EMA均线与抛物线SAR组合策略

Author: ChaoZhang, Date: 2024-06-07 15:23:12Tags: EMASAR

概述

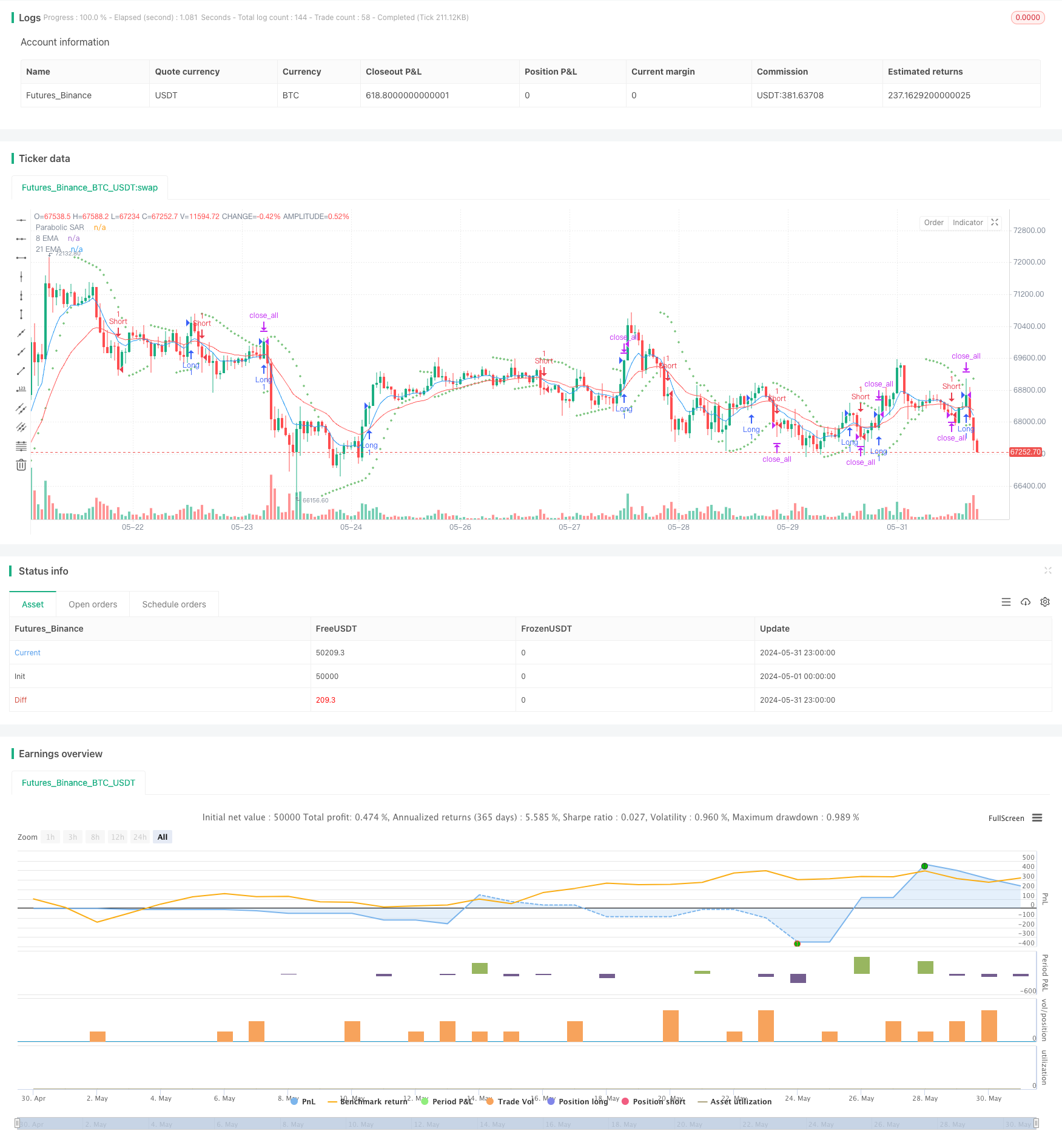

该策略结合了8周期和21周期的指数移动平均线(EMA)以及抛物线SAR指标,旨在捕捉趋势并管理风险。策略根据特定的交叉和价格行为条件开仓和平仓,并定义了包括固定止损和强制在特定时间平仓的出场规则。

策略原理

该策略使用两条不同周期的EMA(8周期和21周期)以及抛物线SAR指标来确定开仓和平仓条件。当短期EMA在长期EMA上方交叉,且收盘价高于SAR时,策略开多头仓位;当短期EMA在长期EMA下方交叉,且收盘价低于SAR时,策略开空头仓位。多头仓位在收盘价低于SAR时平仓,空头仓位在收盘价高于SAR时平仓。策略还设置了固定止损点数,以控制单笔交易的风险。此外,该策略要求在每个交易日的15:15强制平掉所有仓位。

策略优势

- 结合EMA和SAR指标,可以更好地捕捉趋势和判断趋势反转。

- 固定止损有助于控制单笔交易的风险。

- 在每个交易日的固定时间平仓,避免隔夜持仓风险。

- 参数可调,适应不同的市场环境和交易品种。

策略风险

- EMA和SAR指标可能会发出错误信号,导致亏损交易。

- 固定止损点数可能无法适应市场波动,导致止损位置设置不当。

- 在趋势不明朗或波动较大的市场中,该策略可能会频繁开平仓,导致高昂的交易成本。

- 该策略缺乏对市场情绪和基本面因素的考量,可能错过一些重要的交易机会。

策略优化方向

- 引入更多技术指标,如RSI、MACD等,以提高开平仓信号的可靠性。

- 优化止损和止盈规则,如采用动态止损或基于波动率的止损方法,以更好地适应市场变化。

- 考虑引入市场情绪和基本面因素,如交易量、新闻事件等,以提高策略的全面性。

- 对不同市场和交易品种进行参数优化和回测,找出最佳参数组合。

总结

EMA均线与抛物线SAR组合策略通过结合两种常用的技术指标,试图捕捉趋势并控制风险。该策略简单易懂,适合初学者学习和使用。然而,该策略也存在一些局限性,如对市场波动适应性不足,缺乏对市场情绪和基本面因素的考量等。因此,在实际应用中,需要根据具体市场和交易品种对策略进行优化和改进,以提高其稳定性和盈利能力。

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("EMA and Parabolic SAR Strategy", overlay=true)

// Input parameters for EMAs and Parabolic SAR

emaShortPeriod = input.int(8, title="Short EMA Period")

emaLongPeriod = input.int(21, title="Long EMA Period")

sarStart = input.float(0.02, title="Parabolic SAR Start")

sarIncrement = input.float(0.02, title="Parabolic SAR Increment")

sarMaximum = input.float(0.2, title="Parabolic SAR Maximum")

fixedSL = input.int(83, title="Fixed Stop Loss (pts)")

// Calculate EMAs and Parabolic SAR

emaShort = ta.ema(close, emaShortPeriod)

emaLong = ta.ema(close, emaLongPeriod)

sar = ta.sar(sarStart, sarIncrement, sarMaximum)

// Entry conditions

longCondition = ta.crossover(emaShort, emaLong) and close > sar

shortCondition = ta.crossunder(emaShort, emaLong) and close < sar

// Exit conditions

longExitCondition = close < sar

shortExitCondition = close > sar

// Strategy entry and exit

if (longCondition)

strategy.entry("Long", strategy.long)

if (shortCondition)

strategy.entry("Short", strategy.short)

if (longExitCondition)

strategy.close("Long")

if (shortExitCondition)

strategy.close("Short")

// Fixed Stop Loss

strategy.exit("Long Exit", "Long", stop=close - fixedSL * syminfo.mintick)

strategy.exit("Short Exit", "Short", stop=close + fixedSL * syminfo.mintick)

// Exit all positions at 15:15

exitHour = 15

exitMinute = 15

exitTime = timestamp(year(timenow), month(timenow), dayofmonth(timenow), exitHour, exitMinute)

if (timenow >= exitTime)

strategy.close_all()

// Plot EMAs and Parabolic SAR

plot(emaShort, color=color.blue, title="8 EMA")

plot(emaLong, color=color.red, title="21 EMA")

plot(sar, style=plot.style_cross, color=color.green, title="Parabolic SAR")

相关内容

- EMA SAR 中长期趋势跟踪策略

- HIGH LOW SAR

- 多重订单突破趋势跟踪策略

- 艾略特波浪理论4-9脉冲波自动检测交易策略

- 多重均线黄金交叉分批止盈策略

- EMA均线交叉与短期信号策略

- EMA TREND CLOUD

- Ichimoku Cloud Smooth Oscillator

- 双均线交叉动态颜色量化策略

- 双均线动量趋势交易策略结合满实体烛线信号系统

更多内容

- 基于支撑位和阻力位反转形态的量化交易策略

- 均线,简单移动平均线,均线斜率,追踪止损,重新进场

- TSI交叉策略

- EMA双均线交叉策略

- Williams %R 动态调整止盈止损策略

- RSI动态回撤止损策略

- VWAP交易策略与成交量异常监测

- Supertrend和EMA组合策略

- TGT基于价格下跌买入策略

- EMA交叉与RSI过滤的双重趋势策略

- MACD与RSI相结合的多重过滤日内交易策略

- 基于两个市场价格关系的套利交易策略

- RSI基于百分比止盈止损的交易策略

- MACD与马丁策略结合的多头优化交易策略

- Elliott 波动随机EMA策略

- 布林带交叉移动平均策略

- SMA双均线交叉策略

- 10SMA与MACD双重趋势跟踪交易策略

- MACD和RSI结合的自然交易策略

- 动态时间框架高低点突破策略