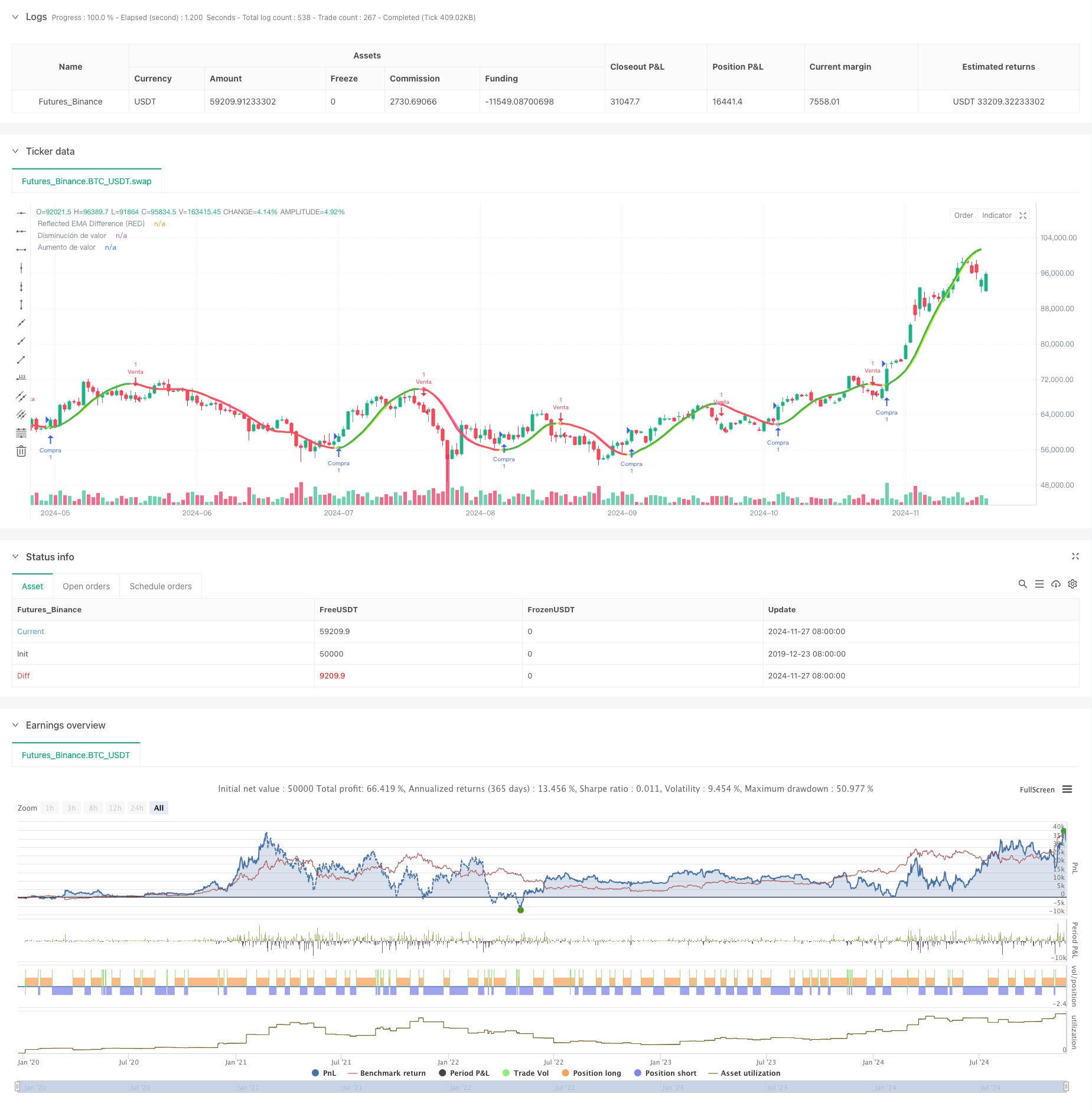

概述

该策略通过运用Hull移动平均线(HMA)的反射特性来判断市场趋势。策略核心是计算短期与长期Hull移动平均线之间的差异值,并通过这个差异的反射值来预测价格走势。通过设定可调整的百分比参数,策略能够适应不同的交易周期,从而提供更精准的趋势判断信号。

策略原理

策略采用了36周期和44周期的两条Hull移动平均线作为基础指标。通过计算这两条移动平均线之间的绝对差值,并结合当前趋势方向对差值进行反射计算,最终得到反射值。策略还引入了加权移动平均(WMA)来计算delta值,通过这个delta值与反射值的交叉来确定趋势的转折点。在趋势判断过程中,策略设置了可调整的修正因子,用于控制趋势反转的灵敏度。当价格突破预设的趋势限制线时,策略会发出相应的交易信号。

策略优势

- 采用Hull移动平均线降低了传统移动平均线的滞后性,提高了策略对市场变化的响应速度

- 引入反射值概念,能更准确地捕捉趋势转折点

- 设计了可调整的修正因子,使策略具有较强的适应性

- 通过绝对差值计算提高了信号的可靠性

- 集成了风险控制机制,包括趋势限制线的动态调整

- 系统自带可视化组件,便于交易者直观判断市场状态

策略风险

- 在横盘整理市场中可能产生频繁的假信号

- 参数设置不当可能导致信号滞后或过度敏感

- 在剧烈波动市场中,趋势限制线可能无法及时调整

- 策略依赖历史数据计算,在市场突发事件面前反应可能不够迅速

策略优化方向

- 引入波动率指标,动态调整修正因子,提高策略对市场状态的适应能力

- 增加市场状态识别机制,在不同市场环境下采用不同的参数设置

- 开发自适应参数优化系统,实现参数的动态调整

- 增加成交量分析模块,提高信号的可靠性

- 完善风险控制机制,增加止损和资金管理功能

总结

该策略通过创新性地将Hull移动平均线与反射值概念相结合,构建了一个反应灵敏、适应性强的趋势跟踪系统。策略的核心优势在于其对趋势转折点的准确捕捉能力,同时通过可调整的参数设置,保证了策略在不同市场环境下的适用性。虽然存在一些固有的风险,但通过持续优化和完善,该策略有望成为一个稳定可靠的交易工具。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Reflected EMA Difference (RED)", shorttitle="RED [by MarcosPna]", overlay=true) //mv30

// Análisis de Riesgo

// Risk Analysis

media_delta = ta.wma(2 * ta.wma(close, 8 / 2) - ta.wma(close, 8), math.floor(math.sqrt(8)))

// Calcular EMAs

// Calculate EMAs

ema_corta_delta = ta.hma(close, 36)

ema_larga_delta = ta.hma(close, 44)

// Calcular la diferencia entre las EMAs

// Calculate the difference between EMAs

diferencia_delta_ema = math.abs(ema_corta_delta - ema_larga_delta)

// Calcular el valor reflejado basado en la posición de la EMA corta

// Compute the reflected value based on the position of the short EMA

valor_reflejado_delta = ema_corta_delta + (ema_corta_delta > ema_larga_delta ? diferencia_delta_ema : -diferencia_delta_ema)

// Suavizar el valor reflejado

// Smooth the reflected value

periodo_suavizado_delta = input.int(2, title="Periodo extendido")

ema_suavizada_delta = ta.hma(valor_reflejado_delta, periodo_suavizado_delta)

// Ploteo de las EMAs y la línea reflejada

// Plot EMAs and the reflected line

plot(valor_reflejado_delta, title="Reflected EMA Difference (RED)", color=valor_reflejado_delta > ema_suavizada_delta ? color.rgb(253, 25, 238, 30) : color.rgb(183, 255, 30), linewidth=2, style=plot.style_line)

// Parámetros ajustables para la reversión de tendencia

// Adjustable parameters for trend reversal

factor_correccion_delta = input.float(title='Porcentaje de cambio', minval=0, maxval=100, step=0.1, defval=0.04)

tasa_correccion_delta = factor_correccion_delta * 0.01

// Variables para la reversión de tendencia

// Variables for trend reversal

var int direccion_delta_tendencia = 0

var float precio_maximo_delta = na

var float precio_minimo_delta = na

var float limite_tendencia_delta = na

// Inicializar precio máximo y mínimo con el primer valor de la EMA suavizada reflejada

// Initialize peak and trough prices with the first value of the smoothed reflected EMA

if na(precio_maximo_delta)

precio_maximo_delta := ema_suavizada_delta

if na(precio_minimo_delta)

precio_minimo_delta := ema_suavizada_delta

// Lógica de reversión de tendencia con la EMA suavizada reflejada

// Trend reversal logic with the smoothed reflected EMA

if direccion_delta_tendencia >= 0

if ema_suavizada_delta > precio_maximo_delta

precio_maximo_delta := ema_suavizada_delta

limite_tendencia_delta := precio_maximo_delta - (precio_maximo_delta * tasa_correccion_delta)

if ema_suavizada_delta <= limite_tendencia_delta

direccion_delta_tendencia := -1

precio_minimo_delta := ema_suavizada_delta

strategy.entry("Venta", strategy.short)

else

if ema_suavizada_delta < precio_minimo_delta

precio_minimo_delta := ema_suavizada_delta

limite_tendencia_delta := precio_minimo_delta + (precio_minimo_delta * tasa_correccion_delta)

if ema_suavizada_delta >= limite_tendencia_delta

direccion_delta_tendencia := 1

precio_maximo_delta := ema_suavizada_delta

strategy.entry("Compra", strategy.long)

// Ploteo y señales

// Plotting and signals

indice_delta_ascendente = plot(direccion_delta_tendencia == 1 ? limite_tendencia_delta : na, title="Aumento de valor", style=plot.style_linebr, linewidth=3, color=color.new(color.green, 0))

senal_compra_delta = direccion_delta_tendencia == 1 and direccion_delta_tendencia[1] == -1

plotshape(senal_compra_delta ? limite_tendencia_delta : na, title="Estilo señal alcista", location=location.absolute, style=shape.circle, size=size.tiny, color=color.new(color.green, 0))

indice_delta_descendente = plot(direccion_delta_tendencia == 1 ? na : limite_tendencia_delta, title="Disminución de valor", style=plot.style_linebr, linewidth=3, color=color.new(color.red, 0))

senal_venta_delta = direccion_delta_tendencia == -1 and direccion_delta_tendencia[1] == 1

plotshape(senal_venta_delta ? limite_tendencia_delta : na, title="Estilo señal bajista", location=location.absolute, style=shape.circle, size=size.tiny, color=color.new(color.red, 0))

// Variables para manejo de cajas

// Variables for box management

var box caja_tendencia_delta = na

// Condición: Cruce de HullMA hacia abajo

// Condition: HullMA crosses below reflected EMA value

cruce_bajista_delta = ta.crossunder(media_delta, valor_reflejado_delta)

// Condición: Cruce de HullMA hacia arriba

// Condition: HullMA crosses above reflected EMA value

cruce_alcista_delta = ta.crossover(media_delta, valor_reflejado_delta)

// Dibujar caja cuando HullMA cruza hacia abajo el valor reflejado de EMA

// Draw a box when HullMA crosses below the reflected EMA value

// if (cruce_bajista_delta) and direccion_delta_tendencia == 1

// caja_tendencia_delta := box.new(left=bar_index, top=high, right=bar_index, bottom=low, text = "Critical Areas", text_color = color.white, border_width=2, border_color=color.rgb(254, 213, 31), bgcolor=color.new(color.red, 90))

// Cerrar caja cuando HullMA cruza hacia arriba el valor reflejado de EMA

// Close the box when HullMA crosses above the reflected EMA value

// if (cruce_alcista_delta and not na(caja_tendencia_delta))

// box.set_right(caja_tendencia_delta, bar_index)

// caja_tendencia_delta := na // Remove the reference to create a new box at the next cross down

相关推荐