Stratégie de prévision croisée des oscillations dynamiques du MACD

Auteur:ChaoZhang est là., Date: 2024-11-27 14:54:02 Je suis désoléLes étiquettes:Le MACDLe taux d'intérêtSMAROC

Résumé

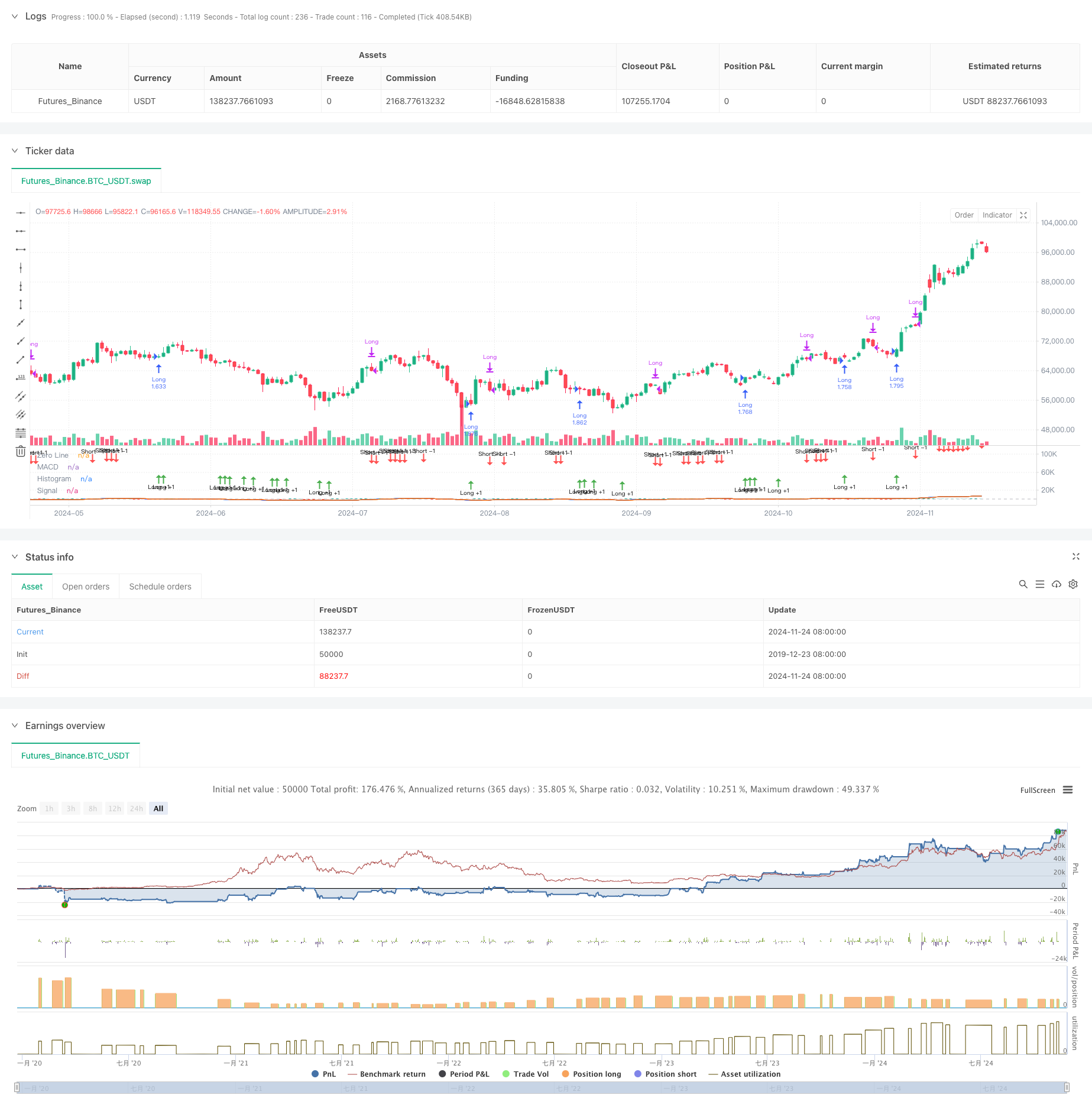

Cette stratégie base les décisions de trading sur les caractéristiques dynamiques de l'indicateur MACD (Moving Average Convergence Divergence). L'approche de base se concentre sur l'observation des changements dans l'histogramme MACD pour prédire les croisements potentiels d'or et de mort, permettant l'établissement précoce de positions.

Principes de stratégie

La stratégie utilise un système d'indicateur MACD modifié, incorporant la différence entre les moyennes mobiles rapides (EMA12) et lentes (EMA26), ainsi qu'une ligne de signal à 2 périodes.

- Calcul du taux de changement de l'histogramme (hist_change) pour juger de la dynamique de la tendance

- Anticiper les signaux de croisement doré en entrant dans des positions longues lorsque l'histogramme est négatif et montre une tendance à la hausse pendant trois périodes consécutives

- Anticiper les signaux croisés de mort en clôturant les positions lorsque l'histogramme est positif et montre une tendance à la baisse pendant trois périodes consécutives

- Mise en œuvre d'un mécanisme de filtrage temporel pour ne négocier que dans des intervalles de temps déterminés

Les avantages de la stratégie

- Prédiction des signaux puissants: Anticipe les signaux croisés potentiels en observant la dynamique des histogrammes, améliorant le moment de l'entrée

- Contrôle raisonnable des risques: comprend une commission de 0,1% et un décalage de 3 points, reflétant des conditions de négociation réalistes

- Gestion souple des capitaux: utilise une dimensionnement des positions basée sur le pourcentage par rapport au fonds propres du compte pour un contrôle efficace des risques

- Excellente visualisation: utilise des histogrammes codés par couleur et des marqueurs de flèches pour les signaux commerciaux, facilitant l'analyse

Risques stratégiques

- Risque de fausse rupture: des signaux erronés fréquents peuvent se produire sur différents marchés

- Risque de retard: Malgré les mécanismes prédictifs, le MACD conserve un certain retard inhérent

- Dépendance de l'environnement du marché: la stratégie fonctionne mieux sur les marchés tendance, potentiellement moins bien dans des conditions variables

- Sensibilité des paramètres: la performance de la stratégie dépend fortement des réglages de la période de ligne rapide et lente

Directions d'optimisation

- Filtrage de l'environnement du marché: ajout d'indicateurs d'identification des tendances pour ajuster les paramètres de négociation en fonction des conditions du marché

- Amélioration de la gestion de la position: mise en œuvre d'une dimensionnement dynamique de la position basée sur la force du signal

- Mise en œuvre du stop loss: ajouter des stops de retard ou des stops fixes pour contrôler le retrait

- Amélioration de la confirmation du signal: inclure des indicateurs techniques supplémentaires pour la validation croisée

- Optimisation des paramètres: mettre en œuvre des paramètres adaptatifs qui s'ajustent en fonction des conditions du marché

Résumé

Cette stratégie utilise de manière innovante les caractéristiques dynamiques de l'histogramme MACD pour améliorer les systèmes de trading traditionnels MACD. Le mécanisme prédictif fournit des signaux d'entrée plus tôt, tandis que des conditions de trading strictes et des mesures de contrôle des risques assurent la stabilité de la stratégie.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-25 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Demo GPT - Moving Average Convergence Divergence", shorttitle="MACD", commission_type=strategy.commission.percent, commission_value=0.1, slippage=3, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Getting inputs

fast_length = input(title="Fast Length", defval=12)

slow_length = input(title="Slow Length", defval=26)

src = input(title="Source", defval=close)

signal_length = input.int(title="Signal Smoothing", minval=1, maxval=50, defval=2) // Set smoothing line to 2

sma_source = input.string(title="Oscillator MA Type", defval="EMA", options=["SMA", "EMA"])

sma_signal = input.string(title="Signal Line MA Type", defval="EMA", options=["SMA", "EMA"])

// Date inputs

start_date = input(title="Start Date", defval=timestamp("2018-01-01T00:00:00"))

end_date = input(title="End Date", defval=timestamp("2069-12-31T23:59:59"))

// Calculating

fast_ma = sma_source == "SMA" ? ta.sma(src, fast_length) : ta.ema(src, fast_length)

slow_ma = sma_source == "SMA" ? ta.sma(src, slow_length) : ta.ema(src, slow_length)

macd = fast_ma - slow_ma

signal = sma_signal == "SMA" ? ta.sma(macd, signal_length) : ta.ema(macd, signal_length)

hist = macd - signal

// Strategy logic

isInDateRange = true

// Calculate the rate of change of the histogram

hist_change = hist - hist[1]

// Anticipate a bullish crossover: histogram is negative, increasing, and approaching zero

anticipate_long = isInDateRange and hist < 0 and hist_change > 0 and hist > hist[1] and hist > hist[2]

// Anticipate an exit (bearish crossover): histogram is positive, decreasing, and approaching zero

anticipate_exit = isInDateRange and hist > 0 and hist_change < 0 and hist < hist[1] and hist < hist[2]

if anticipate_long

strategy.entry("Long", strategy.long)

if anticipate_exit

strategy.close("Long")

// Plotting

hline(0, "Zero Line", color=color.new(#787B86, 50))

plot(hist, title="Histogram", style=plot.style_columns, color=(hist >= 0 ? (hist > hist[1] ? #26A69A : #B2DFDB) : (hist < hist[1] ? #FF5252 : #FFCDD2)))

plot(macd, title="MACD", color=#2962FF)

plot(signal, title="Signal", color=#FF6D00)

// Plotting arrows when anticipating the crossover

plotshape(anticipate_long, title="Long +1", location=location.belowbar, color=color.green, style=shape.arrowup, size=size.tiny, text="Long +1")

plotshape(anticipate_exit, title="Short -1", location=location.abovebar, color=color.red, style=shape.arrowdown, size=size.tiny, text="Short -1")

- Indicateur d'inversion de K I

- Indicateur MACD personnalisé CM - Cadre temporel multiple - V2

- Système de négociation de confirmation de tendance MACD double

- Stratégie courte longue du MACD ZeroLag

- Stratégie de négociation à double croisement MACD à retard zéro - négociation à haute fréquence basée sur la capture de tendance à court terme

- La moyenne mobile croisée + la stratégie de dynamique de la ligne lente du MACD

- Système de négociation dynamique MACD à intervalles multiples de stop-loss et de take-profit

- Stratégie de combinaison MACD et Martingale pour une négociation longue optimisée

- Stratégie de négociation quantitative réglable en fonction de la date de croisement de la moyenne mobile MACD double

- Stratégie de rupture du MACD BB

- Stratégie de négociation quantitative de suivi de tendance et d' intégration de l' élan

- Stratégie de négociation dynamique basée sur Z-Score et Supertrend: système de commutation longue courte

- Évasion de Bollinger adaptative avec système de stratégie quantitative de moyenne mobile

- Système de négociation adaptatif stop-loss optimisé par l'IA avec intégration d'indicateurs techniques multiples

- Crossover des moyennes mobiles à plusieurs périodes avec système d'analyse du volume

- Stratégie quantitative de suivi de l'élan de la moyenne mobile double

- La stratégie de croisement double des moyennes mobiles avec stop-loss et take-profit adaptatifs

- Tendance d' adaptation suivant une stratégie basée sur un oscillateur de dynamique

- Stratégie de volume-prix croisée de tendance PVT-EMA

- Système de négociation quantitative croisée dynamique à plusieurs périodes MACD-EMA

- Système de négociation dynamique d'action des prix VWAP-ATR

- Stratégie quantitative de tendance dynamique basée sur les bandes de Bollinger et le signe croisé RSI

- La valeur de l'échange de titres est la valeur de l'échange de titres.

- Système de stratégie de négociation dynamique basé sur l'indicateur SAR parabolique

- Système de négociation quantitative de volatilité et de dynamique adaptative (AVMQTS)

- Stratégie de négociation de tendance avancée basée sur les bandes de Bollinger et les modèles de chandeliers

- Volatilité ATR et tendance d'adaptation basée sur la moyenne mobile à la suite de la stratégie de sortie

- Stratégie de négociation de tendance à double dynamique EMA avec système de signaux à bougie entière

- Supertrend à double échéancier avec système d'optimisation RSI

- La valeur de la valeur de l'actif détenu par la banque est la valeur de l'actif détenu par la banque.