マルチMAトレンド・インテニシティ・トレーディング・戦略 - MA偏差に基づく柔軟なスマート・トレーディング・システム

作者: リン・ハーンチャオチャン開催日:2024年12月11日17時46分33秒タグ:マルチATRHTFRRTPSL

概要

この戦略は,複数の移動平均値とトレンド強度に基づいたインテリジェントな取引システムである.この戦略は,ポジション管理とリスク管理のためのATR波動性指標と組み合わせて,異なる期間の価格と移動平均値との間の偏差を分析することによって,市場のトレンド強さを測定する.この戦略は高いカスタマイズ可能性を提供し,異なる市場環境と取引ニーズに応じてパラメータを柔軟に調整することができます.

戦略原則

戦略の基本論理は以下の側面に基づいています 1. 2つの移動平均値 (速いと遅い) を用いて,異なる期間のトレンド方向と交差信号を識別する 2. 価格と移動平均間の偏差 (ポイントで) を計算することによってトレンド強さを定量化する 3. 確認信号としてろうそくのパターン (飲み込み,ハンマー,落星,ドジ) を組み込む 4. ストップ損失と利益目標を動的に計算するためにATR指標を使用します. 5. オーダー管理のために部分利益とトレーリングストップを使用

戦略 の 利点

- システムには,異なる市場環境のためのパラメータ調整による強い適応性があります.

- 傾向の強さを測定し,傾向の弱さで頻繁に取引しないようにします.

- 信号信頼性の向上のために複数の技術指標とパターンを組み合わせます

- 合理的なリスク管理のためにATRベースのダイナミックストップ損失を使用する.

- 複合および固定位置サイズメソッドの両方をサポートします

- 利益の保護のために,部分的な利益の取得と後続的な停止の特徴

戦略リスク

- 波動シグナルを発生させる可能性があります. オシレーターフィルターを追加することを検討します.

- 複数の指標の組み合わせによって,いくつかの取引機会が失われる可能性があります.

- パラメータの過剰な最適化により,過剰な適合リスクが生じる

- 流動性が低い市場での大きな取引は,スライドリスクに直面する可能性があります.

- 過剰な単一の損失を避けるために適切なストップ損失設定が必要です.

戦略の最適化

- 増加傾向の補完的な確認として,ボリューム指標を追加することができます.

- 取引頻度を動的に調整するために波動性指標を導入することを検討

- 異なる時間枠におけるトレンド一貫性に基づいてシグナルをフィルターする

- タイムベースストップなど,より多くのストップ損失オプションを追加します.

- 戦略の適応性を向上させるための適応パラメータ最適化メカニズムを開発する

概要

この戦略は,移動平均値,トレンド強度定量化,キャンドルスタックパターン,ダイナミックリスク管理を組み合わせて包括的な取引システムを構築する.複数の確認メカニズムを通じて取引信頼性を向上させながら戦略的シンプルさを維持する.この戦略の高いカスタマイズ可能性は,異なる取引スタイルと市場環境に適応することを可能にするが,実装中にパラメータ最適化とリスク管理に注意を払わなければならない.

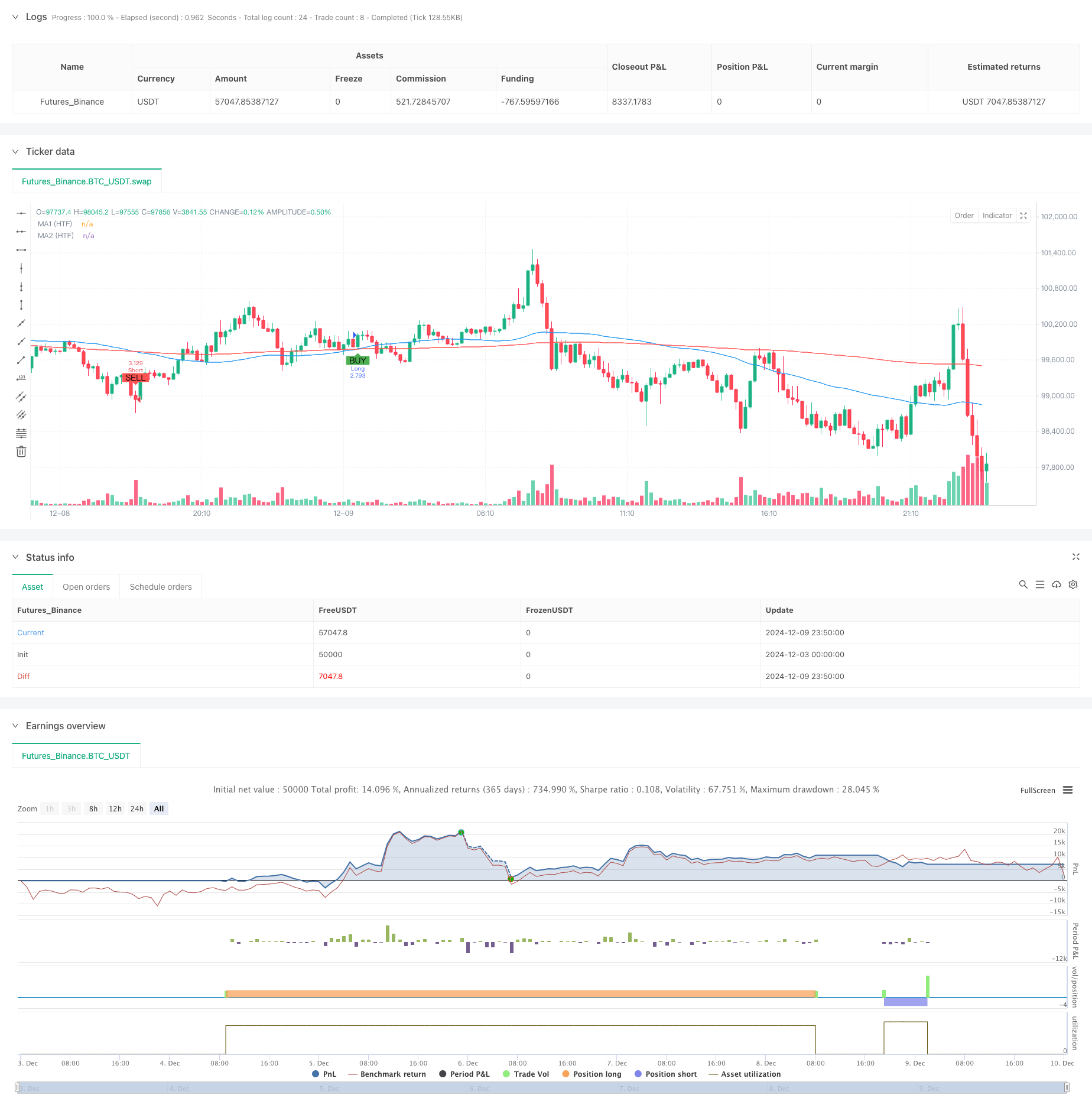

/*backtest

start: 2024-12-03 00:00:00

end: 2024-12-10 00:00:00

period: 10m

basePeriod: 10m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Customizable Strategy with Signal Intensity Based on Pips Above/Below MAs", overlay=true)

// Customizable Inputs

// Account and Risk Management

account_size = input.int(100000, title="Account Size (USD)", minval=1)

compounded_results = input.bool(true, title="Compounded Results")

risk_per_trade = input.float(1.0, title="Risk per Trade (%)", minval=0.1, maxval=100) / 100

// Moving Averages Settings

ma1_length = input.int(50, title="Moving Average 1 Length", minval=1)

ma2_length = input.int(200, title="Moving Average 2 Length", minval=1)

// Higher Time Frame for Moving Averages

ma_htf = input.timeframe("D", title="Higher Time Frame for MA Delay")

// Signal Intensity Range based on pips

signal_intensity_min = input.int(0, title="Signal Intensity Start (Pips)", minval=0, maxval=1000)

signal_intensity_max = input.int(1000, title="Signal Intensity End (Pips)", minval=0, maxval=1000)

// ATR-Based Stop Loss and Take Profit

atr_length = input.int(14, title="ATR Length", minval=1)

atr_multiplier_stop = input.float(1.5, title="Stop Loss Size (ATR Multiplier)", minval=0.1)

atr_multiplier_take_profit = input.float(2.5, title="Take Profit Size (ATR Multiplier)", minval=0.1)

// Trailing Stop and Partial Profit

trailing_stop_rr = input.float(2.0, title="Trailing Stop (R:R)", minval=0)

partial_profit_percentage = input.float(50, title="Take Partial Profit (%)", minval=0, maxval=100)

// Trend Filter Settings

trend_filter_enabled = input.bool(true, title="Trend Filter Enabled")

trend_filter_sensitivity = input.float(50, title="Trend Filter Sensitivity", minval=0, maxval=100)

// Candle Pattern Type for Entry

entry_candle_type = input.string("Any", title="Entry Candle Type", options=["Any", "Engulfing", "Hammer", "Shooting Star", "Doji"])

// Moving Average Entry Conditions

ma_entry_condition = input.string("Both", title="MA Entry", options=["Fast Above Slow", "Fast Below Slow", "Both"])

// Trade Direction (Long, Short, or Both)

trade_direction = input.string("Both", title="Trade Direction", options=["Long", "Short", "Both"])

// ATR Calculation

atr_value = ta.atr(atr_length)

// Moving Average Calculations (using Higher Time Frame)

ma1_htf = ta.sma(request.security(syminfo.tickerid, ma_htf, close), ma1_length)

ma2_htf = ta.sma(request.security(syminfo.tickerid, ma_htf, close), ma2_length)

// Candle Pattern Conditions

is_engulfing = close[1] < open[1] and close > open and high > high[1] and low < low[1]

is_hammer = (high - low) > 3 * (close - open) and (close > open) and (low == ta.lowest(low, 5))

is_shooting_star = (high - low) > 3 * (open - close) and (open > close) and (high == ta.highest(high, 5))

is_doji = (close - open) <= ((high - low) * 0.1)

// Apply the selected candle pattern

candle_condition = false

if entry_candle_type == "Any"

candle_condition := true

if entry_candle_type == "Engulfing"

candle_condition := is_engulfing

if entry_candle_type == "Hammer"

candle_condition := is_hammer

if entry_candle_type == "Shooting Star"

candle_condition := is_shooting_star

if entry_candle_type == "Doji"

candle_condition := is_doji

// Moving Average Entry Conditions

ma_cross_above = ta.crossover(ma1_htf, ma2_htf)

ma_cross_below = ta.crossunder(ma1_htf, ma2_htf)

// Calculate pips distance to MAs and normalize it for signal intensity

pip_size = syminfo.mintick * 10 // Assuming Forex; for other asset classes, modify as needed

// Calculate distances in pips between price and MAs

distance_to_ma1_pips = math.abs(close - ma1_htf) / pip_size

distance_to_ma2_pips = math.abs(close - ma2_htf) / pip_size

// Calculate signal intensity based on the pips distance

// Normalize the signal intensity between the user-specified min and max

signal_intensity = math.min(math.max((distance_to_ma1_pips + distance_to_ma2_pips), signal_intensity_min), signal_intensity_max)

// Trend Filter Condition (Optional)

trend_condition = false

if trend_filter_enabled

trend_condition := ta.sma(close, ma2_length) > ta.sma(close, ma2_length + int(trend_filter_sensitivity))

// Entry Conditions Based on MA, Candle Patterns, and Trade Direction

long_condition = (trade_direction == "Long" or trade_direction == "Both") and (ma_entry_condition == "Fast Above Slow" or ma_entry_condition == "Both") and ma_cross_above and candle_condition and (not trend_filter_enabled or trend_condition) and signal_intensity > signal_intensity_min

short_condition = (trade_direction == "Short" or trade_direction == "Both") and (ma_entry_condition == "Fast Below Slow" or ma_entry_condition == "Both") and ma_cross_below and candle_condition and (not trend_filter_enabled or not trend_condition) and signal_intensity > signal_intensity_min

// Position Sizing Based on Risk Per Trade and ATR for Stop Loss

risk_amount = account_size * risk_per_trade

stop_loss_atr = atr_multiplier_stop * atr_value

// Calculate the position size based on the risk amount and ATR stop loss

position_size = risk_amount / stop_loss_atr

// If compounded results are not enabled, adjust position size for non-compounded returns

if not compounded_results

position_size := position_size / account_size * 100000 // Adjust for non-compounded results

// Convert take profit and stop loss from ATR to USD

pip_value = syminfo.mintick * 10 // Assuming Forex; for other asset classes, modify as needed

take_profit_atr = atr_multiplier_take_profit * atr_value

take_profit_usd = (take_profit_atr * pip_value) * position_size

stop_loss_usd = (stop_loss_atr * pip_value) * position_size

// Trailing Stop

trail_stop_level = trailing_stop_rr * stop_loss_atr

// Initialize long_box_id and short_box_id as boxes (not ints)

var box long_box_id = na

var box short_box_id = na

// Track Monthly Profit

var float monthly_profit = 0.0

if (month(timenow) != month(timenow[1])) // New month

monthly_profit := 0

// Long Trade Management

if long_condition

strategy.entry("Long", strategy.long, qty=position_size)

// Partial Profit at 50% position close when 1:1 risk/reward

strategy.exit("Partial Profit", from_entry="Long", limit=strategy.position_avg_price + stop_loss_atr, qty_percent=partial_profit_percentage / 100)

// Full take profit and stop loss with trailing stop

strategy.exit("Take Profit Long", from_entry="Long", limit=strategy.position_avg_price + take_profit_atr, stop=strategy.position_avg_price - stop_loss_atr, trail_offset=trail_stop_level)

// Delete the old box if it exists

if not na(long_box_id)

box.delete(long_box_id)

// Plot Take Profit and Stop Loss for Long Positions

// long_box_id := box.new(left=bar_index - 1, top=strategy.position_avg_price + take_profit_atr, right=bar_index, bottom=strategy.position_avg_price - stop_loss_atr, bgcolor=color.new(color.green, 90), border_width=1, border_color=color.new(color.green, 0))

// Short Trade Management

if short_condition

strategy.entry("Short", strategy.short, qty=position_size)

// Partial Profit at 50% position close when 1:1 risk/reward

strategy.exit("Partial Profit", from_entry="Short", limit=strategy.position_avg_price - stop_loss_atr, qty_percent=partial_profit_percentage / 100)

// Full take profit and stop loss with trailing stop

strategy.exit("Take Profit Short", from_entry="Short", limit=strategy.position_avg_price - take_profit_atr, stop=strategy.position_avg_price + stop_loss_atr, trail_offset=trail_stop_level)

// Delete the old box if it exists

// if not na(short_box_id)

// box.delete(short_box_id)

// Plot Take Profit and Stop Loss for Short Positions

// short_box_id := box.new(left=bar_index - 1, top=strategy.position_avg_price + stop_loss_atr, right=bar_index, bottom=strategy.position_avg_price - take_profit_atr, bgcolor=color.new(color.red, 90), border_width=1, border_color=color.new(color.red, 0))

// Plot MAs and Signals

plot(ma1_htf, color=color.blue, title="MA1 (HTF)")

plot(ma2_htf, color=color.red, title="MA2 (HTF)")

plotshape(series=long_condition, location=location.belowbar, color=color.green, style=shape.labelup, title="Buy Signal", text="BUY")

plotshape(series=short_condition, location=location.abovebar, color=color.red, style=shape.labeldown, title="Sell Signal", text="SELL")

関連性

- ダイナミックなサポートとレジスタンスの取引システムを持つ適応チャネルブレークアウト戦略

- Fibonacci リトレースメント レベルに基づく定量的な取引戦略を伴う多条件トレンド

- 移動平均のクロスオーバーに基づくリスク/報酬比最適化戦略

- ダイナミックなリスクマネジメントを伴う二重移動平均のクロスオーバー戦略

- ATR ベースのダイナミックストップ・ロスの最適化による二重 EMA プルバック・トレーディングシステム

- 動的リスク管理の指数関数移動平均のクロスオーバー戦略

- ATRベースのリスク管理システムによる戦略をフォローする二重移動平均傾向

- 強化された二重ピボットポイント逆転取引戦略

- 固定ストップ・ロスの最適化モデルによる動的移動平均値とボリンジャー・バンドのクロス戦略

- 2つのRSI指標に基づく適応範囲取引システム

もっと

- ダイナミック RSI スマートタイム スウィング トレーディング 戦略

- 2方向取引戦略 キャンドルスティック吸収パターン分析に基づく

- Bollinger Breakout with Mean Reversion 4H 定量取引戦略

- ダイナミックグリッド位置サイズ戦略の傾向

- 双重BBI (bulls and bears index) クロスオーバー戦略

- 動的ロング/ショート・スウィング・トレーディング・ストラテジー

- 取引戦略をフォローするマルチテクニカル指標傾向

- 先進的な波動性平均逆転取引戦略:VIXと移動平均値に基づく多次元量的な取引システム

- 金のトレンドチャネル逆転のモメンタム戦略

- 先進的なEMAモメンタムトレンド取引戦略

- ボリューム重量化二重傾向検出システム

- 多要素対トレンド取引戦略

- 強化されたモメントオシレーターとストカスティックディバージェンスの定量取引戦略

- トレンドブレイク・トレード戦略によるマルチタイムフレームフィボナッチ・リトラセメント

- 多指標の傾向 利益の最適化による戦略

- フラクタル・ブレイクアウト・モメンタム・トレーディング・戦略

- チェンデ・モメンタム・オシレーターに基づいた適応型平均逆転取引戦略

- 取引戦略をフォローするMACD-スーパートレンド 双重確認傾向

- 多期スーパートレンド・ダイナミック・トレーディング・戦略

- Fibonacci リトラセッションとピボットポイント取引戦略のマルチタイムフレーム EMA