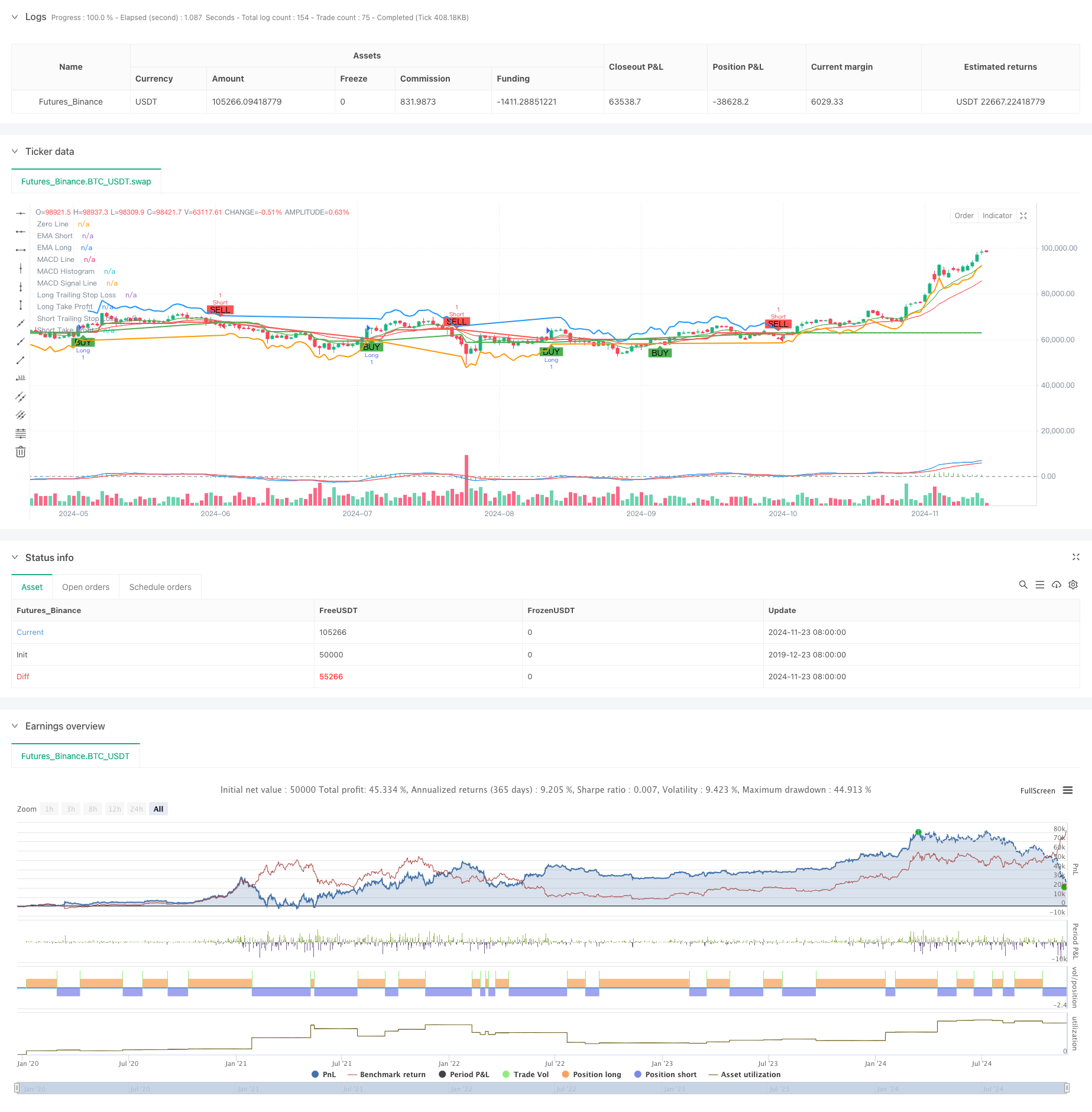

概述

该策略是一个综合性的趋势跟踪交易系统,结合了多重时间框架分析、均线系统、动量指标和波动率指标。系统通过短期与长期指数移动平均线(EMA)的交叉来识别趋势方向,使用相对强弱指标(RSI)进行超买超卖判断,结合MACD进行动量确认,并利用更高时间框架EMA作为趋势过滤器。系统采用基于ATR的动态止损和获利方案,可以根据市场波动性自适应调整。

策略原理

策略采用多层验证机制进行交易决策: 1. 趋势识别层:使用9期和21期EMA的交叉来捕捉趋势变化 2. 动量确认层:通过MACD指标(12,26,9)的交叉和方向验证趋势动量 3. 超买超卖过滤:利用RSI(14)指标在70/30水平进行过滤 4. 高时间框架确认:可选择性地使用日线级别EMA作为趋势过滤器 5. 风险管理层:使用1.5倍ATR作为追踪止损,2倍ATR设置获利目标

系统在满足多重条件后才会开仓:EMA交叉、RSI未到极值、MACD方向正确且高时间框架趋势确认。出场采用追踪止损和固定获利目标相结合的方式。

策略优势

- 多重验证机制显著降低假信号

- 高时间框架趋势过滤提升胜率

- 基于波动率的动态止损适应性强

- 完整的风险管理体系

- 参数可根据不同市场特征灵活调整

- 支持双向交易,可适应不同市场环境

- 指标组合既照顾趋势又关注动量

策略风险

- 多重条件可能导致错过部分交易机会

- 在震荡市场中可能频繁交易

- 参数优化可能导致过度拟合

- 高时间框架确认可能导致入场延迟 解决方案:

- 根据不同市场特征动态调整参数

- 增加交易方向选择的灵活性

- 引入波动率过滤机制

- 优化参数自适应机制

策略优化方向

- 引入波动率过滤机制,在高波动期间调整仓位

- 开发参数自适应机制,根据市场状态动态调整

- 增加成交量指标确认信号有效性

- 优化高时间框架趋势判断逻辑

- 完善止损方案,考虑增加时间止损

- 开发策略性能评估模块

总结

该策略是一个完整的趋势跟踪交易系统,通过多重技术指标的组合和严格的风险管理制度,能够在趋势市场中获得稳定收益。系统的可扩展性强,通过优化可以适应不同的市场环境。建议在实盘交易前进行充分的回测和参数优化。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-24 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Trend Following with ATR, MTF Confirmation, and MACD", overlay=true)

// Parameters

emaShortPeriod = input.int(9, title="Short EMA Period", minval=1)

emaLongPeriod = input.int(21, title="Long EMA Period", minval=1)

rsiPeriod = input.int(14, title="RSI Period", minval=1)

rsiOverbought = input.int(70, title="RSI Overbought", minval=50)

rsiOversold = input.int(30, title="RSI Oversold", minval=1)

atrPeriod = input.int(14, title="ATR Period", minval=1)

atrMultiplier = input.float(1.5, title="ATR Multiplier", minval=0.1)

takeProfitATRMultiplier = input.float(2.0, title="Take Profit ATR Multiplier", minval=0.1)

// Multi-timeframe settings

htfEMAEnabled = input.bool(true, title="Use Higher Timeframe EMA Confirmation?", inline="htf")

htfEMATimeframe = input.timeframe("D", title="Higher Timeframe", inline="htf")

// MACD Parameters

macdShortPeriod = input.int(12, title="MACD Short Period", minval=1)

macdLongPeriod = input.int(26, title="MACD Long Period", minval=1)

macdSignalPeriod = input.int(9, title="MACD Signal Period", minval=1)

// Select trade direction

tradeDirection = input.string("Both", title="Trade Direction", options=["Both", "Long", "Short"])

// Calculating indicators

emaShort = ta.ema(close, emaShortPeriod)

emaLong = ta.ema(close, emaLongPeriod)

rsiValue = ta.rsi(close, rsiPeriod)

atrValue = ta.atr(atrPeriod)

// Calculate MACD

[macdLine, macdSignalLine, _] = ta.macd(close, macdShortPeriod, macdLongPeriod, macdSignalPeriod)

// Higher timeframe EMA confirmation

htfEMALong = request.security(syminfo.tickerid, htfEMATimeframe, ta.ema(close, emaLongPeriod))

// Trading conditions

longCondition = ta.crossover(emaShort, emaLong) and rsiValue < rsiOverbought and (not htfEMAEnabled or close > htfEMALong) and macdLine > macdSignalLine

shortCondition = ta.crossunder(emaShort, emaLong) and rsiValue > rsiOversold and (not htfEMAEnabled or close < htfEMALong) and macdLine < macdSignalLine

// Plotting EMAs

plot(emaShort, title="EMA Short", color=color.green)

plot(emaLong, title="EMA Long", color=color.red)

// Plotting MACD

hline(0, "Zero Line", color=color.gray)

plot(macdLine - macdSignalLine, title="MACD Histogram", color=color.green, style=plot.style_histogram)

plot(macdLine, title="MACD Line", color=color.blue)

plot(macdSignalLine, title="MACD Signal Line", color=color.red)

// Trailing Stop-Loss and Take-Profit levels

var float trailStopLoss = na

var float trailTakeProfit = na

if (strategy.position_size > 0) // Long Position

trailStopLoss := na(trailStopLoss) ? close - atrValue * atrMultiplier : math.max(trailStopLoss, close - atrValue * atrMultiplier)

trailTakeProfit := close + atrValue * takeProfitATRMultiplier

strategy.exit("Exit Long", "Long", stop=trailStopLoss, limit=trailTakeProfit, when=shortCondition)

if (strategy.position_size < 0) // Short Position

trailStopLoss := na(trailStopLoss) ? close + atrValue * atrMultiplier : math.min(trailStopLoss, close + atrValue * atrMultiplier)

trailTakeProfit := close - atrValue * takeProfitATRMultiplier

strategy.exit("Exit Short", "Short", stop=trailStopLoss, limit=trailTakeProfit, when=longCondition)

// Strategy Entry

if (longCondition and (tradeDirection == "Both" or tradeDirection == "Long"))

strategy.entry("Long", strategy.long)

if (shortCondition and (tradeDirection == "Both" or tradeDirection == "Short"))

strategy.entry("Short", strategy.short)

// Plotting Buy/Sell signals

plotshape(series=longCondition, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(series=shortCondition, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// Plotting Trailing Stop-Loss and Take-Profit levels

plot(strategy.position_size > 0 ? trailStopLoss : na, title="Long Trailing Stop Loss", color=color.red, linewidth=2, style=plot.style_line)

plot(strategy.position_size < 0 ? trailStopLoss : na, title="Short Trailing Stop Loss", color=color.green, linewidth=2, style=plot.style_line)

plot(strategy.position_size > 0 ? trailTakeProfit : na, title="Long Take Profit", color=color.blue, linewidth=2, style=plot.style_line)

plot(strategy.position_size < 0 ? trailTakeProfit : na, title="Short Take Profit", color=color.orange, linewidth=2, style=plot.style_line)

相关推荐