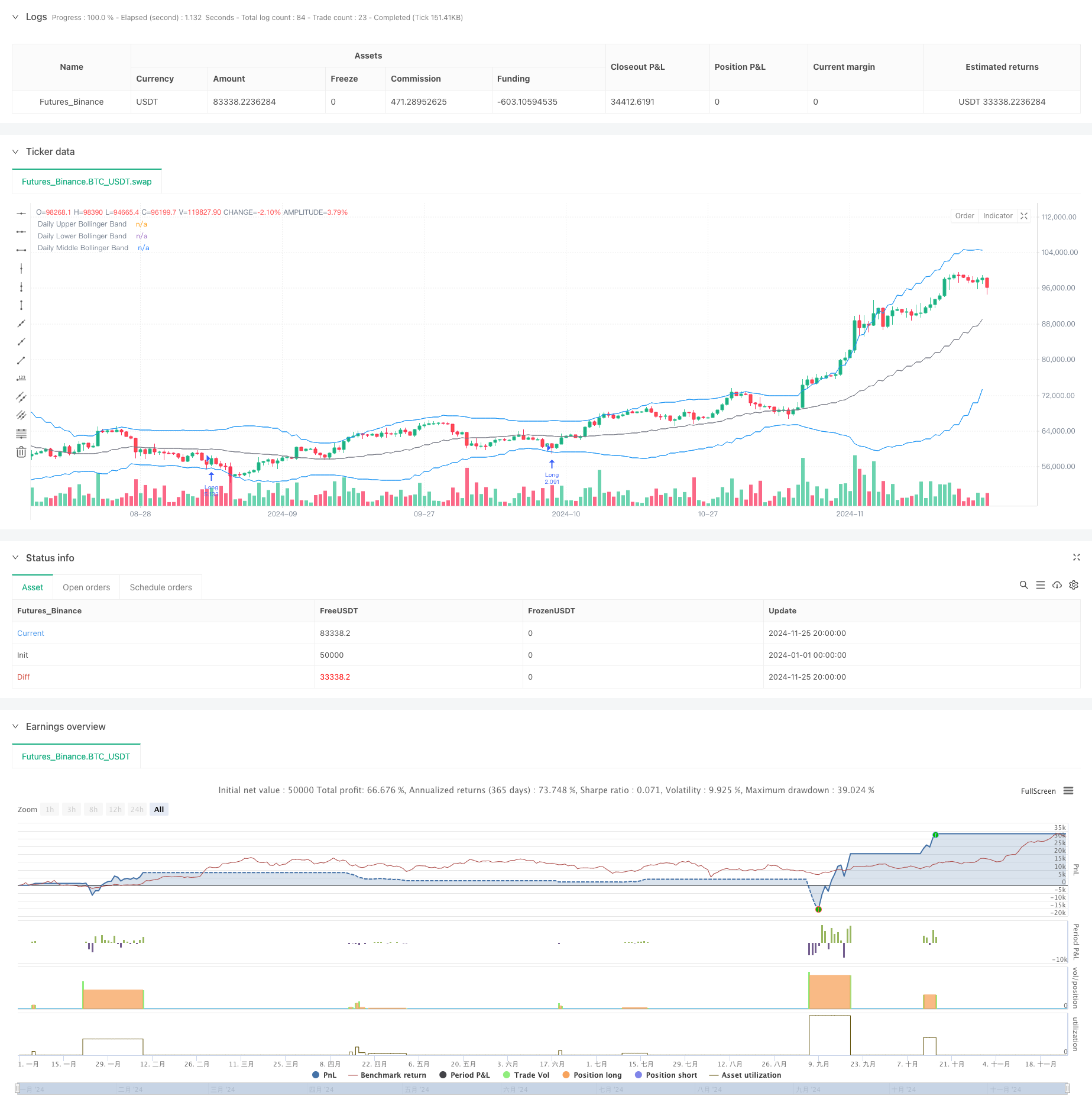

概述

这是一个基于玻林格带与蜡烛图形态分析的趋势跟踪策略。策略主要通过观察价格触及玻林格带时的蜡烛图形态特征,结合上下引线与实体的比率关系来判断市场可能的反转点。同时,策略采用了固定风险模型来控制每笔交易的风险敞口,并通过多重时间周期分析来提高交易的准确性。

策略原理

策略的核心逻辑基于以下几个关键要素:首先,通过计算20周期的玻林格带来确定价格波动的范围;其次,在价格触及玻林格带时,分析蜡烛图的上下引线与实体的比率,当比率超过设定阈值时,视为潜在的反转信号;第三,通过计算关键支撑位和阻力位来设置止损点位;最后,根据账户总额的固定比例(1%)来计算每笔交易的持仓量,实现风险的动态管理。该策略还提供了多种入场时机选择,包括收盘价、开盘价、日内最高价和最低价等。

策略优势

- 风险控制精确:采用固定比例风险管理模型,确保每笔交易的风险敞口都在可控范围内

- 入场点位灵活:提供多种入场价格选择,能够适应不同的交易风格

- 技术指标结合:将玻林格带与蜡烛图形态分析相结合,提高信号的可靠性

- 止损设置合理:通过关键支撑阻力位设置止损,符合市场运行规律

- 交易管理完善:包含订单到期机制,避免过期信号带来的误操作

策略风险

- 市场快速波动风险:在剧烈波动市场中,引线比率可能产生虚假信号

- 资金管理风险:固定比例风险模型在连续亏损情况下可能导致仓位过小

- 止损设置风险:支撑阻力位的计算可能在某些市场条件下不够准确

- 时间周期依赖:策略主要基于日线级别,可能错过更小时间框架的机会

策略优化方向

- 引入成交量指标:可以通过在信号确认时增加成交量分析,提高信号的可靠性

- 优化止损机制:考虑引入动态止损,根据市场波动度自动调整止损距离

- 增加市场环境过滤:添加趋势强度指标,在不同市场环境下调整策略参数

- 完善仓位管理:考虑引入动态仓位管理机制,根据市场波动性调整风险敞口

- 增加时间过滤:可以添加时间过滤器,避免在市场波动较大的时段交易

总结

该策略通过将经典的技术分析工具与现代风险管理方法相结合,构建了一个相对完善的交易系统。策略的核心优势在于其严格的风险控制和灵活的入场机制,但同时也需要在实际应用中注意市场环境的变化和信号的可靠性验证。通过建议的优化方向,策略还有进一步提升的空间,特别是在信号过滤和风险管理方面。

策略源码

/*backtest

start: 2024-01-01 00:00:00

end: 2024-11-26 00:00:00

period: 12h

basePeriod: 12h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Trade Entry Detector, based on Wick to Body Ratio when price tests Bollinger Bands", overlay=true, default_qty_type=strategy.fixed)

// Input for primary analysis time frame

timeFrame = "D" // Daily time frame

// Bollinger Band settings

length = input.int(20, title="Bollinger Band Length", minval=1)

mult = input.float(2.0, title="Standard Deviation Multiplier", minval=0.1)

source = input(close, title="Source")

// Entry ratio settings

wickToBodyRatio = input.float(1.0, title="Minimum Wick-to-Body Ratio", minval=0)

// Order Fill Timing Option

fillOption = input.string("Daily Close", title="Order Fill Timing", options=["Daily Close", "Daily Open", "HOD", "LOD"])

// Account and risk settings

accountBalance = 100000 // Account balance in dollars

riskPercentage = 1.0 // Risk percentage per trade

riskAmount = (riskPercentage / 100) * accountBalance // Fixed 1% risk amount

// Request daily data for calculations

dailyHigh = request.security(syminfo.tickerid, timeFrame, high)

dailyLow = request.security(syminfo.tickerid, timeFrame, low)

dailyClose = request.security(syminfo.tickerid, timeFrame, close)

dailyOpen = request.security(syminfo.tickerid, timeFrame, open)

// Calculate Bollinger Bands on the daily time frame

dailyBasis = request.security(syminfo.tickerid, timeFrame, ta.sma(source, length))

dailyDev = mult * request.security(syminfo.tickerid, timeFrame, ta.stdev(source, length))

dailyUpperBand = dailyBasis + dailyDev

dailyLowerBand = dailyBasis - dailyDev

// Calculate the body and wick sizes on the daily time frame

dailyBodySize = math.abs(dailyOpen - dailyClose)

dailyUpperWickSize = dailyHigh - math.max(dailyOpen, dailyClose)

dailyLowerWickSize = math.min(dailyOpen, dailyClose) - dailyLow

// Conditions for a candle with an upper wick or lower wick that touches the Bollinger Bands

upperWickCondition = (dailyUpperWickSize / dailyBodySize >= wickToBodyRatio) and (dailyHigh > dailyUpperBand)

lowerWickCondition = (dailyLowerWickSize / dailyBodySize >= wickToBodyRatio) and (dailyLow < dailyLowerBand)

// Define the swing high and swing low for stop loss placement

var float swingLow = na

var float swingHigh = na

if (ta.pivothigh(dailyHigh, 5, 5))

swingHigh := dailyHigh[5]

if (ta.pivotlow(dailyLow, 5, 5))

swingLow := dailyLow[5]

// Determine entry price based on chosen fill option

var float longEntryPrice = na

var float shortEntryPrice = na

if lowerWickCondition

longEntryPrice := fillOption == "Daily Close" ? dailyClose :

fillOption == "Daily Open" ? dailyOpen :

fillOption == "HOD" ? dailyHigh : dailyLow

if upperWickCondition

shortEntryPrice := fillOption == "Daily Close" ? dailyClose :

fillOption == "Daily Open" ? dailyOpen :

fillOption == "HOD" ? dailyHigh : dailyLow

// Execute the long and short entries with expiration

var int longOrderExpiry = na

var int shortOrderExpiry = na

if not na(longEntryPrice)

longOrderExpiry := bar_index + 2 // Order expires after 2 days

if not na(shortEntryPrice)

shortOrderExpiry := bar_index + 2 // Order expires after 2 days

// Check expiration and execute orders

if (longEntryPrice and bar_index <= longOrderExpiry and high >= longEntryPrice)

longStopDistance = close - nz(swingLow, close)

longPositionSize = longStopDistance > 0 ? riskAmount / longStopDistance : na

if (not na(longPositionSize))

strategy.entry("Long", strategy.long, qty=longPositionSize)

longEntryPrice := na // Reset after entry

if (shortEntryPrice and bar_index <= shortOrderExpiry and low <= shortEntryPrice)

shortStopDistance = nz(swingHigh, close) - close

shortPositionSize = shortStopDistance > 0 ? riskAmount / shortStopDistance : na

if (not na(shortPositionSize))

strategy.entry("Short", strategy.short, qty=shortPositionSize)

shortEntryPrice := na // Reset after entry

// Exit logic: hit the opposing Bollinger Band

if (strategy.position_size > 0) // Long position

strategy.exit("Exit Long", "Long", limit=dailyUpperBand)

else if (strategy.position_size < 0) // Short position

strategy.exit("Exit Short", "Short", limit=dailyLowerBand)

if (strategy.position_size > 0) // Long position

strategy.exit("Stop Loss Long", "Long", stop=swingLow)

else if (strategy.position_size < 0) // Short position

strategy.exit("Stop Loss Short", "Short", stop=swingHigh)

// Plot daily Bollinger Bands and levels on the chosen time frame

plot(dailyUpperBand, color=color.blue, linewidth=1, title="Daily Upper Bollinger Band")

plot(dailyLowerBand, color=color.blue, linewidth=1, title="Daily Lower Bollinger Band")

plot(dailyBasis, color=color.gray, linewidth=1, title="Daily Middle Bollinger Band")

相关推荐