Volatility and Linear Regression-based Long-Short Market Regime Optimization Strategy

Author: ChaoZhang, Date: 2024-05-28 17:40:37Tags: ATREMA

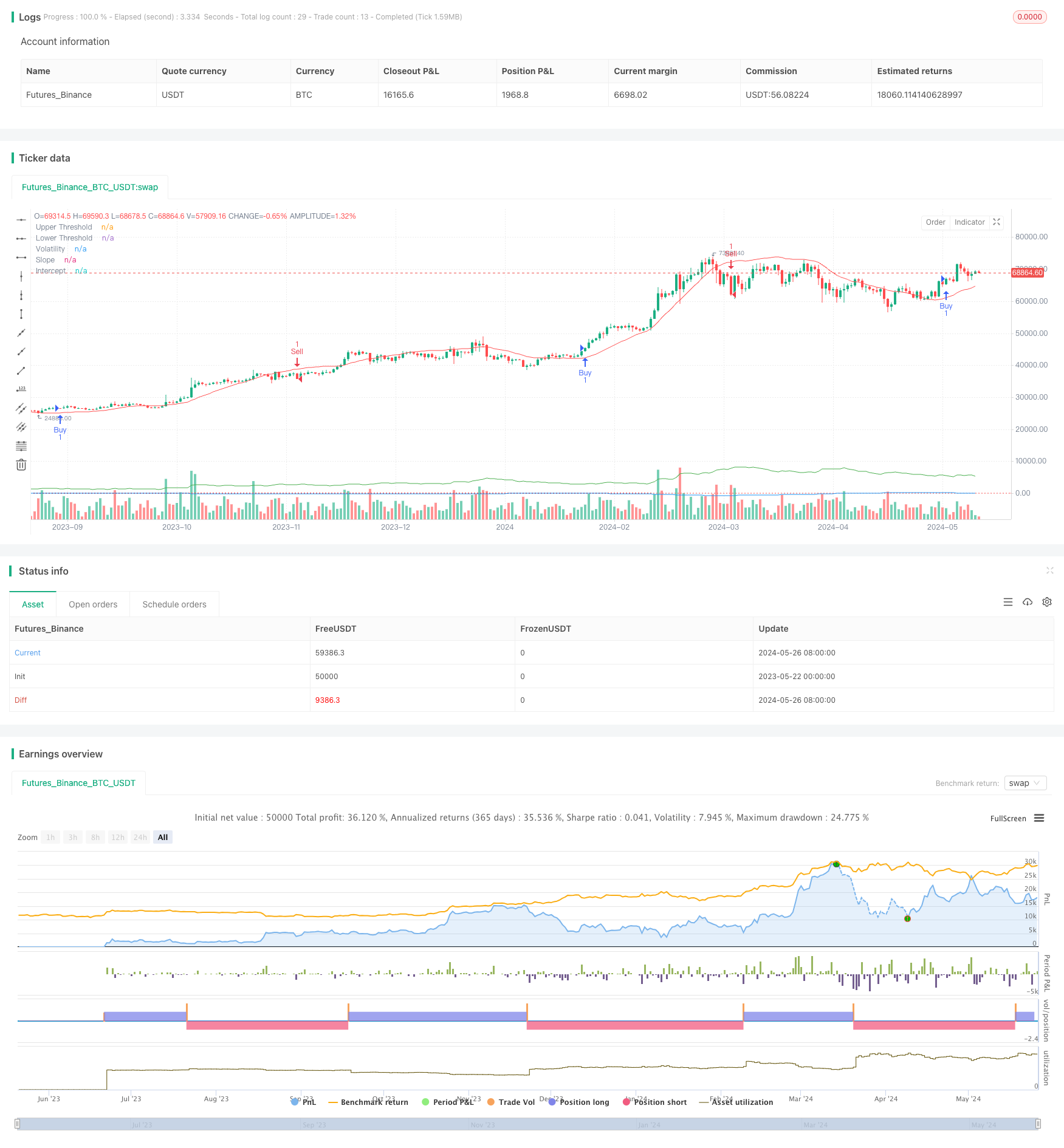

Overview

The strategy utilizes linear regression and volatility indicators to identify different market states. When the conditions for buying or selling are met, the strategy establishes corresponding long or short positions. Additionally, the strategy allows for parameter optimization and adjustment based on market conditions to adapt to various market environments. The strategy also employs exponential moving averages (EMAs) as additional indicators to confirm trading signals.

Strategy Principles

- Calculate the intercept and slope of the linear regression to determine market trends.

- Calculate the Average True Range (ATR) multiplied by a multiplier as the volatility indicator.

- Generate a buy signal when the slope is greater than the upper threshold and the price is above the regression line plus volatility.

- Generate a sell signal when the slope is less than the lower threshold and the price is below the regression line minus volatility.

- Use fast and slow EMAs as additional confirmation indicators.

- Establish a long position when a buy signal occurs and the fast EMA is above the slow EMA.

- Establish a short position when a sell signal occurs and the fast EMA is below the slow EMA.

Strategy Advantages

- By combining linear regression and volatility indicators, the strategy can more accurately identify market states and trends.

- The use of additional EMA indicators to confirm trading signals enhances the reliability of the strategy.

- Allowing optimization of key parameters enables adaptation to different market environments and instrument characteristics.

- Considering both trends and volatility, the strategy can promptly establish positions when trends are clear and control risks when volatility increases.

Strategy Risks

- Improper parameter selection may lead to poor strategy performance, requiring optimization based on specific instruments and market characteristics.

- In choppy markets or at trend turning points, the strategy may experience frequent trades or false signals.

- The strategy relies on historical data and may not react promptly to sudden events or abnormal market fluctuations.

Strategy Optimization Directions

- Incorporate other technical indicators or fundamental factors to enrich the decision-making basis and improve signal accuracy.

- Optimize parameter selection, such as regression length, volatility multiplier, EMA periods, etc., to adapt to different instruments and market characteristics.

- Introduce stop-loss and take-profit mechanisms to control individual trade risks and overall drawdown levels.

- Consider incorporating position sizing and money management rules to adjust position sizes based on market volatility and account equity.

Summary

The strategy identifies market states using linear regression and volatility indicators, with EMAs as confirmation indicators, constructing an adaptive and logically clear trading strategy. The strategy’s advantages lie in combining trends and volatility while allowing parameter optimization, making it suitable for various market environments. However, the strategy also faces risks such as parameter selection, choppy markets, and black swan events, requiring continuous optimization and improvement in practical applications. Future enhancements can focus on enriching signal sources, optimizing parameter selection, and refining risk control measures to enhance the strategy’s stability and profitability.

/*backtest

start: 2023-05-22 00:00:00

end: 2024-05-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tmalvao

//@version=5

strategy("Regime de Mercado com Regressão e Volatilidade Otimizado", overlay=true)

// Parâmetros para otimização

upperThreshold = input.float(1.0, title="Upper Threshold")

lowerThreshold = input.float(-1.0, title="Lower Threshold")

length = input.int(50, title="Length", minval=1)

// Indicadores de volatilidade

atrLength = input.int(14, title="ATR Length")

atrMult = input.float(2.0, title="ATR Multiplier")

atr = ta.atr(atrLength)

volatility = atr * atrMult

// Calculando a regressão linear usando função incorporada

intercept = ta.linreg(close, length, 0)

slope = ta.linreg(close, length, 1) - ta.linreg(close, length, 0)

// Sinal de compra e venda

buySignal = slope > upperThreshold and close > intercept + volatility

sellSignal = slope < lowerThreshold and close < intercept - volatility

// Entrando e saindo das posições

if (buySignal)

strategy.entry("Buy", strategy.long)

if (sellSignal)

strategy.entry("Sell", strategy.short)

// Indicadores adicionais para confirmação

emaFastLength = input.int(10, title="EMA Fast Length")

emaSlowLength = input.int(50, title="EMA Slow Length")

emaFast = ta.ema(close, emaFastLength)

emaSlow = ta.ema(close, emaSlowLength)

// Confirmando sinais com EMAs

if (buySignal and emaFast > emaSlow)

strategy.entry("Buy Confirmed", strategy.long)

if (sellSignal and emaFast < emaSlow)

strategy.entry("Sell Confirmed", strategy.short)

// Exibindo informações no gráfico

plot(slope, title="Slope", color=color.blue)

plot(intercept, title="Intercept", color=color.red)

plot(volatility, title="Volatility", color=color.green)

hline(upperThreshold, "Upper Threshold", color=color.green, linestyle=hline.style_dotted)

hline(lowerThreshold, "Lower Threshold", color=color.red, linestyle=hline.style_dotted)

- Enhanced Multi-Indicator Momentum Trading Strategy

- Multi-Timeframe Trend Following Strategy with ATR-Based Take Profit and Stop Loss

- K Consecutive Candles Bull Bear Strategy

- Keltner Channels EMA ATR Strategy

- Supertrend and EMA Combination Strategy

- Multi-Indicator Trend Following Strategy with Dynamic Channel and Moving Average Trading System

- ATR and EMA-based Dynamic Take Profit and Stop Loss Adaptive Strategy

- EMA Dynamic Trend Following Trading Strategy

- Triple EMA Crossover Strategy

- Multi-Exponential Moving Average Crossover Strategy with Volume-Based ATR Dynamic Stop-Loss Optimization

- MA MACD BB Multi-Indicator Trading Strategy Backtesting Tool

- RSI+Supertrend Trend-Following Trading Strategy

- Ichimoku Kumo Trading Strategy

- Dynamic ATR Stop Loss and Take Profit Moving Average Crossover Strategy

- EMA Trend Momentum Candlestick Pattern Strategy

- G-Channel Trend Detection Strategy

- Moving Average Crossover with Trailing Stop Loss Strategy

- EMA Crossover Trading Strategy with Dynamic Take Profit and Stop Loss

- Bollinger Bands and EMA Trend Following Strategy

- WaveTrend Oscillator Divergence Strategy

- Hybrid Binomial Z-Score Quantitative Strategy

- RSI and MA Combination Strategy

- EMA Momentum Trading Strategy

- FVG Momentum Scalping Strategy

- ATR and EMA-based Dynamic Take Profit and Stop Loss Adaptive Strategy

- Trend Following with Breakout and Frequency Filter (Long Only)

- Fibonacci Golden Harmony Breakout Strategy

- Dynamic Market Regime Identification Strategy Based on Linear Regression Slope

- Trend Reversal Trading Strategy Based on RSI Divergence

- Dual Moving Average RSI Momentum Strategy Based on EMA and Trendline Breakouts