概述

本策略是一个基于技术指标的波动交易策略,结合了均线交叉、RSI超买超卖和ATR止损止盈等多重信号。策略的核心是通过短期EMA和长期SMA的交叉来捕捉市场趋势,同时利用RSI指标进行信号确认,并通过ATR动态设置止损和止盈位置。策略支持多空双向交易,并可以根据用户偏好灵活开启或关闭任一方向。

策略原理

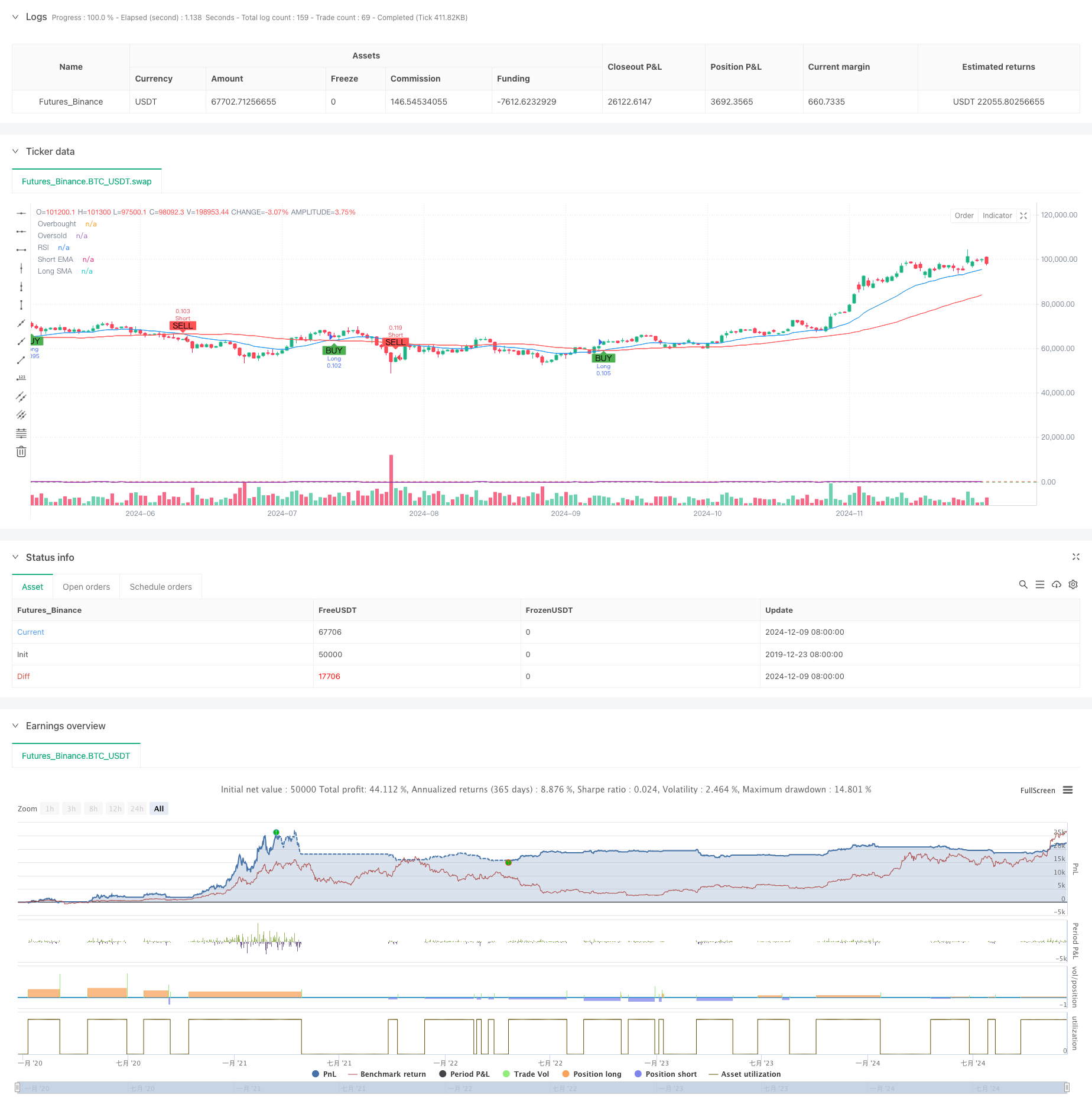

策略采用了多层技术指标组合的方式构建交易系统: 1. 趋势判断层:使用20周期EMA和50周期SMA的交叉来判断趋势方向,EMA上穿SMA视为做多信号,下穿则为做空信号。 2. 动量确认层:使用RSI指标进行超买超卖判断,RSI低于70时允许做多,高于30时允许做空。 3. 波动性计算层:使用14周期ATR来计算止损止盈位置,止损设置为1.5倍ATR,止盈设置为3倍ATR。 4. 仓位管理层:基于初始资金和每笔交易风险比例(默认1%)来动态计算开仓数量。

策略优势

- 多重信号确认:通过均线交叉、RSI和ATR三重指标的配合,有效降低假信号干扰。

- 动态止损止盈:基于ATR动态调整止损止盈位置,能更好地适应市场波动性变化。

- 灵活的交易方向:可以根据市场环境单独启用多头或空头交易。

- 严格的风险控制:通过百分比风险控制和动态仓位管理,有效控制每笔交易的风险敞口。

- 可视化支持:策略提供了完整的图表可视化支持,包括信号标记和指标显示。

策略风险

- 震荡市场风险:在横盘震荡市场中,均线交叉可能产生过多假信号。

- 滑点风险:在波动剧烈时期,实际成交价格可能与信号价格存在较大偏差。

- 资金管理风险:如果设置过高的风险比例,可能导致单笔损失过大。

- 参数敏感性:策略效果对参数设置较为敏感,需要careful调优。

策略优化方向

- 增加趋势强度过滤:可以添加ADX指标来过滤弱趋势环境下的交易信号。

- 优化均线周期:可以根据不同市场周期特征,动态调整均线参数。

- 完善止损机制:可以增加追踪止损功能,更好地保护盈利。

- 增加成交量确认:加入成交量指标作为辅助确认,提高信号可靠性。

- 市场环境分类:增加市场环境识别模块,在不同市场环境下使用不同的参数组合。

总结

该策略通过多重技术指标的组合运用,构建了一个相对完整的交易系统。策略的优势在于信号确认的可靠性和风险管理的完整性,但也需要注意市场环境对策略表现的影响。通过建议的优化方向,策略还有较大的改进空间。在实盘应用时,建议进行充分的参数测试和回测验证。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © CryptoRonin84

//@version=5

strategy("Swing Trading Strategy with On/Off Long and Short", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input for turning Long and Short trades ON/OFF

enable_long = input.bool(true, title="Enable Long Trades")

enable_short = input.bool(true, title="Enable Short Trades")

// Input parameters for strategy

sma_short_length = input.int(20, title="Short EMA Length", minval=1)

sma_long_length = input.int(50, title="Long SMA Length", minval=1)

sl_percentage = input.float(1.5, title="Stop Loss (%)", step=0.1, minval=0.1)

tp_percentage = input.float(3, title="Take Profit (%)", step=0.1, minval=0.1)

risk_per_trade = input.float(1, title="Risk Per Trade (%)", step=0.1, minval=0.1)

capital = input.float(10000, title="Initial Capital", step=100)

// Input for date range for backtesting

start_date = input(timestamp("2020-01-01 00:00"), title="Backtest Start Date")

end_date = input(timestamp("2024-12-31 23:59"), title="Backtest End Date")

inDateRange = true

// Moving averages

sma_short = ta.ema(close, sma_short_length)

sma_long = ta.sma(close, sma_long_length)

// RSI setup

rsi = ta.rsi(close, 14)

rsi_overbought = 70

rsi_oversold = 30

// ATR for volatility-based stop-loss calculation

atr = ta.atr(14)

stop_loss_level_long = strategy.position_avg_price - (1.5 * atr)

stop_loss_level_short = strategy.position_avg_price + (1.5 * atr)

take_profit_level_long = strategy.position_avg_price + (3 * atr)

take_profit_level_short = strategy.position_avg_price - (3 * atr)

// Position sizing based on risk per trade

risk_amount = capital * (risk_per_trade / 100)

position_size = risk_amount / (close * sl_percentage / 100)

// Long and Short conditions

long_condition = ta.crossover(sma_short, sma_long) and rsi < rsi_overbought

short_condition = ta.crossunder(sma_short, sma_long) and rsi > rsi_oversold

// Execute long trades

if (long_condition and inDateRange and enable_long)

strategy.entry("Long", strategy.long, qty=position_size)

strategy.exit("Take Profit/Stop Loss", "Long", stop=stop_loss_level_long, limit=take_profit_level_long)

// Execute short trades

if (short_condition and inDateRange and enable_short)

strategy.entry("Short", strategy.short, qty=position_size)

strategy.exit("Take Profit/Stop Loss", "Short", stop=stop_loss_level_short, limit=take_profit_level_short)

// Plot moving averages

plot(sma_short, title="Short EMA", color=color.blue)

plot(sma_long, title="Long SMA", color=color.red)

// Plot RSI on separate chart

hline(rsi_overbought, "Overbought", color=color.red)

hline(rsi_oversold, "Oversold", color=color.green)

plot(rsi, title="RSI", color=color.purple)

// Plot signals on chart

plotshape(series=long_condition and enable_long, title="Long Signal", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(series=short_condition and enable_short, title="Short Signal", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// Background color for backtest range

bgcolor(inDateRange ? na : color.red, transp=90)

相关推荐