Advanced Multi-Indicator Multi-Dimensional Trend Cross Quantitative Strategy

Author: ChaoZhang, Date: 2025-01-17 16:00:03Tags: RSIMACDEMAHTFSMACCIMA

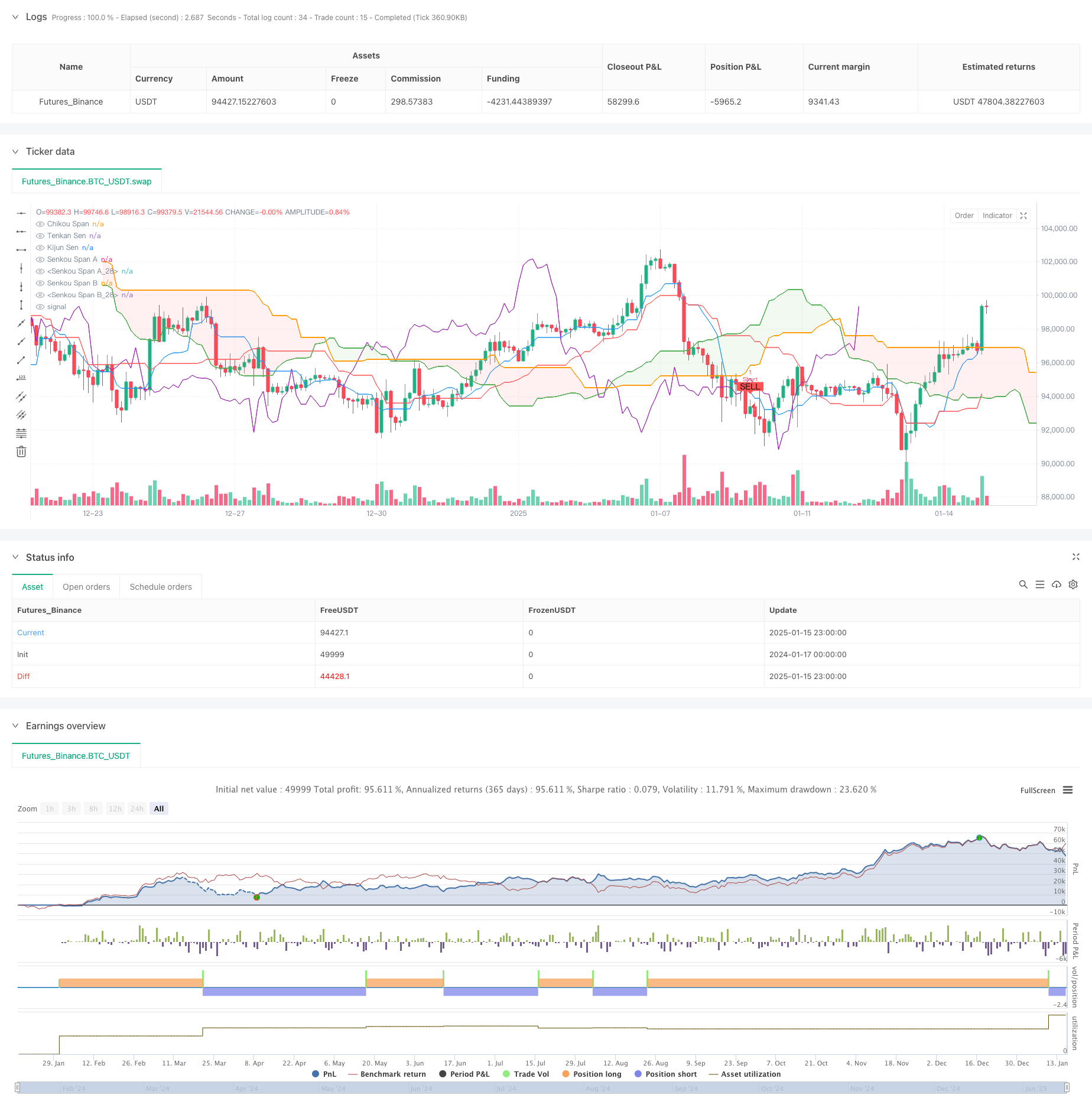

Overview

This strategy is a comprehensive trading system that combines multiple technical indicators, including Ichimoku Cloud, Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Higher Time Frame (HTF) divergence, and Exponential Moving Average (EMA) crossovers. The strategy utilizes multiple signal confirmations to improve trading accuracy while leveraging market information from different time frames to capture more reliable trading opportunities.

Strategy Principles

The core principle of the strategy is to confirm trading signals through multi-layer technical analysis. It uses the Ichimoku Cloud components to determine overall market trends, combines RSI to judge market overbought/oversold conditions, utilizes MACD to identify trend momentum changes, and captures potential trend reversal signals through HTF RSI and MACD divergences. Additionally, the strategy incorporates EMA50 and EMA100 crossovers for confirmation, along with EMA200 as a primary trend filter, creating a multi-layered trading confirmation system.

Strategy Advantages

- Multi-dimensional signal confirmation significantly reduces false breakout risks and improves trading accuracy

- HTF divergence analysis enhances the ability to predict market turning points

- Integration of trend-following and reversal trading characteristics provides strong adaptability

- EMA crossovers provide additional trend confirmation, improving entry timing accuracy

- Comprehensive technical indicator system enables all-round market state analysis

Strategy Risks

- Multiple indicator confirmations may cause missed opportunities in rapid market movements

- May generate numerous false signals in ranging markets

- High complexity in parameter optimization increases the risk of overfitting

- Multiple indicators may introduce certain latency in signal generation

- Multiple confirmation mechanisms may fail under extreme market conditions

Strategy Optimization Directions

- Introduce adaptive parameter mechanisms to dynamically adjust indicator parameters based on market conditions

- Add volatility filters to adjust strategy parameters in high-volatility environments

- Develop more intelligent stop-loss and take-profit mechanisms to improve money management efficiency

- Add market state classification modules to apply different trading logic for different market conditions

- Optimize HTF divergence identification algorithms to improve signal timeliness

Summary

This strategy constructs a relatively complete trading system through the coordination of multiple technical indicators. Its strength lies in its multi-dimensional signal confirmation mechanism, while also facing challenges in parameter optimization and market adaptability. Through the proposed optimization directions, the strategy has the potential to further enhance its performance across different market environments while maintaining its robustness.

/*backtest

start: 2024-01-17 00:00:00

end: 2025-01-16 00:00:00

period: 3h

basePeriod: 3h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=6

strategy("Ichimoku + RSI + MACD + HTF Divergence + EMA Cross Strategy", overlay=true)

// تنظیمات تایمفریم بالاتر

htf_timeframe = input.timeframe("D", title="تایمفریم بالاتر")

// تنظیمات پارامترهای ایچیموکو

tenkan_period = input(9, title="Tenkan Sen Period")

kijun_period = input(26, title="Kijun Sen Period")

senkou_span_b_period = input(52, title="Senkou Span B Period")

displacement = input(26, title="Displacement")

// محاسبه خطوط ایچیموکو

tenkan_sen = (ta.highest(high, tenkan_period) + ta.lowest(low, tenkan_period)) / 2

kijun_sen = (ta.highest(high, kijun_period) + ta.lowest(low, kijun_period)) / 2

senkou_span_a = (tenkan_sen + kijun_sen) / 2

senkou_span_b = (ta.highest(high, senkou_span_b_period) + ta.lowest(low, senkou_span_b_period)) / 2

chikou_span = close // قیمت بسته شدن فعلی

// رسم خطوط ایچیموکو

plot(tenkan_sen, color=color.blue, title="Tenkan Sen")

plot(kijun_sen, color=color.red, title="Kijun Sen")

plot(senkou_span_a, offset=displacement, color=color.green, title="Senkou Span A")

plot(senkou_span_b, offset=displacement, color=color.orange, title="Senkou Span B")

plot(chikou_span, offset=-displacement, color=color.purple, title="Chikou Span")

// رنگآمیزی ابر ایچیموکو

fill(plot(senkou_span_a, offset=displacement, color=color.green, title="Senkou Span A"), plot(senkou_span_b, offset=displacement, color=color.orange, title="Senkou Span B"), color=senkou_span_a > senkou_span_b ? color.new(color.green, 90) : color.new(color.red, 90), title="Cloud")

// تنظیمات RSI

rsi_length = input(14, title="RSI Length")

rsi_overbought = input(70, title="RSI Overbought Level")

rsi_oversold = input(30, title="RSI Oversold Level")

// محاسبه RSI

rsi_value = ta.rsi(close, rsi_length)

// تنظیمات MACD

fast_length = input(12, title="MACD Fast Length")

slow_length = input(26, title="MACD Slow Length")

signal_smoothing = input(9, title="MACD Signal Smoothing")

// محاسبه MACD

[macd_line, signal_line, hist_line] = ta.macd(close, fast_length, slow_length, signal_smoothing)

// شناسایی واگراییها در تایمفریم بالاتر

f_find_divergence(src, lower, upper) =>

var int divergence = na // تعریف نوع متغیر بهصورت صریح

if (src >= upper and src[1] < upper)

divergence := 1 // واگرایی نزولی

else if (src <= lower and src[1] > lower)

divergence := -1 // واگرایی صعودی

divergence

// محاسبه RSI و MACD در تایمفریم بالاتر

htf_rsi_value = request.security(syminfo.tickerid, htf_timeframe, rsi_value)

htf_macd_line = request.security(syminfo.tickerid, htf_timeframe, macd_line)

// شناسایی واگراییها در تایمفریم بالاتر

htf_rsi_divergence = f_find_divergence(htf_rsi_value, rsi_oversold, rsi_overbought)

htf_macd_divergence = f_find_divergence(htf_macd_line, 0, 0)

// فیلتر روند با EMA 200

ema_200 = ta.ema(close, 200)

// اضافه کردن EMA 50 و 100

ema_50 = ta.ema(close, 50)

ema_100 = ta.ema(close, 100)

// کراسهای EMA

ema_cross_up = ta.crossover(ema_50, ema_100) // کراس صعودی EMA 50 و 100

ema_cross_down = ta.crossunder(ema_50, ema_100) // کراس نزولی EMA 50 و 100

// شرایط ورود و خروج

long_condition = (close > senkou_span_a and close > senkou_span_b) and // قیمت بالای ابر

(rsi_value > 50) and // RSI بالای 50

(macd_line > signal_line) and // MACD خط سیگنال را قطع کرده

(htf_rsi_divergence == -1 or htf_macd_divergence == -1) and // واگرایی صعودی در تایمفریم بالاتر

(close > ema_200) and // قیمت بالای EMA 200

(ema_cross_up) // کراس صعودی EMA 50 و 100

short_condition = (close < senkou_span_a and close < senkou_span_b) and // قیمت زیر ابر

(rsi_value < 50) and // RSI زیر 50

(macd_line < signal_line) and // MACD خط سیگنال را قطع کرده

(htf_rsi_divergence == 1 or htf_macd_divergence == 1) and // واگرایی نزولی در تایمفریم بالاتر

(close < ema_200) and // قیمت زیر EMA 200

(ema_cross_down) // کراس نزولی EMA 50 و 100

// نمایش نقاط ورود در چارت

plotshape(series=long_condition, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY", size=size.small)

plotshape(series=short_condition, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL", size=size.small)

// اجرای استراتژی

if (long_condition)

strategy.entry("Long", strategy.long)

if (short_condition)

strategy.entry("Short", strategy.short)

- Dynamic Dual Moving Average Crossover Quantitative Trading Strategy

- Quantitative Long-Short Switching Strategy Based on G-Channel and EMA

- Multi-Level Dynamic MACD Trend Following Strategy with 52-Week High/Low Extension Analysis System

- Multi-Strategy Technical Analysis Trading System

- Multi-EMA Dynamic Trend Capture Quantitative Trading Strategy

- Multi-Timeframe EMA Cross High-Win Rate Trend Following Strategy (Advanced)

- Multi-Technical Indicator Synergistic Trading System

- Dual EMA Indicator Smart Crossing Trading System with Dynamic Stop-Loss and Take-Profit Strategy

- EMA/SMA Multi-Indicator Comprehensive Trend Following Strategy

- No Upper Wick Bullish Candle Breakout Strategy

- Dynamic Stop-Loss Adjustment Elephant Bar Trend Following Strategy

- Dual-Period RSI Trend Momentum Strategy with Pyramiding Position Management System

- Multi-Timeframe Trading Strategy Combining Harmonic Patterns and Williams %R

- EMA Trend with Round Number Breakout Trading Strategy

- Dynamic RSI Quantitative Trading Strategy with Multiple Moving Average Crossover

- Dynamic Trend RSI Indicator Crossing Strategy

- Multi-Dimensional KNN Algorithm with Volume-Price Candlestick Pattern Trading Strategy

- Dual Crossover Trend Following Strategy: EMA and MACD Synergistic Trading System

- SMA-Based Intelligent Trailing Stop Strategy with Intraday Pattern Recognition

- Adaptive Multi-Strategy Dynamic Switching System: A Quantitative Trading Strategy Combining Trend Following and Range Oscillation

- Multi-Factor Regression and Dynamic Price Band Quantitative Trading System

- Multi-Indicator Dynamic Trend Detection and Risk Management Trading Strategy

- Multi-Smoothed Moving Average Dynamic Crossover Trend Following Strategy with Multiple Confirmations

- Advanced Dynamic Stop-Loss Strategy Based on Large Candles and RSI Divergence

- Liquidity-Weighted Moving Average Momentum Crossover Strategy

- Multi-Indicator Synergistic Trend Reversal Quantitative Trading Strategy

- Multi-Channel Dynamic Support Resistance Keltner Channel Strategy

- Machine Learning Adaptive SuperTrend Quantitative Trading Strategy

- Dynamic WaveTrend and Fibonacci Integrated Quantitative Trading Strategy

- Volatility Stop Based EMA Trend Following Trading Strategy