Bull Bear Power Trading Strategy dengan Volume-Percentile Based Dynamic Take-Profit System

Penulis:ChaoZhang, Tanggal: 2025-01-06 16:16:04Tag:BBPEMAATRTP

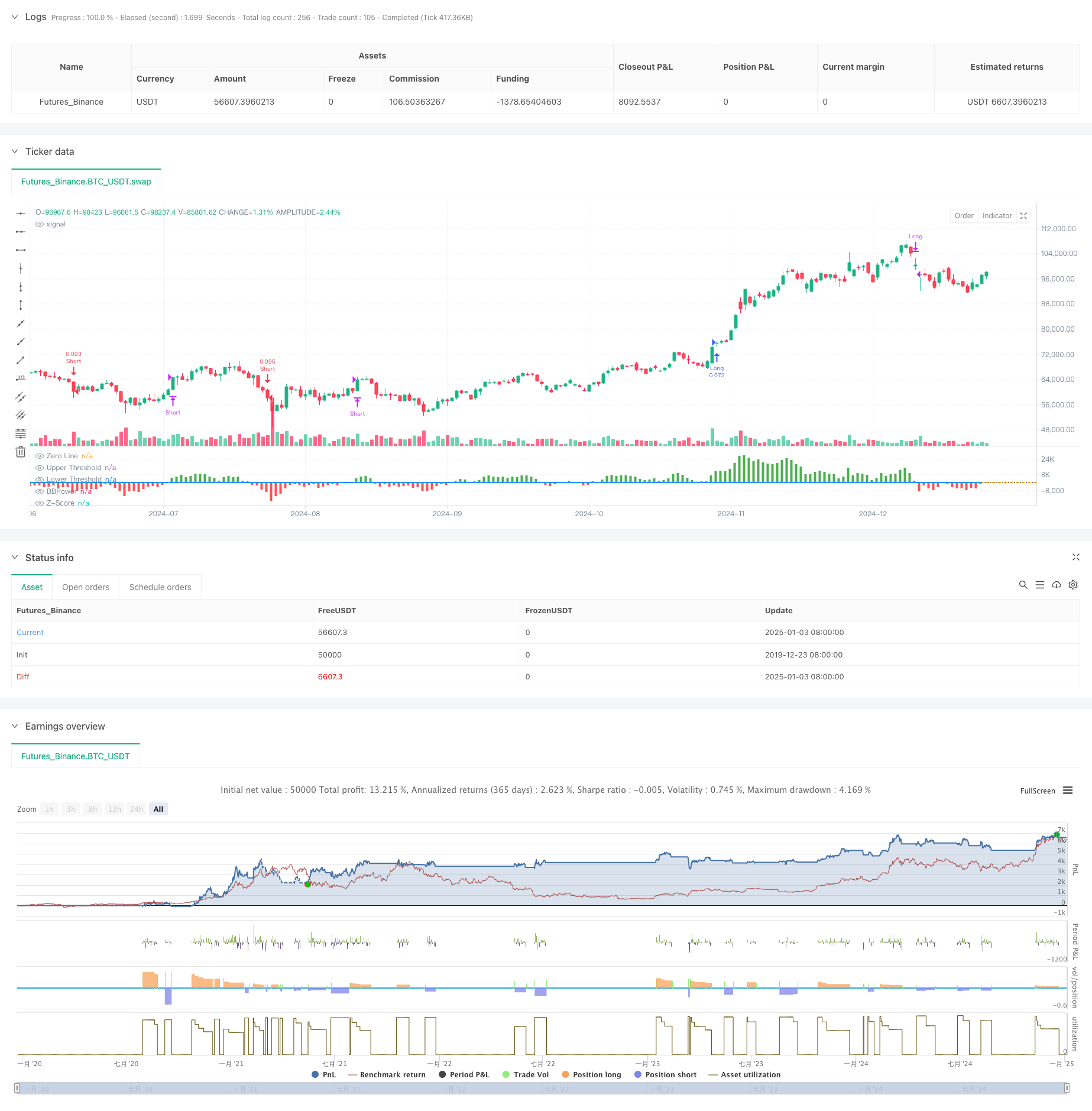

Gambaran umum

Strategi ini menggabungkan indikator Bull Bear Power (BBP) dengan sistem take profit dinamis multi-level berdasarkan persentil volume. Ini menciptakan sistem perdagangan yang adaptif dan dikendalikan risiko melalui analisis multi-dimensi data harga, volume, dan momentum. Logika inti termasuk menggunakan nilai BBP yang dinormalisasi Z-Score sebagai pemicu sinyal perdagangan, sambil menggabungkan analisis persentil volume untuk penyesuaian take profit dinamis.

Prinsip Strategi

Perhitungan inti mencakup beberapa komponen utama:

- Indikator BBP: Mengukur keseimbangan kekuatan pasar dengan menjumlahkan perbedaan antara harga tinggi dan EMA (kekuatan bull) dan harga rendah dan EMA (kekuatan bear).

- Normalisasi Z-Score: Menstandarisasi nilai BBP untuk menilai tingkat penyimpangan kekuatan pasar.

- Analisis Volume: Menghitung volume saat ini relatif terhadap rata-rata bergerak untuk mengukur aktivitas pasar.

- Analisis Persentil: Menghitung persentil historis harga dan volume untuk distribusi probabilitas keadaan pasar.

- Dynamic Take-Profit: Mengatur tingkat take-profit berdasarkan skor komposit ATR, persentil volume, dan persentil harga.

Keuntungan Strategi

- Analisis Multidimensional: Menyediakan perspektif pasar yang komprehensif melalui momentum harga, volume, dan posisi pasar.

- Kemampuan beradaptasi yang tinggi: Beradaptasi dengan lingkungan pasar yang berbeda melalui mekanisme mengambil keuntungan yang dinamis.

- Diversifikasi risiko: Mengimplementasikan strategi mengambil keuntungan multi-level untuk realisasi keuntungan pada tingkat harga yang berbeda.

- Keunggulan Statistik: Mencapai keuntungan yang signifikan melalui Z-Score dan analisis persentil.

- Ekspansibilitas: Kerangka kerja memungkinkan penambahan dimensi analisis baru dengan mudah.

Risiko Strategi

- Sensitivitas Parameter: Beberapa parameter membutuhkan optimasi untuk lingkungan pasar yang berbeda.

- Dependensi dari Lingkungan Pasar: Mungkin berkinerja buruk selama periode volatilitas atau transisi tren.

- Eksekusi Slippage: Perintah take-profit multi-level mungkin menghadapi eksekusi slippage.

- Kompleksitas komputasi: Perhitungan real-time dari beberapa indikator dapat menyebabkan beban sistem.

- Risiko sinyal palsu: Dapat menghasilkan sinyal perdagangan yang salah di pasar yang berbeda.

Arahan Optimasi

- Adaptasi parameter: Memperkenalkan metode pembelajaran mesin untuk optimasi parameter otomatis.

- Prediksi Pasar: Tambahkan modul klasifikasi lingkungan pasar untuk identifikasi kondisi negatif yang dini.

- Optimasi Stop-Loss: Mengimplementasikan mekanisme stop-loss dinamis untuk meningkatkan kontrol risiko.

- Filter sinyal: Tambahkan filter kekuatan tren untuk mengurangi sinyal palsu.

- Manajemen Posisi: Optimalkan algoritma alokasi posisi untuk meningkatkan efisiensi modal.

Ringkasan

Strategi ini menggabungkan indikator BBP tradisional dengan metode analisis kuantitatif modern untuk menciptakan sistem perdagangan dengan dasar teoritis yang kuat dan kepraktisan yang kuat. Ini mencapai keseimbangan yang baik antara pengembalian dan risiko melalui mekanisme pengambilan keuntungan dan penyesuaian dinamis multi-tingkat. Sementara optimasi parameter menimbulkan beberapa tantangan, ekstensibilitas kerangka strategi memberikan ruang yang cukup untuk perbaikan di masa depan. Dalam aplikasi praktis, pedagang harus membuat penyesuaian khusus berdasarkan karakteristik pasar dan preferensi risiko individu.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability.

// Unlike traditional strategies that rely solely on price movements or volume indicators, this strategy synergizes Bollinger Bands Power (BBP) with volume percentile analysis to determine optimal entry and exit points. Additionally, it employs a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to varying market conditions.

// This multi-faceted approach not only enhances signal accuracy but also optimizes risk management, setting it apart from conventional trading methodologies.

//@version=5

strategy("BBP Strategy with Volume-Percentile TP - Strategy [presentTrading] ", overlay=false, precision=3, commission_value= 0.1, commission_type=strategy.commission.percent, slippage= 1, currency=currency.USD, default_qty_type = strategy.percent_of_equity, default_qty_value = 10, initial_capital=10000)

// ————————

// Bull Bear Power Strategy Settings

// ————————

lengthInput = input.int(21, "EMA Length")

zLength = input.int(252, "Z-Score Length")

zThreshold = input.float(1.618, "Z-Score Threshold")

// ————————

// Take Profit Settings

// ————————

tp_group = "Take Profit Settings"

// Enable/disable take profit function

useTP = input.bool(true, "Use Take Profit", group=tp_group)

// === ATR Base Settings ===

// ATR calculation period for determining base price movement range

baseAtrLength = input.int(20, "ATR Period", minval=1, group=tp_group, tooltip="ATR period for calculating base price movement range. Shorter periods are more sensitive to recent volatility")

// === Take Profit Multiplier Settings ===

// First take profit ATR multiplier, usually the most conservative target

atrMult1 = input.float(1.618, "TP1 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="First take profit level ATR multiplier, recommended 1.5-2.0")

// Second take profit ATR multiplier, medium profit target

atrMult2 = input.float(2.382, "TP2 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="Second take profit level ATR multiplier, recommended 2.5-3.0")

// Third take profit ATR multiplier, most aggressive target

atrMult3 = input.float(3.618, "TP3 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="Third take profit level ATR multiplier, recommended 4.0-5.0")

// === Position Size Allocation ===

// First take profit position size, usually larger for securing basic profits

tp1_size = input.float(13, "TP1 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for first take profit, recommended 30-40%")

// Second take profit position size, medium allocation

tp2_size = input.float(13, "TP2 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for second take profit, recommended 30-40%")

// Third take profit position size, usually smaller for catching larger moves

tp3_size = input.float(13, "TP3 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for third take profit, recommended 20-30%")

// ————————

// Volume Analysis Settings

// ————————

vol_group = "Volume Analysis Settings"

// Volume MA period for determining relative volume levels

vol_period = input.int(100, "Volume MA Period", minval=1, group=vol_group, tooltip="Period for calculating volume moving average, recommended 20-30")

// === Volume Level Thresholds ===

// High volume threshold relative to MA

vol_high = input.float(2.0, "High Volume Multiplier", minval=1.0, step=0.1, group=vol_group, tooltip="High volume threshold multiplier, typically 2x MA or above")

// Medium volume threshold

vol_med = input.float(1.5, "Medium Volume Multiplier", minval=1.0, step=0.1, group=vol_group, tooltip="Medium volume threshold multiplier, typically around 1.5x MA")

// Low volume threshold

vol_low = input.float(1.0, "Low Volume Multiplier", minval=0.5, step=0.1, group=vol_group, tooltip="Low volume threshold multiplier, typically around 1x MA")

// === Volume Adjustment Factors ===

// High volume adjustment factor, usually extends take profit targets

vol_high_mult = input.float(1.5, "High Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for high volume")

// Medium volume adjustment factor

vol_med_mult = input.float(1.3, "Medium Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for medium volume")

// Low volume adjustment factor

vol_low_mult = input.float(1.0, "Low Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for low volume")

// ————————

// Percentile Analysis Settings

// ————————

perc_group = "Percentile Analysis Settings"

// Percentile calculation period for evaluating price position

perc_period = input.int(100, "Percentile Period", minval=20, group=perc_group, tooltip="Historical period for percentile calculations, recommended 100-200")

// === Percentile Thresholds ===

// High percentile threshold, typically indicates relative high levels

perc_high = input.float(90, "High Percentile", minval=50, maxval=100, group=perc_group, tooltip="High level percentile threshold, typically above 90")

// Medium percentile threshold

perc_med = input.float(80, "Medium Percentile", minval=50, maxval=100, group=perc_group, tooltip="Medium level percentile threshold, typically around 80")

// Low percentile threshold

perc_low = input.float(70, "Low Percentile", minval=0, maxval=100, group=perc_group, tooltip="Low level percentile threshold, typically around 70")

// === Percentile Adjustment Factors ===

// High percentile adjustment factor

perc_high_mult = input.float(1.5, "High Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for high percentile levels")

// Medium percentile adjustment factor

perc_med_mult = input.float(1.3, "Medium Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for medium percentile levels")

// Low percentile adjustment factor

perc_low_mult = input.float(1.0, "Low Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for low percentile levels")

// ————————

// Core Bull Bear Power Calculations

// ————————

emaClose = ta.ema(close, lengthInput)

bullPower = high - emaClose

bearPower = low - emaClose

bbp = bullPower + bearPower

bbp_mean = ta.sma(bbp, zLength)

bbp_std = ta.stdev(bbp, zLength)

zscore = (bbp - bbp_mean) / bbp_std

// ————————

// Volume & Percentile Analysis

// ————————

// 成交量分析

vol_sma = ta.sma(volume, vol_period)

vol_mult = volume / vol_sma

// 百分位數計算

calcPercentile(src) =>

var values = array.new_float(0)

array.unshift(values, src)

if array.size(values) > perc_period

array.pop(values)

array.size(values) > 0 ? array.percentrank(values, array.size(values)-1) * 100 : 50

price_perc = calcPercentile(close)

vol_perc = calcPercentile(volume)

// 止盈動態調整系數計算

getTpFactor() =>

vol_score = vol_mult > vol_high ? vol_high_mult : vol_mult > vol_med ? vol_med_mult : vol_mult > vol_low ? vol_low_mult : 0.8

price_score = price_perc > perc_high ? perc_high_mult :price_perc > perc_med ? perc_med_mult :price_perc > perc_low ? perc_low_mult : 0.8

math.avg(vol_score, price_score)

// ————————

// Entry/Exit Logic

// ————————

longCondition = ta.crossover(zscore, zThreshold)

shortCondition = ta.crossunder(zscore, -zThreshold)

exitLongCondition = ta.crossunder(zscore, 0)

exitShortCondition = ta.crossover(zscore, 0)

if (barstate.isconfirmed)

if longCondition

strategy.entry("Long", strategy.long)

if shortCondition

strategy.entry("Short", strategy.short)

if exitLongCondition

strategy.close("Long")

if exitShortCondition

strategy.close("Short")

// ————————

// Take Profit Execution

// ————————

if useTP and strategy.position_size != 0

base_move = ta.atr(baseAtrLength)

tp_factor = getTpFactor()

is_long = strategy.position_size > 0

entry_price = strategy.position_avg_price

if is_long

tp1_price = entry_price + (base_move * atrMult1 * tp_factor)

tp2_price = entry_price + (base_move * atrMult2 * tp_factor)

tp3_price = entry_price + (base_move * atrMult3 * tp_factor)

strategy.exit("TP1", "Long", qty_percent=tp1_size, limit=tp1_price)

strategy.exit("TP2", "Long", qty_percent=tp2_size, limit=tp2_price)

strategy.exit("TP3", "Long", qty_percent=tp3_size, limit=tp3_price)

else

tp1_price = entry_price - (base_move * atrMult1 * tp_factor)

tp2_price = entry_price - (base_move * atrMult2 * tp_factor)

tp3_price = entry_price - (base_move * atrMult3 * tp_factor)

strategy.exit("TP1", "Short", qty_percent=tp1_size, limit=tp1_price)

strategy.exit("TP2", "Short", qty_percent=tp2_size, limit=tp2_price)

strategy.exit("TP3", "Short", qty_percent=tp3_size, limit=tp3_price)

// ————————

// Plotting

// ————————

plot(bbp, color=bbp >= 0 ? color.new(color.green, 0) : color.new(color.red, 0),

title="BBPower", style=plot.style_columns)

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dotted)

plot(zscore, title="Z-Score", color=color.blue, linewidth=2)

hline(zThreshold, "Upper Threshold", color=color.orange, linestyle=hline.style_dashed)

hline(-zThreshold, "Lower Threshold", color=color.orange, linestyle=hline.style_dashed)

- Tren Dinamis Mengikuti dengan Strategi Take-Profit dan Stop-Loss yang Tepat

- Tren Dinamis Mengikuti Strategi Menggabungkan Supertrend dan EMA

- Strategi crossover rata-rata bergerak eksponensial yang dikelola risiko dinamis

- Triple Exponential Moving Average Trend Trading Strategi

- EMA Advanced Crossover Trend Following Strategy dengan Sistem Manajemen Hentian Dinamis berbasis ATR

- Sistem Strategi Dinamis Crossover Multi-Indikator: Model Perdagangan Kuantitatif Berdasarkan EMA, RVI dan Sinyal Perdagangan

- Strategi Momentum Crossover MACD dengan Optimasi Take Profit dan Stop Loss Dinamis

- Sistem Manajemen Modal Berbasis Kekuatan Tren RSI dan ADX

- Adaptive Moving Average Crossover dengan Trailing Stop-Loss Strategy

- Strategi perdagangan swing panjang/pendek yang dinamis dengan sistem sinyal crossover rata-rata bergerak

- Strategi perdagangan pola candlestick multi-frame

- Algoritma Perdagangan Tren Dinamis Supertrend Multi-Timeframe

- Strategi Trading Crossover MACD Lanjutan dengan Manajemen Risiko Adaptif

- Strategi Penangkapan Tren Kuantitatif Berdasarkan Analisis Panjang Wick Candle

- Strategi Perdagangan Breakout VWAP dengan Penyimpangan Standar Ganda

- Strategi Jaringan Panjang Berdasarkan Penarikan dan Target Keuntungan

- Trend crossover rata-rata bergerak dinamis mengikuti strategi dengan sistem manajemen risiko ATR

- Multi-Indikator Optimized KDJ Trend Crossover Strategy Berdasarkan Sistem Perdagangan Pola Stochastic Dinamis

- Multi-Timeframe Heikin-Ashi Moving Average Trend Mengikuti Sistem Perdagangan

- Tren Dinamis yang Disesuaikan dengan Volatilitas Mengikuti Strategi Berdasarkan Indikator DI dengan Manajemen Stop ATR

- Z-Score Normalized Linear Signal Strategi Perdagangan Kuantitatif

- Strategi Perdagangan Tren Intelektual Stochastic Multi-Parameter

- Multi-EMA Cross dengan Volume-Price Momentum Trading Strategy

- Sistem Perdagangan Tren Penembusan Tingkat Harga Multi Periode Berdasarkan Tingkat Harga Kunci

- Strategi Trading Retracement Fibonacci Lanjutan Mengikuti Tren dan Reversal

- EMA Advanced Crossover Trend Following Strategy dengan Sistem Manajemen Hentian Dinamis berbasis ATR

- Strategi perdagangan Bollinger Bands dengan sinyal pengembalian rasional

- Trend rata-rata bergerak multi-periode mengikuti strategi silang VWAP

- Opsi sinergi RSI-Rata-rata bergerak ganda Strategi perdagangan kuantitatif

- Advanced WaveTrend dan EMA Ribbon Fusion Trading Strategy