Break of Structure with Volume Confirmation Multi-Condition Intelligent Trading Strategy

Author: ChaoZhang, Date: 2024-12-20 16:15:43Tags: BOSSMAATRTPSL

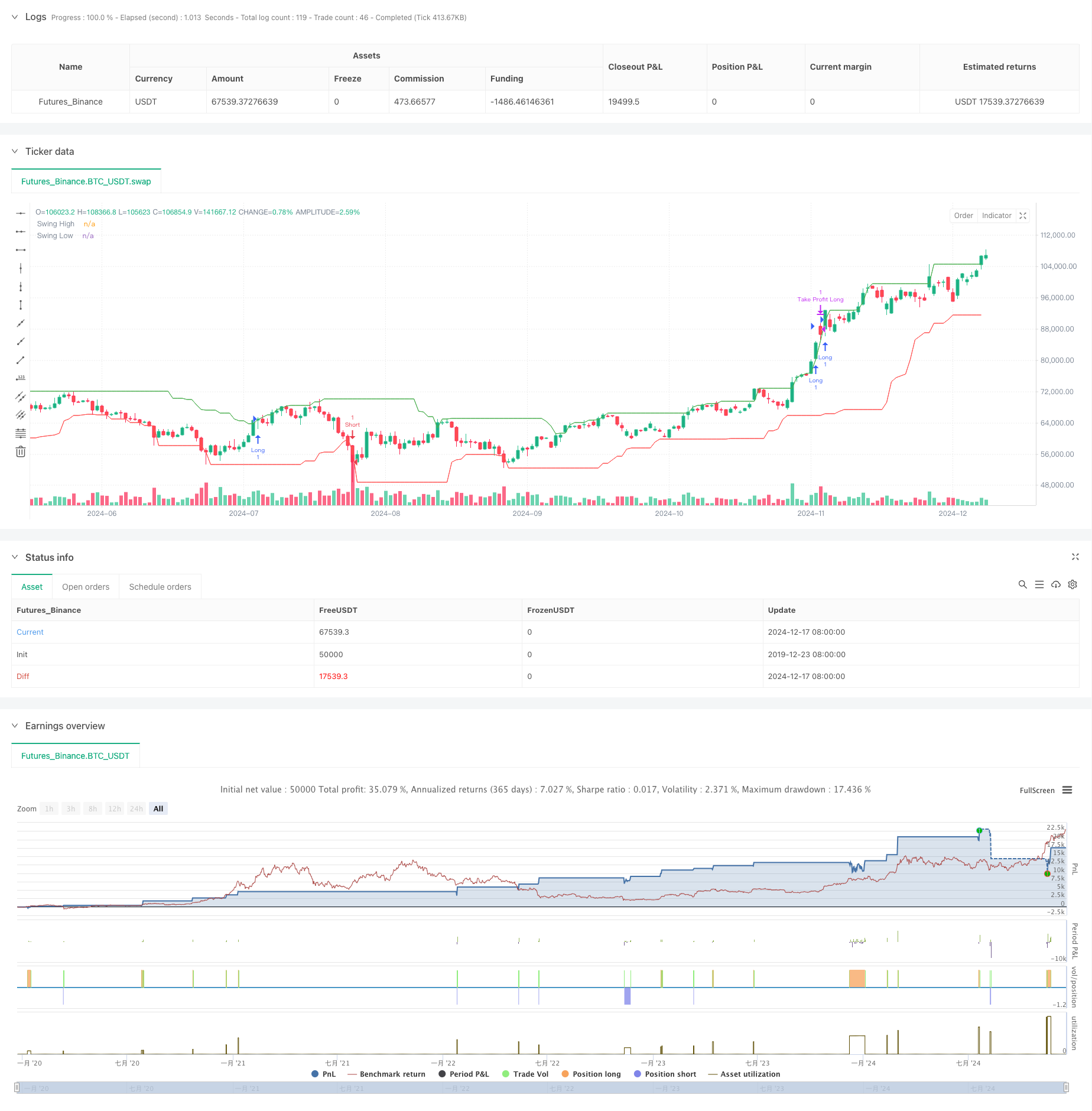

Overview

This is an intelligent trading strategy based on Break of Structure (BOS) and volume confirmation. The strategy generates trading signals by detecting price breakouts of previous highs or lows, combined with volume expansion confirmation. It employs multiple condition verification mechanisms, including consecutive confirmation requirements and dynamic take-profit/stop-loss settings, to enhance trading reliability and risk control capabilities.

Strategy Principles

The core logic includes the following key elements: 1. Identifies structural highs and lows by calculating the highest and lowest prices within a specified period 2. Uses moving averages to calculate volume baseline and determine significant volume expansion 3. Accumulates bullish confirmation count when price breaks above previous high with increased volume 4. Accumulates bearish confirmation count when price breaks below previous low with increased volume 5. Trading signals are only triggered after reaching the specified confirmation count 6. Sets percentage-based take-profit and stop-loss levels after position entry

Strategy Advantages

- Multiple condition verification mechanism improves signal reliability

- Volume indicator integration helps avoid false breakout signals

- Consecutive confirmation mechanism reduces trading frequency and increases win rate

- Dynamic take-profit/stop-loss settings automatically adjust exit positions based on entry price

- Clear strategy logic with adjustable parameters offers good adaptability

Strategy Risks

- Frequent false breakouts in ranging markets may lead to consecutive losses

- Stop-loss positions may not be timely enough in volatile markets

- Confirmation mechanism may delay entries, missing optimal price points

- Fixed volume judgment criteria may not adapt well to changing market conditions Solutions:

- Introduce market volatility indicators for dynamic parameter adjustment

- Add trend filters to reduce false signals in ranging markets

- Optimize stop-loss logic for improved flexibility

- Design adaptive volume threshold calculation methods

Strategy Optimization Directions

- Add trend identification indicators, such as moving average systems, to trade only in trend direction

- Incorporate ATR indicator for dynamic stop-loss distance adjustment

- Design volatility-adaptive volume threshold judgment mechanism

- Include time filters to avoid high-risk periods

- Optimize confirmation mechanism to improve entry timing while maintaining reliability

Summary

This is a strategy system that combines classical technical analysis theory with modern quantitative trading methods. Through multiple condition verification and strict risk control, the strategy demonstrates good stability and reliability. While there are aspects requiring optimization, the overall framework design is reasonable and has practical application value. The strategy’s performance can be further improved through the suggested optimization directions.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("BOS and Volume Strategy with Confirmation", overlay=true)

// Parameters

swingLength = input.int(20, title="Swing Length", minval=1)

volumeMultiplier = input.float(1.1, title="Volume Multiplier", step=0.1)

volumeSMA_length = input.int(10, title="Volume SMA Length", minval=1)

takeProfitPercentage = input.float(0.02, title="Take Profit Percentage", step=0.01)

stopLossPercentage = input.float(0.15, title="Stop Loss Percentage", step=0.01) // New parameter for stop loss

atrLength = input.int(14, title="ATR Length")

confirmationBars = input.int(2, title="Confirmation Bars", minval=1)

// Calculate Swing Highs and Lows

swingHigh = ta.highest(high, swingLength)[1]

swingLow = ta.lowest(low, swingLength)[1]

// Calculate Volume Moving Average

volumeSMA = ta.sma(volume, volumeSMA_length)

highVolume = volume > (volumeSMA * volumeMultiplier)

// Break of Structure Detection with Confirmation

var int bullishCount = 0

var int bearishCount = 0

if (close > swingHigh and highVolume)

bullishCount := bullishCount + 1

bearishCount := 0

else if (close < swingLow and highVolume)

bearishCount := bearishCount + 1

bullishCount := 0

else

bullishCount := 0

bearishCount := 0

bullishBOSConfirmed = (bullishCount >= confirmationBars)

bearishBOSConfirmed = (bearishCount >= confirmationBars)

// Entry and Exit Conditions

var float entryPrice = na // Declare entryPrice as a variable

if (bullishBOSConfirmed and strategy.position_size <= 0)

entryPrice := close // Use ':=' for assignment

strategy.entry("Long", strategy.long)

if (strategy.position_size > 0)

// Calculate stop loss price

stopLossPrice = entryPrice * (1 - stopLossPercentage)

strategy.exit("Take Profit Long", from_entry="Long", limit=entryPrice * (1 + takeProfitPercentage), stop=stopLossPrice)

if (bearishBOSConfirmed and strategy.position_size >= 0)

entryPrice := close // Use ':=' for assignment

strategy.entry("Short", strategy.short)

if (strategy.position_size < 0)

// Calculate stop loss price

stopLossPrice = entryPrice * (1 + stopLossPercentage)

strategy.exit("Take Profit Short", from_entry="Short", limit=entryPrice * (1 - takeProfitPercentage), stop=stopLossPrice)

// Plot Swing Highs and Lows for Visualization

plot(swingHigh, title="Swing High", color=color.green, linewidth=1)

plot(swingLow, title="Swing Low", color=color.red, linewidth=1)

- Dual Moving Average Crossover Strategy with Dynamic Risk Management

- Dual Moving Average Trend Following Strategy with ATR-Based Risk Management System

- Dynamic Dual-SMA Trend Following Strategy with Smart Risk Management

- Dynamic ATR Stop-Loss RSI Oversold Rebound Quantitative Strategy

- Advanced Long-Only Dynamic Trendline Breakout Strategy

- Adaptive Volatility and Momentum Quantitative Trading System (AVMQTS)

- Dynamic Moving Average and Bollinger Bands Cross Strategy with Fixed Stop-Loss Optimization Model

- ATR Fusion Trend Optimization Model Strategy

- Adaptive Moving Average Crossover with Trailing Stop-Loss Strategy

- Dynamic Long/Short Swing Trading Strategy with Moving Average Crossover Signal System

- Adaptive Trend Following Strategy with Dynamic Drawdown Control System

- Multi-EMA Golden Cross Strategy with Tiered Take-Profit

- Multi-Technical Indicator Cross-Trend Tracking Strategy: RSI and Stochastic RSI Synergy Trading System

- Dynamic Buy Entry Strategy Combining EMA Crossing and Candle Body Penetration

- Intelligent Wave-Trend Dollar Cost Averaging Cyclical Trading Strategy

- MACD-RSI Crossover Trend Following Strategy with Bollinger Bands Optimization System

- Adaptive EMA Dynamic Position Break-out Trading Strategy

- Multi-Indicator Dynamic Trading Optimization Strategy

- Multi-SMA Zone Breakout with Dynamic Profit Lock Quantitative Trading Strategy

- Dynamic Wave-Trend Tracking Strategy

- Multi-Indicator Dynamic Stop-Loss Momentum Trend Trading Strategy

- Multi-Condition Trend Following Quantitative Trading Strategy Based on Fibonacci Retracement Levels

- Multi-Moving Average Trend Following Trading Strategy

- Multi-Filter Trend Breakthrough Smart Moving Average Trading Strategy

- Dynamic EMA Breakthrough and Reversal Strategy

- Dynamic Trend Momentum Optimization Strategy with G-Channel Indicator

- Multi-level ATH Dynamic Tracking Triple-Entry Strategy

- Adaptive VWAP Bands with Garman-Klass Volatility Dynamic Tracking Strategy

- Multi-Indicator Trend Following Options Trading EMA Cross Strategy

- Multi-Indicator Volatility Trading RSI-EMA-ATR Strategy