볼 베어 파워 트레이딩 전략, 부피 퍼센틸 기반의 동적 영리 시스템

저자:차오장, 날짜: 2025-01-06 16:16:04태그:GDPEMAATRTP

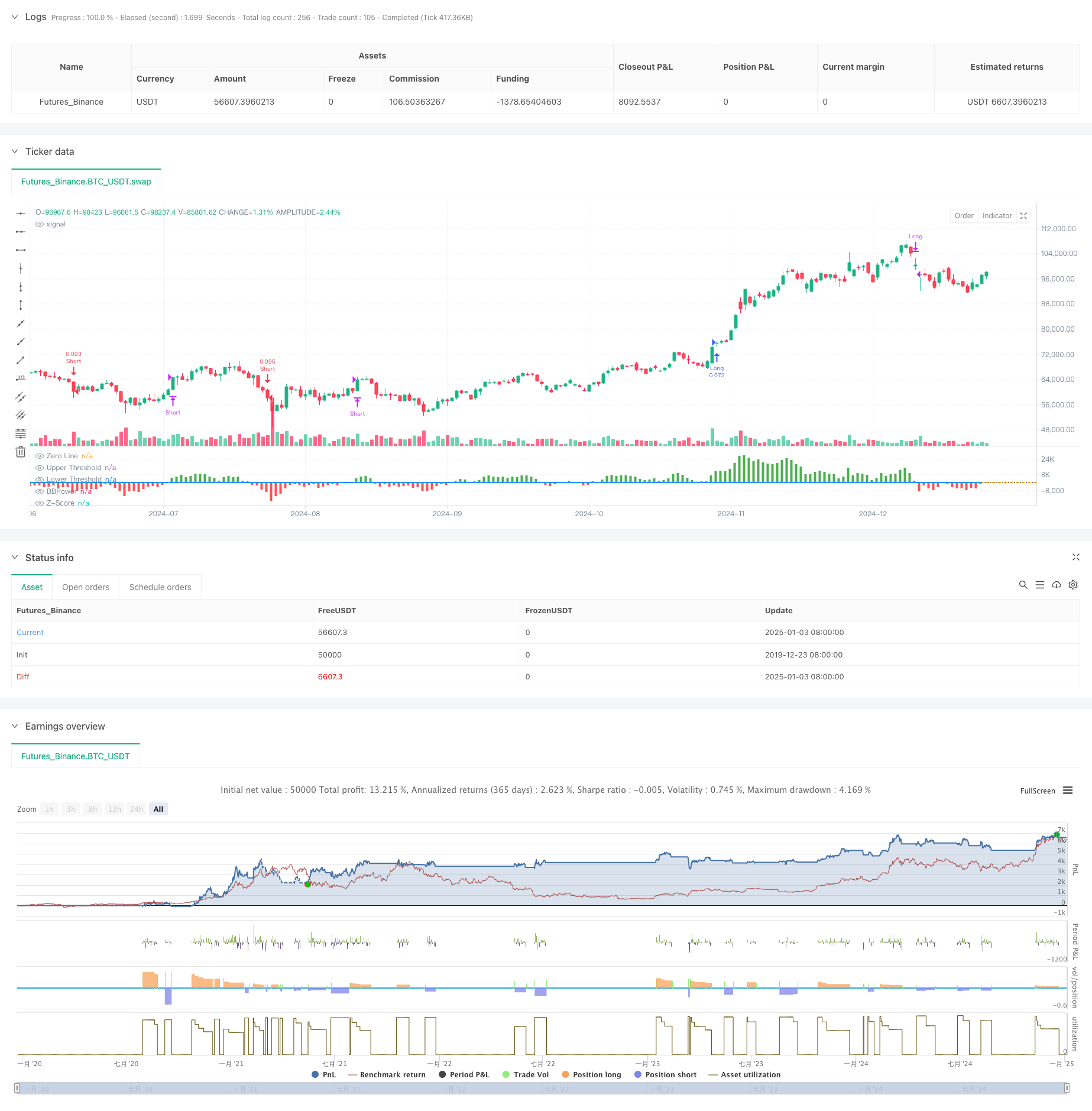

전반적인 설명

이 전략은 볼 베어 파워 (BBP) 지표와 볼륨 퍼센틸을 기반으로 한 다단계 동적 영리 시스템으로 결합합니다. 가격, 볼륨 및 모멘텀 데이터의 다차원 분석을 통해 적응적이고 위험 통제 된 거래 시스템을 만듭니다. 핵심 논리는 Z-Score 정상화된 BBP 값을 거래 신호 트리거로 사용하는 것을 포함하며, 동적 영리 조정을위한 볼륨 퍼센틸 분석을 통합합니다.

전략 원칙

핵심 계산에는 몇 가지 핵심 요소가 포함됩니다.

- BBP 지표: 높은 가격과 EMA (bull power) 와 낮은 가격과 EMA (bear power) 의 차이를 합쳐서 시장 힘 균형을 측정합니다.

- Z 점수 정상화: 시장 강도 오차 수준을 평가하기 위해 BBP 값을 표준화합니다.

- 부피 분석: 시장 활동을 측정하기 위해 이동 평균에 대한 현재 부피를 계산합니다.

- 퍼센틸 분석: 시장 상태 확률 분포에 대한 가격과 부피의 역사적 퍼센틸을 계산합니다.

- 동적 취득: ATR, 부피 퍼센틸, 가격 퍼센틸의 복합 점수를 기반으로 취득 수준을 조정합니다.

전략적 장점

- 다차원적 분석: 가격 동력, 양량 및 시장 포지셔닝을 통해 포괄적인 시장 관점을 제공합니다.

- 높은 적응력: 동적인 수익 메커니즘을 통해 다른 시장 환경에 적응합니다.

- 리스크 다양화: 다양한 가격 수준에서 수익을 창출하기 위해 다단계 수익 전략을 실행합니다.

- 통계적 우수성: Z 점수 및 퍼센틸 분석을 통해 상당한 이점을 얻습니다.

- 확장성: 프레임워크는 새로운 분석 차원을 쉽게 추가 할 수 있습니다.

전략 위험

- 매개 변수 민감성: 여러 매개 변수들은 다른 시장 환경에 최적화를 요구합니다.

- 시장 환경 의존성: 변동성 또는 트렌드 전환 기간 동안 실적이 떨어질 수 있습니다.

- 실행 미끄러짐: 다단계 취득 주문은 실행 미끄러짐을 겪을 수 있습니다.

- 계산 복잡성: 여러 지표의 실시간 계산은 시스템 부하를 유발할 수 있습니다.

- 가짜 신호 위험: 다양한 시장에서 잘못된 거래 신호를 생성할 수 있습니다.

최적화 방향

- 매개 변수 적응: 자동 매개 변수 최적화를 위한 기계 학습 방법을 소개합니다.

- 시장 예측: 불리한 조건의 조기 식별을 위해 시장 환경 분류 모듈을 추가합니다.

- 스톱 로스 최적화: 더 나은 위험 통제를 위해 동적 스톱 로스 메커니즘을 구현합니다.

- 신호 필터링: 잘못된 신호를 줄이기 위해 트렌드 강도 필터를 추가합니다.

- 포지션 관리: 자본 효율성을 향상시키기 위해 포지션 할당 알고리즘을 최적화합니다.

요약

이 전략은 전통적인 BBP 지표와 현대적인 양적 분석 방법을 결합하여 탄탄한 이론적 기초와 강력한 실용성을 갖춘 거래 시스템을 만듭니다. 다단계 수익 및 동적 조정 메커니즘을 통해 수익과 위험 사이의 좋은 균형을 달성합니다. 매개 변수 최적화는 몇 가지 과제를 제시하지만 전략 프레임워크의 확장성은 향후 개선에 대한 충분한 공간을 제공합니다. 실제 응용에서는 거래자가 시장 특성과 개별 위험 선호도에 따라 특정 조정을해야합니다.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability.

// Unlike traditional strategies that rely solely on price movements or volume indicators, this strategy synergizes Bollinger Bands Power (BBP) with volume percentile analysis to determine optimal entry and exit points. Additionally, it employs a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to varying market conditions.

// This multi-faceted approach not only enhances signal accuracy but also optimizes risk management, setting it apart from conventional trading methodologies.

//@version=5

strategy("BBP Strategy with Volume-Percentile TP - Strategy [presentTrading] ", overlay=false, precision=3, commission_value= 0.1, commission_type=strategy.commission.percent, slippage= 1, currency=currency.USD, default_qty_type = strategy.percent_of_equity, default_qty_value = 10, initial_capital=10000)

// ————————

// Bull Bear Power Strategy Settings

// ————————

lengthInput = input.int(21, "EMA Length")

zLength = input.int(252, "Z-Score Length")

zThreshold = input.float(1.618, "Z-Score Threshold")

// ————————

// Take Profit Settings

// ————————

tp_group = "Take Profit Settings"

// Enable/disable take profit function

useTP = input.bool(true, "Use Take Profit", group=tp_group)

// === ATR Base Settings ===

// ATR calculation period for determining base price movement range

baseAtrLength = input.int(20, "ATR Period", minval=1, group=tp_group, tooltip="ATR period for calculating base price movement range. Shorter periods are more sensitive to recent volatility")

// === Take Profit Multiplier Settings ===

// First take profit ATR multiplier, usually the most conservative target

atrMult1 = input.float(1.618, "TP1 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="First take profit level ATR multiplier, recommended 1.5-2.0")

// Second take profit ATR multiplier, medium profit target

atrMult2 = input.float(2.382, "TP2 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="Second take profit level ATR multiplier, recommended 2.5-3.0")

// Third take profit ATR multiplier, most aggressive target

atrMult3 = input.float(3.618, "TP3 ATR Multiplier", minval=0.1, step=0.1, group=tp_group, tooltip="Third take profit level ATR multiplier, recommended 4.0-5.0")

// === Position Size Allocation ===

// First take profit position size, usually larger for securing basic profits

tp1_size = input.float(13, "TP1 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for first take profit, recommended 30-40%")

// Second take profit position size, medium allocation

tp2_size = input.float(13, "TP2 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for second take profit, recommended 30-40%")

// Third take profit position size, usually smaller for catching larger moves

tp3_size = input.float(13, "TP3 Position %", minval=1, maxval=100, group=tp_group, tooltip="Position size percentage for third take profit, recommended 20-30%")

// ————————

// Volume Analysis Settings

// ————————

vol_group = "Volume Analysis Settings"

// Volume MA period for determining relative volume levels

vol_period = input.int(100, "Volume MA Period", minval=1, group=vol_group, tooltip="Period for calculating volume moving average, recommended 20-30")

// === Volume Level Thresholds ===

// High volume threshold relative to MA

vol_high = input.float(2.0, "High Volume Multiplier", minval=1.0, step=0.1, group=vol_group, tooltip="High volume threshold multiplier, typically 2x MA or above")

// Medium volume threshold

vol_med = input.float(1.5, "Medium Volume Multiplier", minval=1.0, step=0.1, group=vol_group, tooltip="Medium volume threshold multiplier, typically around 1.5x MA")

// Low volume threshold

vol_low = input.float(1.0, "Low Volume Multiplier", minval=0.5, step=0.1, group=vol_group, tooltip="Low volume threshold multiplier, typically around 1x MA")

// === Volume Adjustment Factors ===

// High volume adjustment factor, usually extends take profit targets

vol_high_mult = input.float(1.5, "High Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for high volume")

// Medium volume adjustment factor

vol_med_mult = input.float(1.3, "Medium Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for medium volume")

// Low volume adjustment factor

vol_low_mult = input.float(1.0, "Low Volume Factor", minval=0.1, step=0.1, group=vol_group, tooltip="Take profit adjustment factor for low volume")

// ————————

// Percentile Analysis Settings

// ————————

perc_group = "Percentile Analysis Settings"

// Percentile calculation period for evaluating price position

perc_period = input.int(100, "Percentile Period", minval=20, group=perc_group, tooltip="Historical period for percentile calculations, recommended 100-200")

// === Percentile Thresholds ===

// High percentile threshold, typically indicates relative high levels

perc_high = input.float(90, "High Percentile", minval=50, maxval=100, group=perc_group, tooltip="High level percentile threshold, typically above 90")

// Medium percentile threshold

perc_med = input.float(80, "Medium Percentile", minval=50, maxval=100, group=perc_group, tooltip="Medium level percentile threshold, typically around 80")

// Low percentile threshold

perc_low = input.float(70, "Low Percentile", minval=0, maxval=100, group=perc_group, tooltip="Low level percentile threshold, typically around 70")

// === Percentile Adjustment Factors ===

// High percentile adjustment factor

perc_high_mult = input.float(1.5, "High Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for high percentile levels")

// Medium percentile adjustment factor

perc_med_mult = input.float(1.3, "Medium Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for medium percentile levels")

// Low percentile adjustment factor

perc_low_mult = input.float(1.0, "Low Percentile Factor", minval=0.1, step=0.1, group=perc_group, tooltip="Take profit adjustment factor for low percentile levels")

// ————————

// Core Bull Bear Power Calculations

// ————————

emaClose = ta.ema(close, lengthInput)

bullPower = high - emaClose

bearPower = low - emaClose

bbp = bullPower + bearPower

bbp_mean = ta.sma(bbp, zLength)

bbp_std = ta.stdev(bbp, zLength)

zscore = (bbp - bbp_mean) / bbp_std

// ————————

// Volume & Percentile Analysis

// ————————

// 成交量分析

vol_sma = ta.sma(volume, vol_period)

vol_mult = volume / vol_sma

// 百分位數計算

calcPercentile(src) =>

var values = array.new_float(0)

array.unshift(values, src)

if array.size(values) > perc_period

array.pop(values)

array.size(values) > 0 ? array.percentrank(values, array.size(values)-1) * 100 : 50

price_perc = calcPercentile(close)

vol_perc = calcPercentile(volume)

// 止盈動態調整系數計算

getTpFactor() =>

vol_score = vol_mult > vol_high ? vol_high_mult : vol_mult > vol_med ? vol_med_mult : vol_mult > vol_low ? vol_low_mult : 0.8

price_score = price_perc > perc_high ? perc_high_mult :price_perc > perc_med ? perc_med_mult :price_perc > perc_low ? perc_low_mult : 0.8

math.avg(vol_score, price_score)

// ————————

// Entry/Exit Logic

// ————————

longCondition = ta.crossover(zscore, zThreshold)

shortCondition = ta.crossunder(zscore, -zThreshold)

exitLongCondition = ta.crossunder(zscore, 0)

exitShortCondition = ta.crossover(zscore, 0)

if (barstate.isconfirmed)

if longCondition

strategy.entry("Long", strategy.long)

if shortCondition

strategy.entry("Short", strategy.short)

if exitLongCondition

strategy.close("Long")

if exitShortCondition

strategy.close("Short")

// ————————

// Take Profit Execution

// ————————

if useTP and strategy.position_size != 0

base_move = ta.atr(baseAtrLength)

tp_factor = getTpFactor()

is_long = strategy.position_size > 0

entry_price = strategy.position_avg_price

if is_long

tp1_price = entry_price + (base_move * atrMult1 * tp_factor)

tp2_price = entry_price + (base_move * atrMult2 * tp_factor)

tp3_price = entry_price + (base_move * atrMult3 * tp_factor)

strategy.exit("TP1", "Long", qty_percent=tp1_size, limit=tp1_price)

strategy.exit("TP2", "Long", qty_percent=tp2_size, limit=tp2_price)

strategy.exit("TP3", "Long", qty_percent=tp3_size, limit=tp3_price)

else

tp1_price = entry_price - (base_move * atrMult1 * tp_factor)

tp2_price = entry_price - (base_move * atrMult2 * tp_factor)

tp3_price = entry_price - (base_move * atrMult3 * tp_factor)

strategy.exit("TP1", "Short", qty_percent=tp1_size, limit=tp1_price)

strategy.exit("TP2", "Short", qty_percent=tp2_size, limit=tp2_price)

strategy.exit("TP3", "Short", qty_percent=tp3_size, limit=tp3_price)

// ————————

// Plotting

// ————————

plot(bbp, color=bbp >= 0 ? color.new(color.green, 0) : color.new(color.red, 0),

title="BBPower", style=plot.style_columns)

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dotted)

plot(zscore, title="Z-Score", color=color.blue, linewidth=2)

hline(zThreshold, "Upper Threshold", color=color.orange, linestyle=hline.style_dashed)

hline(-zThreshold, "Lower Threshold", color=color.orange, linestyle=hline.style_dashed)

관련

- 정확 한 영업 및 중단 손실 전략과 함께 동적인 추세를 따르고 있습니다

- 슈퍼트렌드와 EMA를 결합하는 전략을 따르는 동적 트렌드

- 동적 리스크 관리 기하급수적 이동 평균 크로스오버 전략

- 트리플 익스포넌셜 이동 평균 트렌드 거래 전략

- ATR 기반의 동적 정지 관리 시스템으로 고급 EMA 크로스오버 트렌드를 따르는 전략

- 다중 지표 크로스오버 동적 전략 시스템: EMA, RVI 및 거래 신호에 기반한 양적 거래 모델

- 동적 취익 및 중지 손실 최적화와 함께 MACD 크로스 오버 모멘텀 전략

- RSI 모멘텀 및 ADX 트렌드 강도에 기반한 자본 관리 시스템

- 후속 스톱 로스 전략과 함께 적응적인 이동 평균 크로스오버

- 이동 평균 크로스오버 신호 시스템으로 동적 장기/단기 스윙 거래 전략

더 많은

- 멀티 타임프레임 촛불 패턴 거래 전략

- 멀티 타임프레임 슈퍼트렌드 동적 트렌드 거래 알고리즘

- 적응적 리스크 관리와 함께 고급 MACD 크로스오버 거래 전략

- 촛불 빗 길이를 분석한 양적 트렌드 포착 전략

- 통계적 이중 표준 오차 VWAP 브레이크업 거래 전략

- 유출 및 목표 수익에 기반한 긴 네트워크 전략

- 동적 이동 평균 크로스오버 트렌드 ATR 리스크 관리 시스템과 전략에 따라

- 다중 지표 최적화된 KDJ 트렌드 크로스오버 전략

- 다중 시간 프레임 하이킨-아시 이동 평균 트렌드 다음 거래 시스템

- 동적 변동성 조정 트렌드 다음 전략 ATR 정지 관리와 함께 DI 지표에 기반

- Z-Score 표준화된 선형 신호 양적 거래 전략

- 여러 매개 변수 스토카스틱 지능 트렌드 거래 전략

- 분량-가격 동력 거래 전략과 함께 멀티 EMA 크로스

- 주요 가격 수준에 기초한 다기기 가격 레벨 브레이크 트렌드 거래 시스템

- 고급 피보나치 리트레이싱 트렌드 추적 및 역전 거래 전략

- ATR 기반의 동적 정지 관리 시스템으로 고급 EMA 크로스오버 트렌드를 따르는 전략

- 평균 반전 볼링거 밴드 거래 전략 합리적인 수익 신호

- VWAP 크로스 전략에 따라 다기간에 이동 평균 트렌드

- 이중 이동 평균-RSI 시너지 옵션 양적 거래 전략

- 고급 웨이브 트렌드와 EMA 리본 퓨전 거래 전략