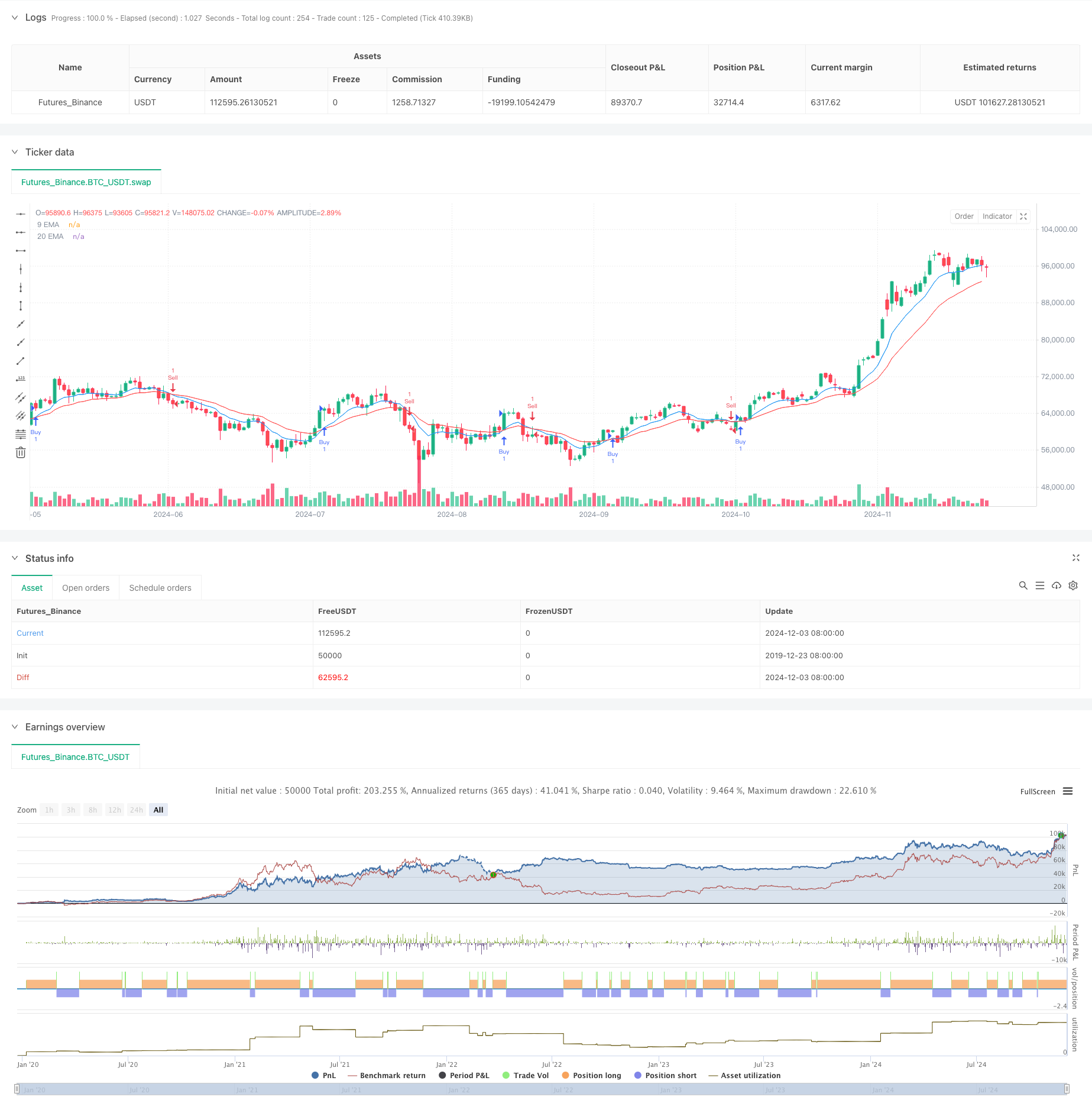

Overview

This strategy is a trend following trading system based on the crossover signals of 9-day and 20-day Exponential Moving Averages (EMA). It captures market trend reversals by monitoring the crossover relationship between the fast EMA (9-day) and slow EMA (20-day). The strategy employs programmatic trading to achieve fully automated operation, effectively avoiding human emotional interference.

Strategy Principle

The core of the strategy uses two EMAs with different periods to identify trend direction and turning points. When the 9-day EMA crosses above the 20-day EMA, the system generates a long signal; when the 9-day EMA crosses below the 20-day EMA, the system generates a short signal. EMAs assign greater weight to recent prices, enabling quick response to price changes and timely capture of trend reversals.

Strategy Advantages

- Clear operational rules with fully programmatic execution, avoiding emotional interference

- Uses exponential moving average calculation method for sensitive market response

- Includes trading alert functionality for timely trader notification

- Clear code structure, easy to maintain and optimize

- Applicable to different markets and time periods

- Strong trend following capability

Strategy Risks

- May generate frequent false signals in ranging markets

- Potential delay in entry timing

- Lack of stop-loss and take-profit mechanisms

- Trading costs not considered

- May underperform in highly volatile markets

- Requires attention to money management

Strategy Optimization Directions

- Add stop-loss and take-profit mechanisms for risk control

- Incorporate volume indicators to improve signal reliability

- Include trend filters to reduce false signals in ranging markets

- Optimize EMA parameters for better strategy adaptability

- Add volatility indicators to optimize trading timing

- Design position management module to improve risk-reward ratio

Summary

This strategy is a classical trend following system that captures trend reversal opportunities through EMA crossovers. The strategy logic is simple and clear, making it easy to understand and implement. However, for live trading, it is recommended to combine it with other technical indicators and money management methods to further improve the trading system. Additionally, optimizing parameters according to different market characteristics can enhance the strategy’s practicality.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-04 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("EMA Crossover Strategy with Buttons", overlay=true)

// Input parameters for EMAs

shortEmaLength = input(9, title="Short EMA Length")

longEmaLength = input(20, title="Long EMA Length")

// Calculate EMAs

shortEma = ta.ema(close, shortEmaLength)

longEma = ta.ema(close, longEmaLength)

// Plot EMAs

plot(shortEma, color=color.blue, title="9 EMA")

plot(longEma, color=color.red, title="20 EMA")

// Buy and Sell Logic

longCondition = ta.crossover(shortEma, longEma)

shortCondition = ta.crossunder(shortEma, longEma)

// Buy Button

if (ta.change(longCondition))

if (longCondition)

strategy.entry("Buy", strategy.long)

// Sell Button

if (ta.change(shortCondition))

if (shortCondition)

strategy.entry("Sell", strategy.short)

// Alert Conditions

alertcondition(longCondition, title="Buy Alert", message="Buy Signal")

alertcondition(shortCondition, title="Sell Alert", message="Sell Signal")

- Multi-Level Balanced Quantitative Trading Strategy

- EMA Dynamic Stop-Loss Trading Strategy

- EMA RSI MACD Dynamic Take Profit and Stop Loss Trading Strategy

- Multi-Indicator High-Frequency Trading Strategy: Short-Term Trading System Combining Exponential Moving Averages and Momentum Indicators

- MACD-RSI Trend Momentum Cross Strategy with Risk Management Model

- EMA, MACD, and RSI Triple Indicator Momentum Strategy

- Dual Trend Strategy with EMA Crossover and RSI Filter

- Multi-Dimensional Technical Indicator Trend Following Quantitative Strategy

- Multi-Technical Indicator Based Trend Following and Momentum Strategy

- EMA-MACD Composite Strategy for Trend Scalping

- Multi-Level Intelligent Dynamic Trailing Stop Strategy Based on Bollinger Bands and ATR

- Dynamic Dual EMA Crossover Strategy with Adaptive Profit/Loss Control

- Bollinger Bands and RSI Combined Dynamic Trading Strategy

- RSI-ATR Momentum Volatility Combined Trading Strategy

- Dual EMA Trend-Following Strategy with Limit Buy Entry

- Multi-Strategy Technical Analysis Trading System

- Multi-Timeframe Combined Candlestick Pattern Recognition Trading Strategy

- Triple Bollinger Bands Touch Trend Following Quantitative Trading Strategy

- Multi-Dimensional Dynamic Breakout Trading System Based on Bollinger Bands and RSI

- RSI Mean Reversion Breakout Strategy

- Multi-Step ATR Trading Strategy with Dynamic Profit Taking

- Dual Timeframe Dynamic Support Trading System

- Multi-Period Moving Average and RSI Momentum Cross Trend Following Strategy

- Financial Asset MFI-Based Oversold Zone Exit and Signal Averaging System

- Multi-EMA Crossover with Momentum Indicators Trading Strategy

- MACD-KDJ Combined Martingale Pyramiding Quantitative Trading Strategy

- Multi-Pattern Recognition and SR Level Trading Strategy

- G-Channel and EMA Trend Filter Trading System

- Dynamic Stop-Loss Multi-Period RSI Trend Following Strategy

- Dynamic Dual Moving Average Breakthrough Trading System