Dynamic RSI Smart Timing Swing Trading Strategy

Author: ChaoZhang, Date: 2024-12-12 11:32:55Tags: RSISMAEMAVWMAWMASMMABBRMA

Overview

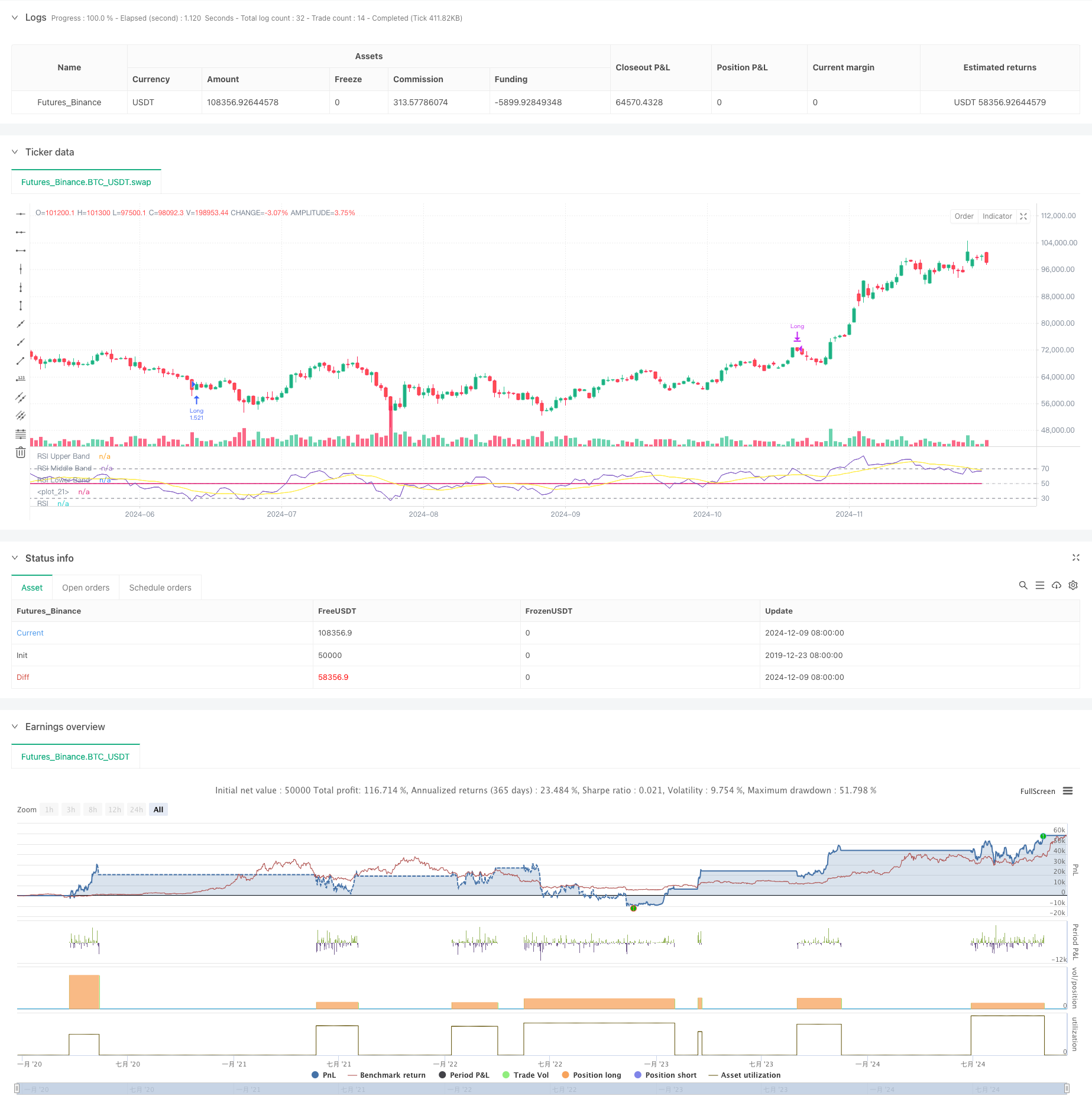

This strategy is an intelligent trading system based on the Relative Strength Index (RSI), combining various moving averages and Bollinger Bands to time trades by identifying market overbought and oversold zones. The core mechanism relies on RSI breakthrough and pullback signals, complemented by different types of moving averages for trend confirmation, enabling efficient swing trading. The strategy demonstrates strong adaptability and can be adjusted for different market conditions.

Strategy Principle

The strategy utilizes a 14-period RSI as its core indicator, generating trading signals by monitoring RSI crossovers with key levels at 30 and 70. A long signal is triggered when RSI breaks above 30, indicating a shift from oversold to bullish conditions. A closing signal is generated when RSI falls below 70, suggesting a transition from overbought to bearish conditions. The strategy incorporates various moving averages (SMA, EMA, SMMA, WMA, VWMA) and Bollinger Bands as supplementary indicators for trend confirmation and volatility assessment.

Strategy Advantages

- Clear Signals: RSI’s overbought and oversold signals are distinct and easy to understand

- Risk Control: Well-defined entry and exit conditions enable effective risk management

- Flexibility: Support for multiple moving average types allows adaptation to market conditions

- Adaptability: Bollinger Bands automatically adjust trading ranges based on market volatility

- Easy Optimization: Strong parameter customization facilitates market-specific adjustments

Strategy Risks

- Sideways Market Risk: May generate frequent false breakout signals in ranging markets

- Trend Continuation Risk: Early exits might miss extended trend movements

- Parameter Sensitivity: Different parameter settings can significantly affect strategy performance

- Slippage Impact: Less liquid markets may experience significant slippage

- Systematic Risk: Consecutive losses possible in extreme market conditions

Strategy Optimization Directions

- Volume Integration: Confirm signal validity through volume analysis

- Trend Filter Addition: Incorporate longer-term trend analysis to avoid counter-trend trades

- Stop-Loss Enhancement: Implement dynamic stop-loss mechanisms for improved capital efficiency

- Position Management Refinement: Adjust position sizes based on market volatility

- Market Sentiment Integration: Combine additional technical indicators to improve signal accuracy

Summary

This strategy captures market overbought and oversold opportunities through the RSI indicator, confirming signals with multiple technical indicators, demonstrating strong practicality and reliability. The strategy design thoroughly considers risk control and can adapt to various market environments through parameter optimization and indicator combinations. Traders are advised to conduct comprehensive backtesting before live implementation and adjust parameters according to specific market characteristics.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Demo GPT - Relative Strength Index", shorttitle="RSI Strategy", overlay=false, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_value=0.1, slippage=3)

// Inputs

rsiLengthInput = input.int(14, minval=1, title="RSI Length", group="RSI Settings")

rsiSourceInput = input.source(close, "Source", group="RSI Settings")

calculateDivergence = input.bool(false, title="Calculate Divergence", group="RSI Settings", tooltip="Calculating divergences is needed in order for divergence alerts to fire.")

// RSI Calculation

change = ta.change(rsiSourceInput)

up = ta.rma(math.max(change, 0), rsiLengthInput)

down = ta.rma(-math.min(change, 0), rsiLengthInput)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

// RSI Plots

rsiPlot = plot(rsi, "RSI", color=#7E57C2)

rsiUpperBand = hline(70, "RSI Upper Band", color=#787B86)

midline = hline(50, "RSI Middle Band", color=color.new(#787B86, 50))

rsiLowerBand = hline(30, "RSI Lower Band", color=#787B86)

fill(rsiUpperBand, rsiLowerBand, color=color.rgb(126, 87, 194, 90), title="RSI Background Fill")

plot(50, color=na, editable=false, display=display.none)

// Moving Averages

maTypeInput = input.string("SMA", "Type", options=["None", "SMA", "SMA + Bollinger Bands", "EMA", "SMMA (RMA)", "WMA", "VWMA"], group="Moving Average")

maLengthInput = input.int(14, "Length", group="Moving Average")

bbMultInput = input.float(2.0, "BB StdDev", minval=0.001, maxval=50, step=0.5, group="Moving Average")

enableMA = maTypeInput != "None"

isBB = maTypeInput == "SMA + Bollinger Bands"

// MA Calculation

ma(source, length, MAtype) =>

switch MAtype

"SMA" => ta.sma(source, length)

"SMA + Bollinger Bands" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

smoothingMA = enableMA ? ma(rsi, maLengthInput, maTypeInput) : na

smoothingStDev = isBB ? ta.stdev(rsi, maLengthInput) * bbMultInput : na

plot(smoothingMA, "RSI-based MA", color=color.yellow, display=enableMA ? display.all : display.none)

bbUpperBand = plot(smoothingMA + smoothingStDev, title="Upper Bollinger Band", color=color.green, display=isBB ? display.all : display.none)

bbLowerBand = plot(smoothingMA - smoothingStDev, title="Lower Bollinger Band", color=color.green, display=isBB ? display.all : display.none)

fill(bbUpperBand, bbLowerBand, color=isBB ? color.new(color.green, 90) : na, title="Bollinger Bands Background Fill", display=isBB ? display.all : display.none)

// Trade Logic

longCondition = ta.crossover(rsi, 30)

exitCondition = ta.crossunder(rsi, 70)

// Start Date & End Date

startDate = input(timestamp("2018-01-01 00:00"), "Start Date", group="Date Range")

endDate = input(timestamp("2069-12-31 23:59"), "End Date", group="Date Range")

inDateRange = true

// Execute Trades

if (longCondition and inDateRange)

strategy.entry("Long", strategy.long)

if (exitCondition and inDateRange)

strategy.close("Long")

- Bollinger Bands and Moving Average Crossover Strategy

- Advanced Quantitative Trading Strategy Combining RSI Divergence and Moving Averages

- Multi-Indicator Adaptive Trading Strategy Based on RSI, MACD and Volume

- Multi-Indicator Synergistic Trading Strategy with Bollinger Bands, Fibonacci, MACD and RSI

- Dual Moving Average Momentum Tracking Quantitative Strategy

- Multi-Period Moving Average Crossover Trend Following Strategy

- Adaptive Moving Average Crossover Strategy

- Multi-Moving Average Crossover Trend Following Strategy with Volatility Filter

- BB Breakout Strategy

- MACD and RSI Combined Natural Trading Strategy

- Multi-Target Intelligent Volume Momentum Trading Strategy

- Multi-Period Bollinger Bands Touch Trend Reversal Quantitative Trading Strategy

- High-Frequency Breakout Trading Strategy Based on Candlestick Close Direction

- Advanced Dynamic Fibonacci Retracement Trend Quantitative Trading Strategy

- Variable Index Dynamic Average Multi-Tier Profit Trend Following Strategy

- Multi Moving Average Trading System with Momentum and Volume Confirmation Quantitative Trend Strategy

- Adaptive Trailing Drawdown Balanced Trading Strategy with Take-Profit and Stop-Loss

- Enhanced Trend Following System: Dynamic Trend Identification Based on ADX and Parabolic SAR

- Dual Timeframe Stochastic Momentum Trading Strategy

- Adaptive Bollinger Bands Dynamic Position Management Strategy

- Bidirectional Trading Strategy Based on Candlestick Absorption Pattern Analysis

- Bollinger Breakout with Mean Reversion 4H Quantitative Trading Strategy

- Trend Following Dynamic Grid Position Sizing Strategy

- Dual BBI (Bulls and Bears Index) Crossover Strategy

- Dynamic Long/Short Swing Trading Strategy with Moving Average Crossover Signal System

- Multi-Technical Indicator Trend Following Trading Strategy

- Advanced Volatility Mean Reversion Trading Strategy: Multi-Dimensional Quantitative Trading System Based on VIX and Moving Average

- Gold Trend Channel Reversal Momentum Strategy

- Advanced EMA Momentum Trend Trading Strategy

- Multi-MA Trend Intensity Trading Strategy - A Flexible Smart Trading System Based on MA Deviation